BigMint's India steel index drops 1.1% w-o-w on weak construction demand, muted trade sentiment

...

- Rebar prices drop across regions amid accumulating inventory

- HRC prices range-bound, CRC drops INR 500/t (over $5/t) w-o-w

- BigMint's Odisha iron ore index drops INR 400/t post OMC auction

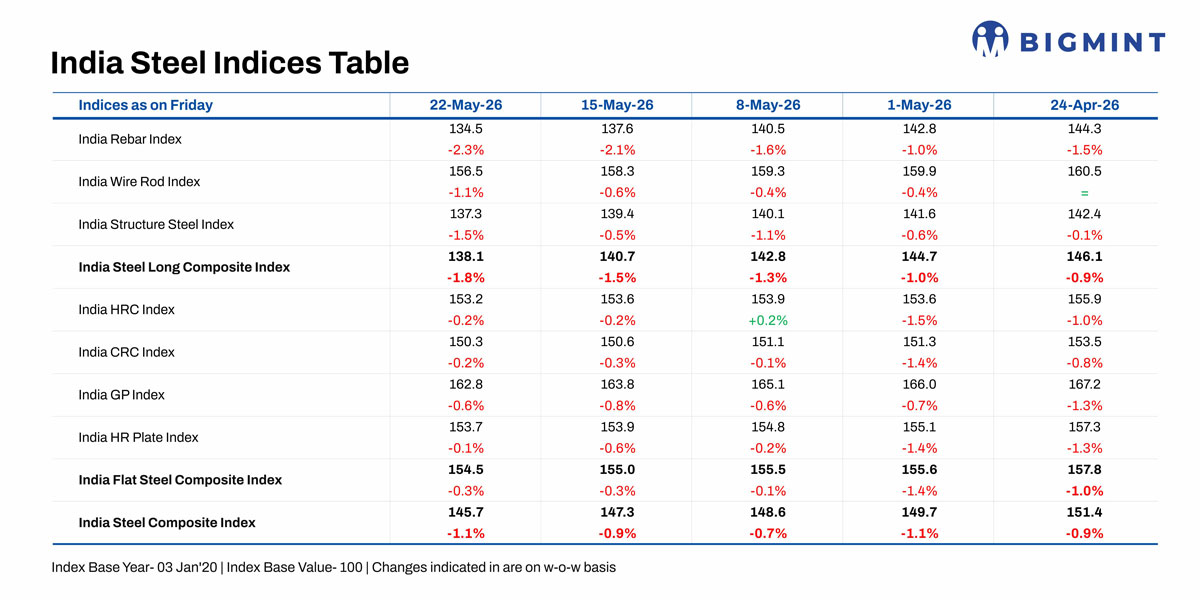

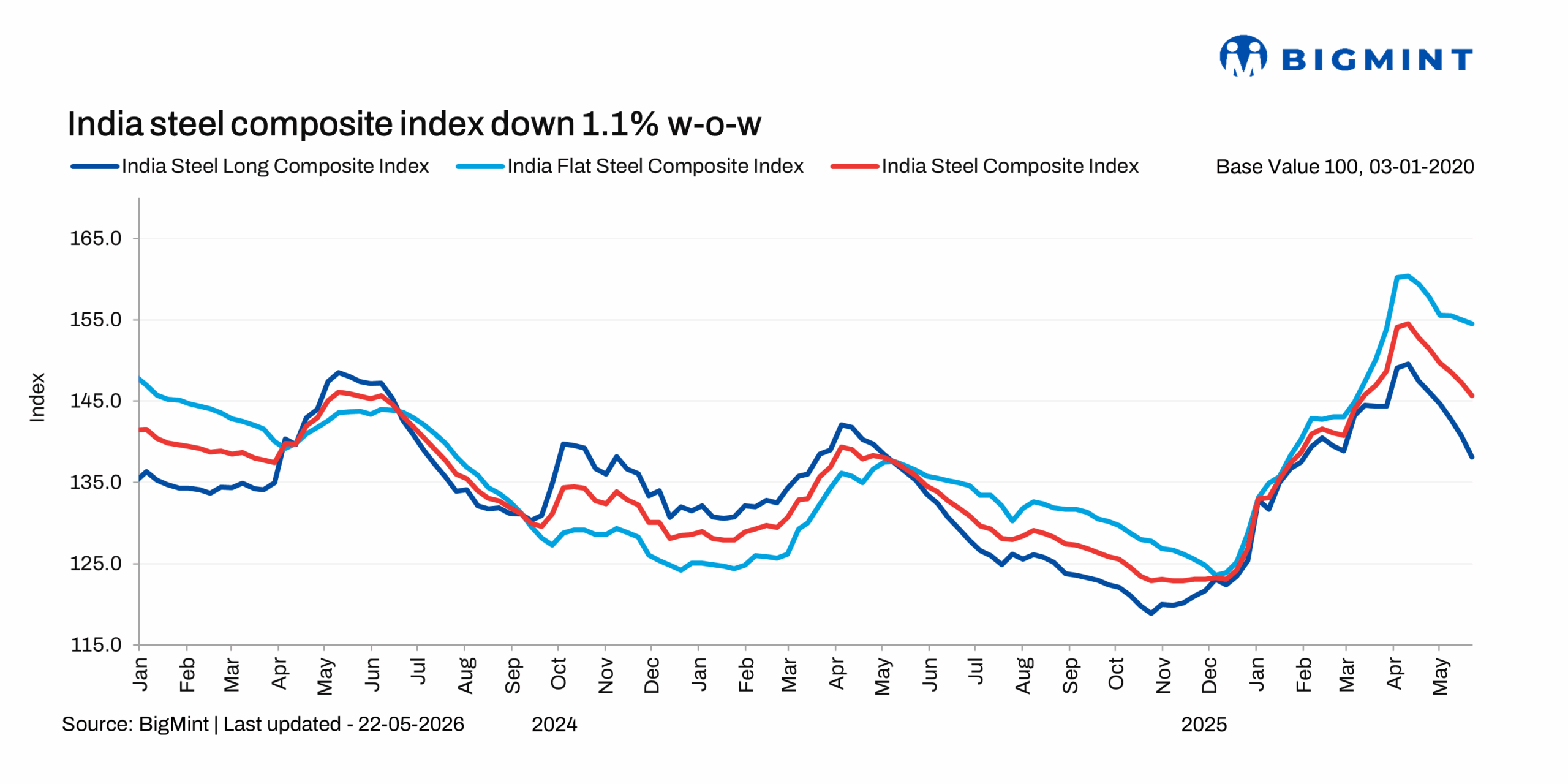

Morning Brief: BigMint's India steel composite index, a barometer of the domestic steel market, declined by 1.1% w-o-w, as assessed on 22 May 2026 last, on inventory build-up amid subdued trade channel demand and declining domestic iron ore prices. Weak construction sector sentiment due to the prevailing heatwave in many regions, and especially the dearth of labourers on site, impacted steel demand and prices in key regions.

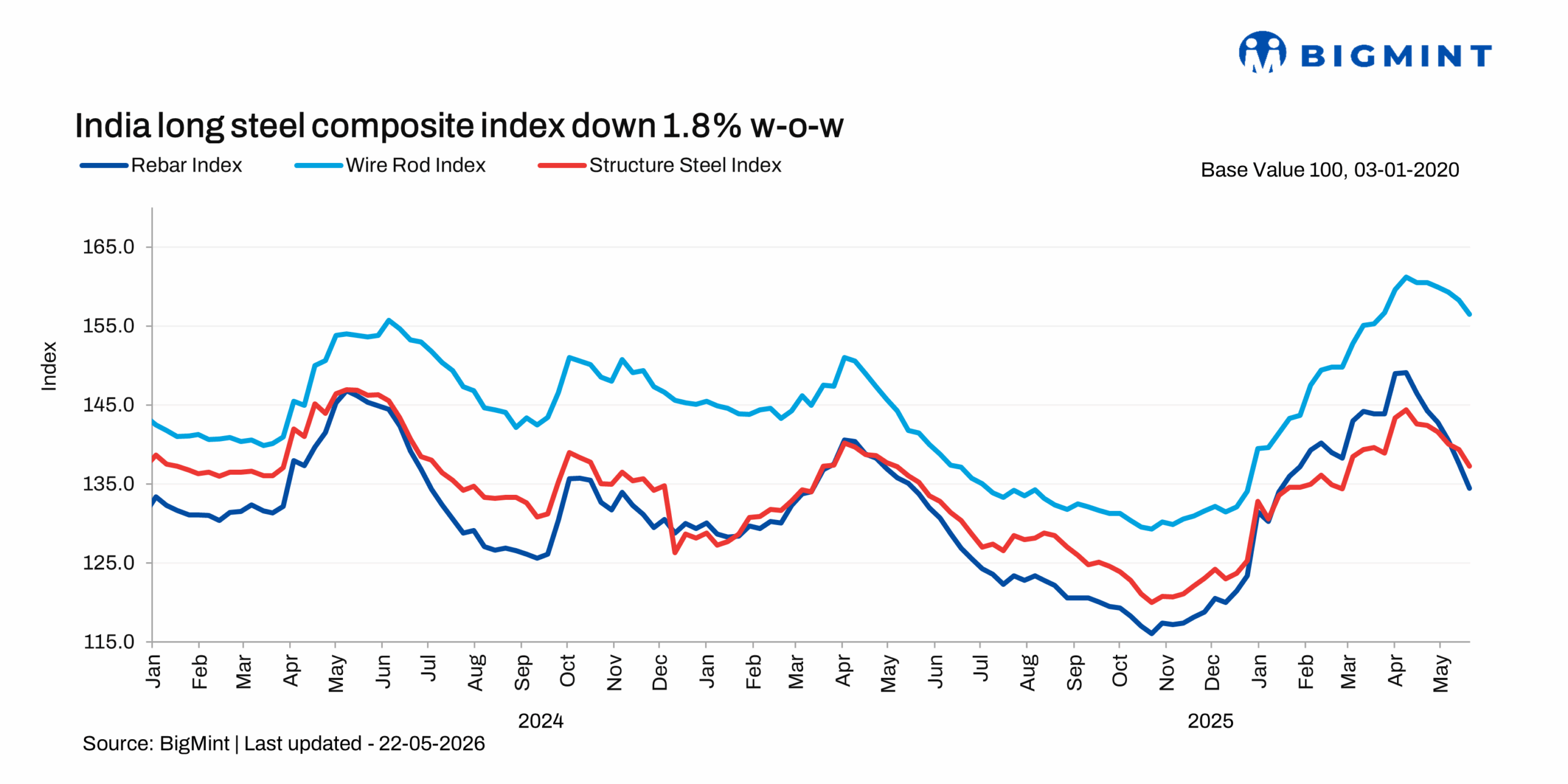

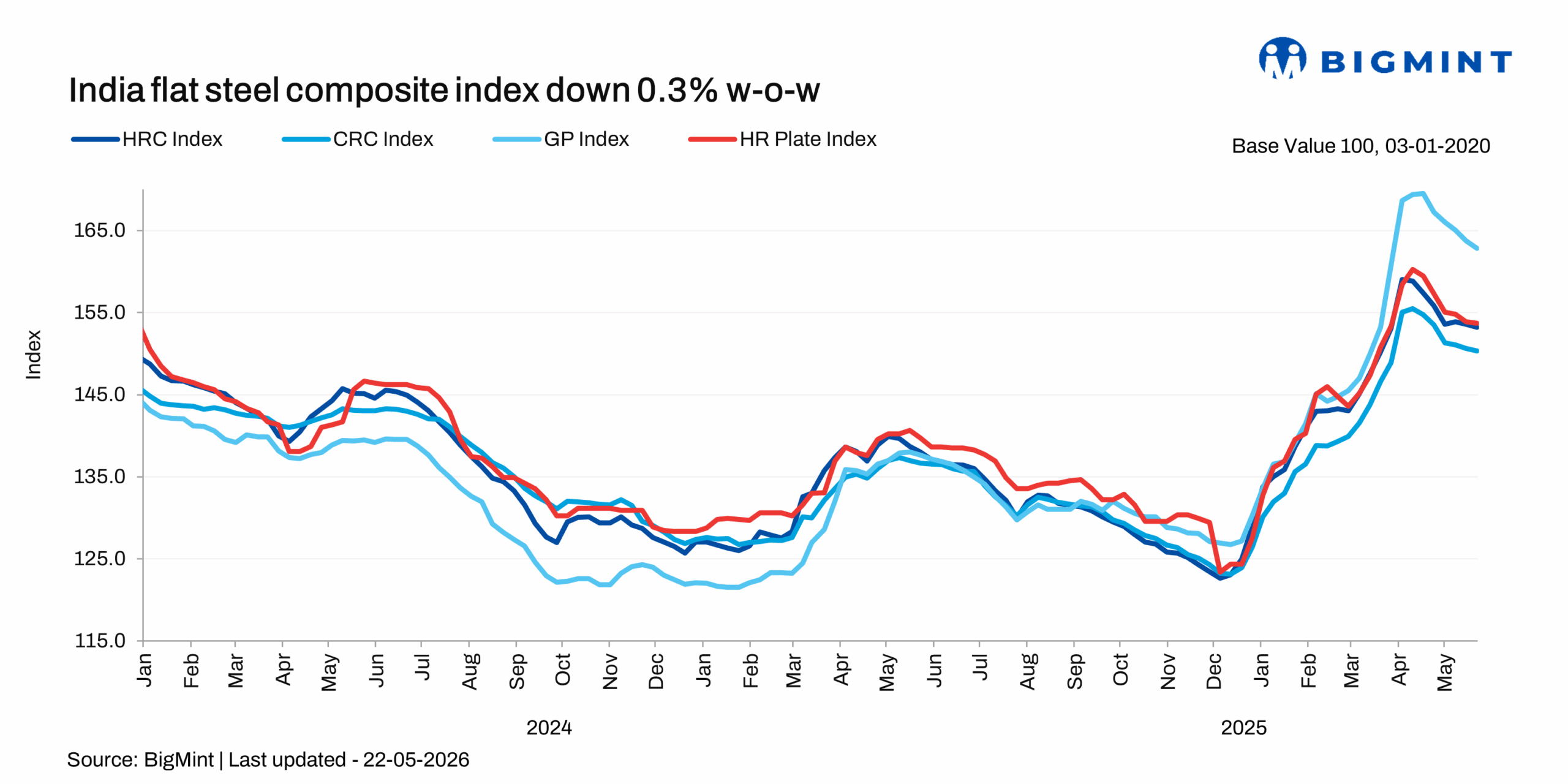

Weak construction sentiment weighed on long steel prices, BigMint notes, with the rebar index dropping sharply by over 2% w-o-w compared with just 0.2% for HRC. With the gradual moderation in energy and fuel supplies amid the temporary calm in the Middle East, domestic steel prices seem to have lost support.

Highlights of price movements

IF rebar weakens further: IF rebar trade prices declined across major markets. Trade activity remained subdued, with limited deal volumes reported. Demand continued to weaken, particularly in the finished and semi-finished steel segments, as buyers focused only on immediate requirements and maintained a cautious approach. Producers reduced offers and extended additional discounts to support material movement, while mill inventories were reported at around 8-12 days.

Market participants expect price volatility to persist amid weak bookings in the finished steel segment. Induction furnace (IF) rebar trade prices in Mumbai decreased by INR 500/t ($5/t) w-o-w to INR 46,800/t ($485/t) exw as of 22 May.

BF rebar trade prices drop: Trade-level BF rebar prices (distributor-to-dealer) edged down by INR 700/t ($7/t) w-o-w to INR 56,800/t ($592/t) exy-Mumbai. Buying activity was moderate across key regions, while demand in south India continuing to stay relatively weak, as per sources. Distributors maintained comfortable inventory levels, leading to need-based procurement amid limited construction activity. Market sentiment remained cautious-to-weak during last week.

The BF-IF rebar price spread in Mumbai narrowed further w-o-w to INR 10,000/t ($103). IF rebar continues to hold a dominant share in the Indian long steel market at approximately 65%.

HRC stable w-o-w, CRC edges down: BigMint's bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.58 mm/CTL) held stable w-o-w at INR 58,700/t ($612/t) as of 22 May. However, CRC (IS513, Gr O, 0.9 mm/CTL) prices decreased by INR 500/t ($5/t) to INR 65,000/t ($678/t) on 22 May from INR 65,500/t ($683/t) on 15 May.

Trade-level prices of HRC and CRC remained largely unchanged, reflecting the continued sluggishness in demand. Trading activity stayed subdued across markets, as buyers refrained from placing fresh bulk orders and limited their procurement strictly to immediate, needs-based requirements.

According to a market participant, "Demand remains extremely weak at present. There is some expectation of improvement once industrial production normalises with the return of labourers at factories and sites and the flow of fresh orders, but that remains speculative for now. The market will need to wait and watch how demand shapes up in the coming weeks."

Overall, the market sentiment continues to remain cautious-to-weak amid muted buying interest and uncertain near-term demand recovery prospects.

Iron ore softens, imported coking coal stable: BigMint's Odisha iron ore fines (Fe 62%) index fell by INR 400/t w-o-w to INR 5,100/t ($53/t) ex-mines following the latest auction by Odisha Mining Corporation (OMC), as lower bids compared to the April auction reflected weakening sentiments. The correction in iron ore prices comes amid a continuous decline in pellet, sponge iron, and semi-finished steel prices.

Imported coking coal prices, on the other hand, remained largely stable, increasing by just $2/t CFR India last week.

Outlook

Steel prices are expected to remain under pressure, correcting marginally this week on subdued trade sentiment. Heatwave conditions in many regions have impacted construction and availability of labour. Weakening raw material and semi-finished steel prices, too, are expected to weigh on steel prices. Coking coal prices may remain range-bound on consistent supply.

Steel prices, therefore, are expected to remain weak till green shoots of restocking demand emerge before the onset of monsoons, which is expected to be erratic this year. So, market uncertainty persists.