BigMint's India steel index drops w-o-w on inventory pressure, soft trade sentiment

...

- BF rebar prices drop to 5-month low in early June

- HRC prices weaken on muted downstream demand

- Longs may decline further, flats to remain stable

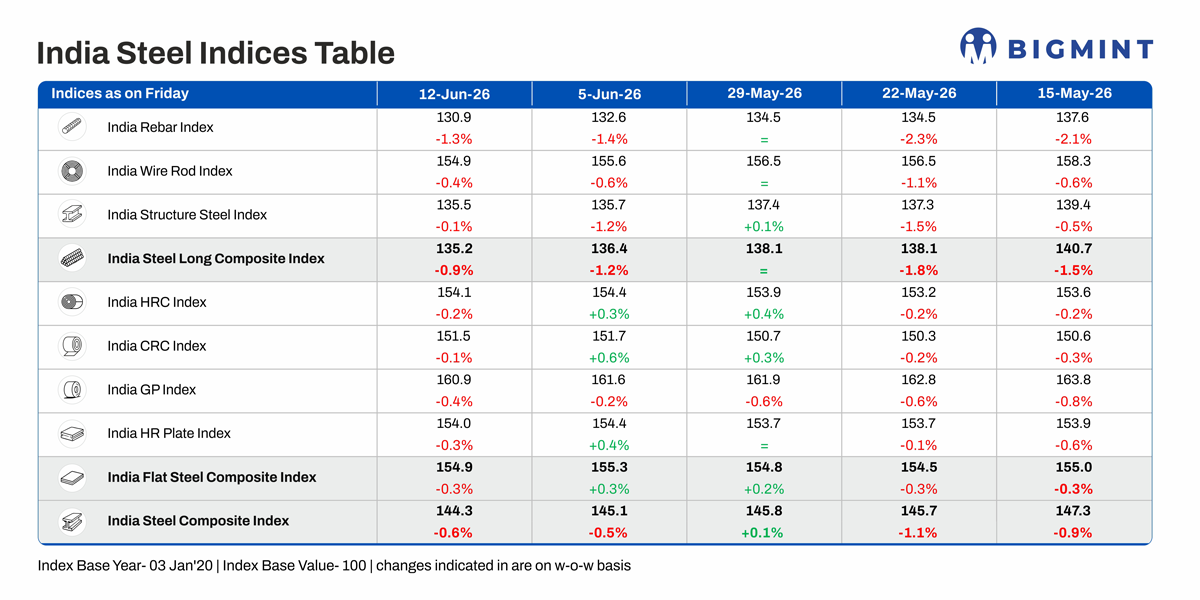

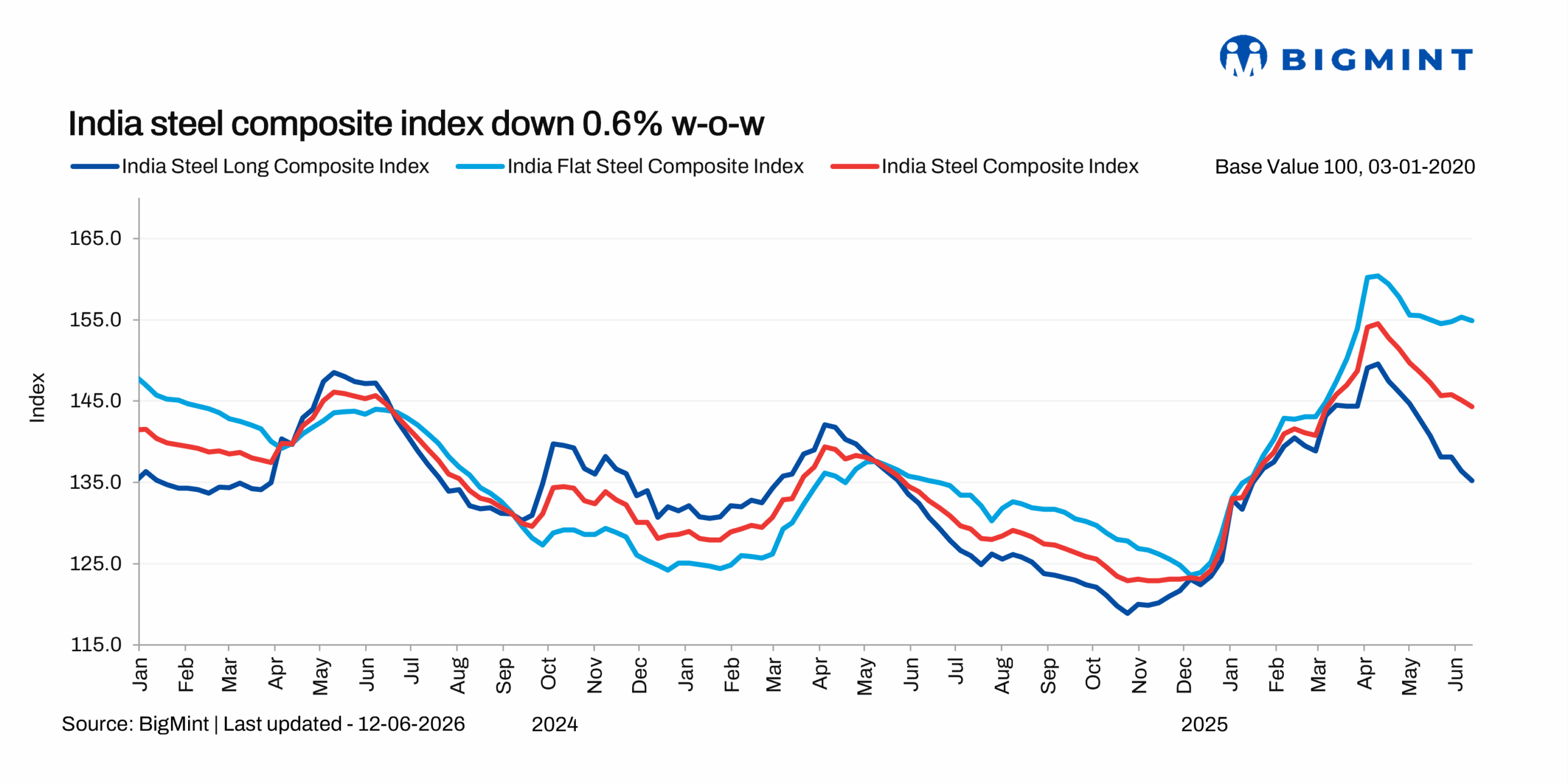

Morning Brief: BigMint's flagship India steel composite index declined by 0.6% w-o-w, as assessed on the week ended 12 June 2026, as steel prices weakened further on slow trade market conditions, although currency depreciation contributed to volatility in the imported raw materials markets and added to the cost burden for producers. Need-based buying in the market led to inventory accumulation, especially in the longs segment, which affected on prices.

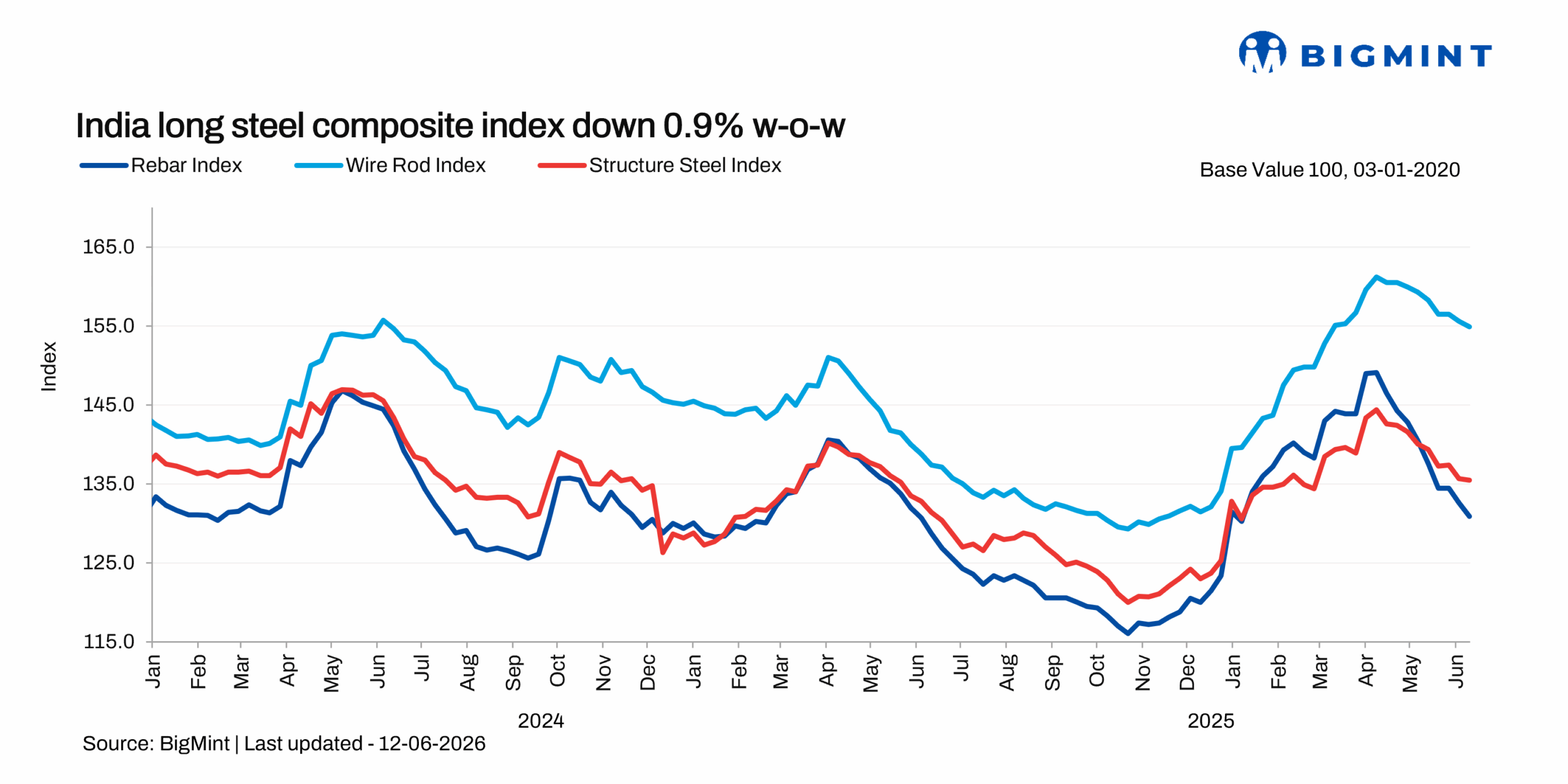

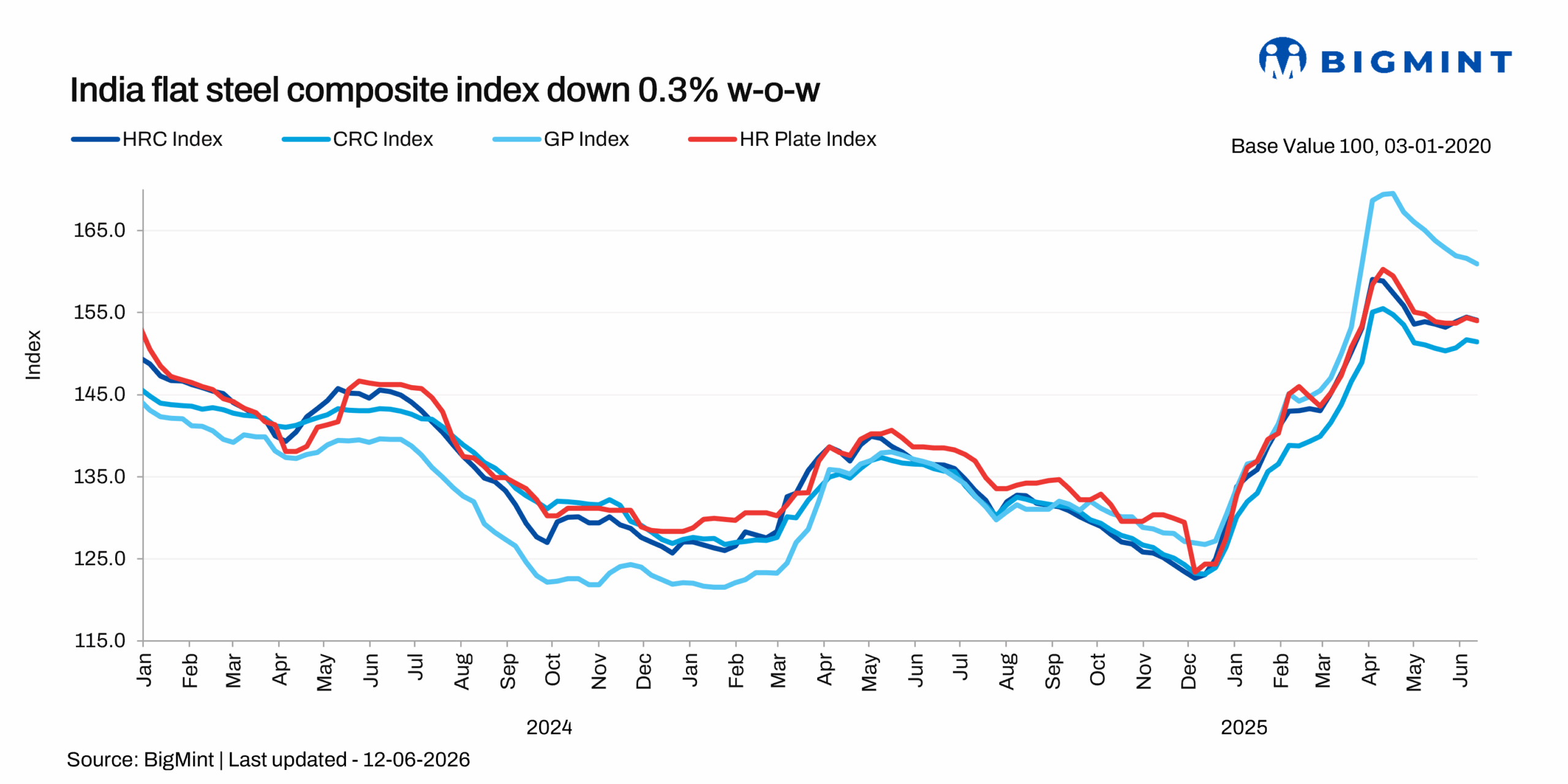

While the flat steel index fell by 0.3% w-o-w, the longs index dropped 0.9% after witnessing a decline of 1.2% the previous week. Fresh export bookings in May, as well as the strength in Chinese HRC prices, had provided some support to flats compared with longs. However, declining raw material prices and increased domestic supplies following the restart of facilities post-maintenance breaks by key mills are weighing on prices.

Highlights of price movements

BF rebar prices drop to 5-month low: BigMint's benchmark assessment for rebar (IS 1786 Fe 550D, 1232 mm, BF route, ex-Mumbai) was assessed at INR 52,900/t as of 12 June 2026, down by INR 2,100/t from INR 55,000/t recorded on 5 June. Prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Prices have dropped to a five-month low. The correction was driven by adequate inventories at the distributor level (25-30 days) and a cautious procurement strategy both in the retail and project segments. Demand remained largely need-based across regions. Weakening raw material prices and the gap with induction furnace (IF)-route rebar also pressured BF rebar prices.

IF rebar market weakens further: Slow construction activity amid heatwave and weak demand visibility also impacted IF rebar, with prices falling by INR 500-1,000/t across markets. Slow bookings kept sentiment cautious. Sluggish demand and limited acceptance of higher offers forced sellers to lower prices and offer discounts. Mills reported sales at around 50-70% of production, while inventories across regions stood at 10-15 days.

Flat steel prices edge down: BigMint's bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) inched down by INR 100/t ($1/t) w-o-w to INR 58,300/t ($611/t) as of 9 June against INR 58,400/t ($612/t) on 2 June. Meanwhile, benchmark CRC (IS513, Gr O, 0.9 mm/CTL) prices held stable at INR 65,200/t ($684/t) over the same period. The assessment excludes 18% GST and is ex-Mumbai.

Despite quantity discounts offered by producers, pre-monsoon demand remained weak. Trade prices were affected by cautious buying sentiment. Although distributors in north India reported limited availability of certain thicknesses and sizes, supply tightness failed to generate meaningful market momentum. Market participants also highlighted payment collection challenges as a key concern, which continued to weigh on trading activity and limit purchases to immediate requirements.

The automotive sector offered mixed cues to the flat steel market. According to SIAM data, domestic vehicle sales declined by 5.2% m-o-m to 2.47 million units in April, while overall production fell by 1.9%, suggesting a moderation in downstream steel consumption after a strong March performance.

HRC exports muted but prices stable: India's HRC export activity remained subdued as buying interest from Europe was muted due to uncertainty surrounding the allocation of country-specific quotas under the EU's revised steel safeguard framework. Demand from the Middle East remained weak due to ongoing geopolitical tensions, elevated freight costs, and shipping disruptions, which continued to weigh on market sentiment. However, export prices to both geographies were unchanged w-o-w.

Domestic-imported HRC differential: After witnessing a surge in May due to increased pipe and tube export demand, HRC imports seem to be edging down again as the spread with domestic prices remains considerable. For both the FTA countries and China, the differential with domestic HRC remained at INR 5,700-7,300/t in May, thereby discouraging imports.

Raw material prices soften: Imported coking coal prices into India dropped by $1/t w-o-w, although still remaining firm. Domestic iron ore prices, on the other hand, continued to soften, with BigMint's Odisha iron ore fines index (Fe 62%) declining by $1.5/t w-o-w on deteriorating steel market conditions.

Outlook

Long steel prices may remain under pressure ahead of and during the monsoon season due to direct impact on construction activity. Therefore, drawdown of inventory in the longs segment is expected to be slow, which will affect prices. The impact of volatile imported scrap prices due to currency depreciation has largely been offset by domestic scrap and the increased reliance on sponge iron. Therefore, the impact on prices is negated.

In contrast, flats are expected to remain somewhat stable due to a) firm coking coal prices, b) wide differential with landed costs of imports, c) domestic manufacturing momentum, and d) a possible short-lived uptick in exports in June ahead of EU quota implementation from 1 July as well as the downsizing of China's presence in key markets such as SE Asia and the Middle East.