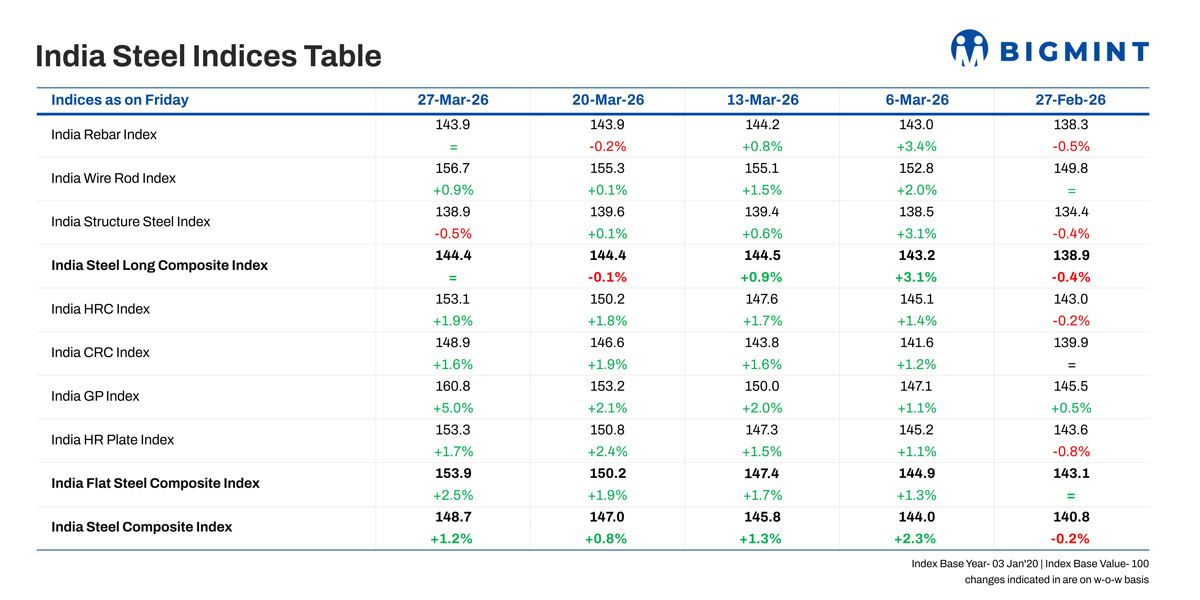

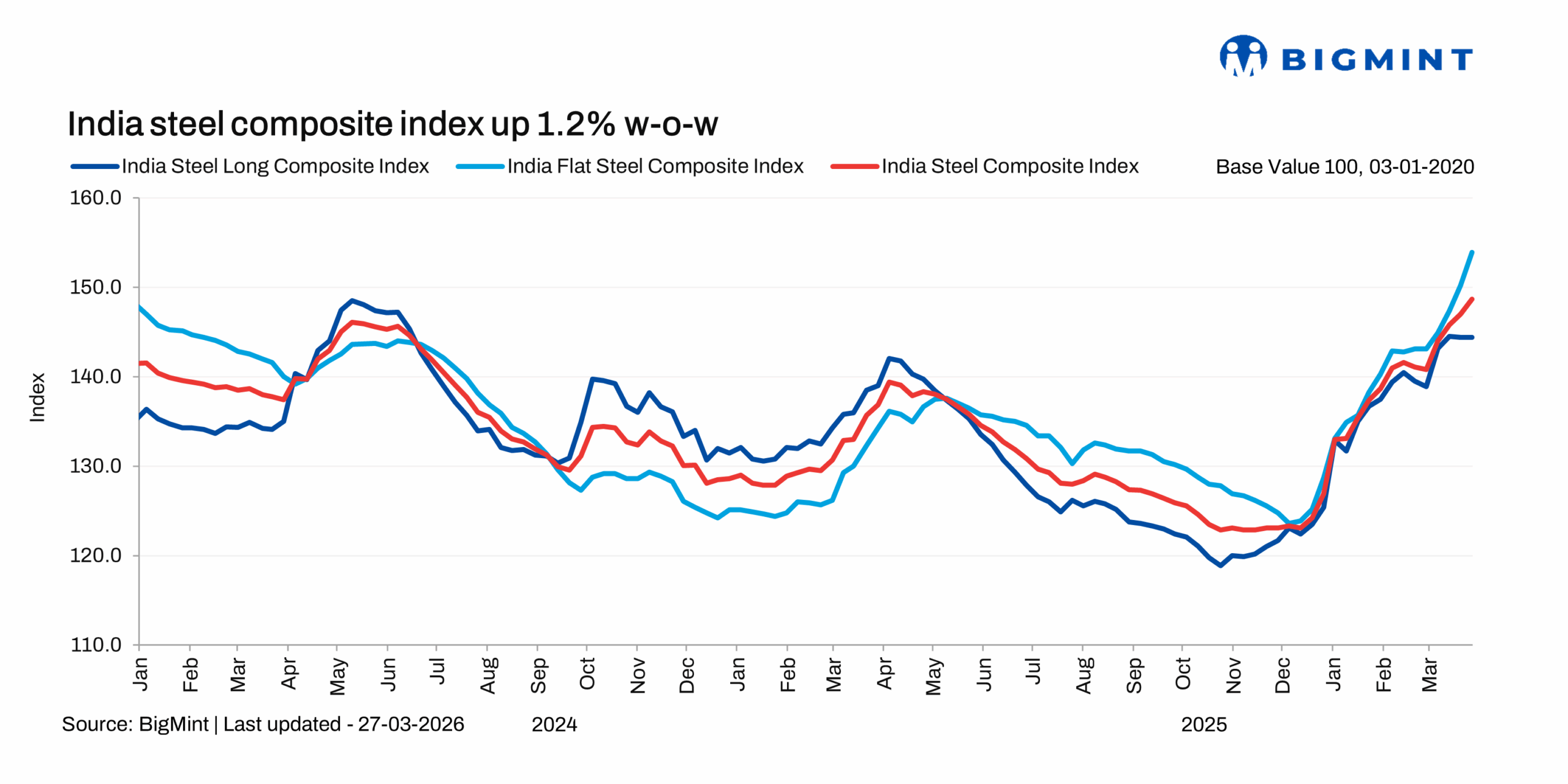

BigMint's India steel index rises 1.2% w-o-w as flats prices surge on tight supplies

...

- Benchmark HRC prices increase by INR 1,000/t ($11/t) w-o-w

- Major mills to take maintenance breaks in April

- Primary mills hike rebar prices further by INR 1,000/t ($11/t)

Morning Brief: BigMint's flagship India steel composite index continued to edge up w-o-w, as assessed on 27 March 2026 last, as tight supply, geopolitical uncertainties, rising freights, and higher raw material costs triggered buyer inquiries in the market. Primary mills raised key product prices, driven by elevated production costs.

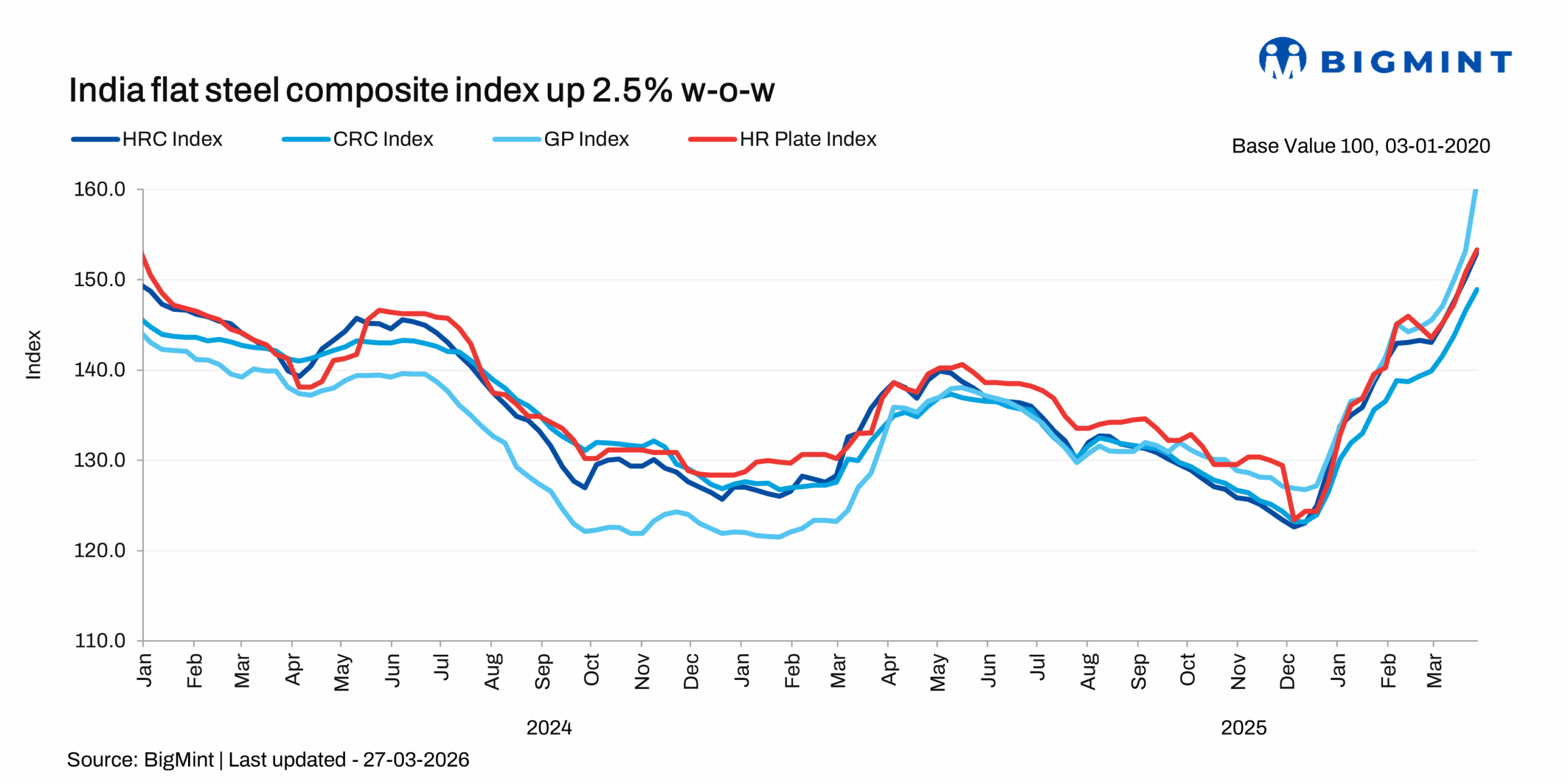

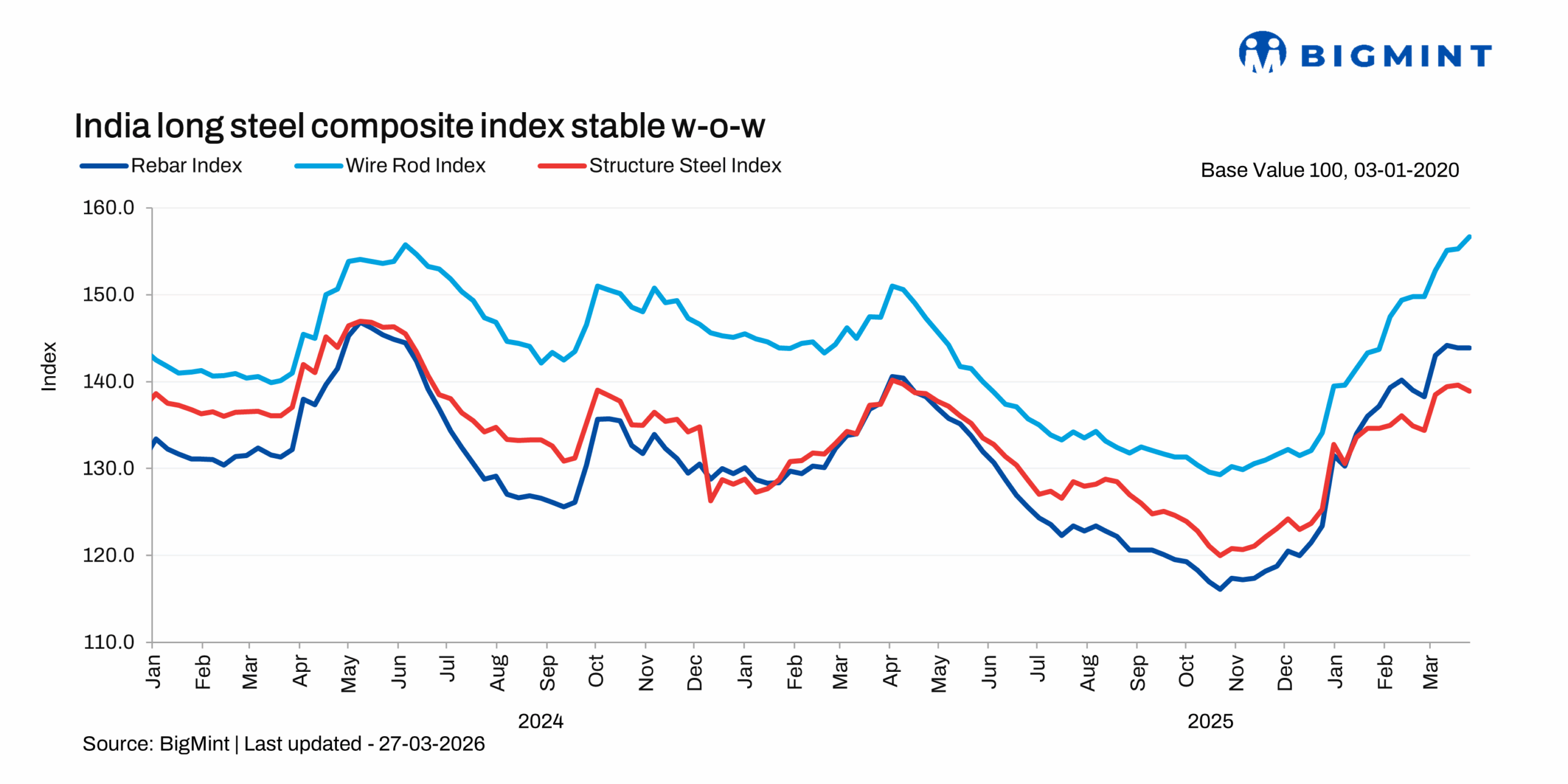

The flagship index rose by 1.2% w-o-w due to the flat steel composite index witnessing a sharp surge of 2.5% w-o-w. The longs index, however, remained flat despite the primary mills raising prices of rebar. However, demand-supply fundamentals remained largely unaffected. The price rise may be attributed more to restocking demand and cost pressures amid global uncertainties than any strong demand push.

Highlights of price movements

HRC trade prices witness upswing: BigMint's benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) prices increased by INR 1,000/t ($11/t) w-o-w to INR 57,500/t ($612/t) on 24 March against INR 56,500/t ($601/t) on 17 March.

CRC (IS513, Gr O, 0.9 mm/CTL) prices increased to INR 65,000/t ($692/t) as assessed on 24 March 2026, up by INR 2,200/t ($23/t) w-o-w against INR 62,800/t ($668/t) on 17 March. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

India's trade-level flat steel prices continued their upward momentum, with HRC prices holding near a 29-month high, with supply conditions tightening due to reduced imports and input constraints.

However, demand continues to be largely need-based, while some level of panic buying persists in the market amid supply concerns. Overall, trades remain limited, with a stable-to-moderate demand outlook.

Sources informed that if the geopolitical situation continues to escalate, further upward pressure on steel prices could emerge due to higher input costs, particularly for energy and logistics.

Major mills to undertake maintenance shutdowns: Additionally, planned maintenance shutdowns at some large integrated producers are expected to keep near-term availability tight in select regions. These are routine annual maintenance exercises, expected to last ten days in the first half of April.

Steel exports rise, imports decline in Jan-Feb'26: Indian steel exports surged 45% y-o-y to 1.68 million tonnes (mnt) in January-February, led by higher shipments to Vietnam and the UAE as EU demand softened. The rise was also supported by strong restocking in H2CY'25 ahead of CBAM, though momentum has started easing in early 2026.

India's steel imports fell 17% y-o-y to 1.27 mnt in January-February, mainly due to safeguard duty on flat steel and anti-dumping duties on Vietnamese material. Domestic HRC price hikes have narrowed the landed price gap, but import inflows remained weak amid limited buying interest.

IF rebar shows mixed trends, sentiments weaken: The IF-route rebar market exhibited a mixed trend w-o-w across major markets, indicating cautious sentiment. Trading activity remained moderate, with buyers largely purchasing material at lower price levels while showing resistance to higher offers. Demand continued to be predominantly need-based, limiting aggressive bookings. Manufacturers maintained relatively higher offer levels, supported by prevailing cost pressures, although selective discounts were extended to facilitate transactions.

BF rebar hiked further: The primary steelmakers increased rebar prices further by up to INR 1,000/t ($11/t) in the week ended 27 March. Post-revision, list prices stood at INR 59,500-61,000/t ($628-644/t) on landed basis. The price hike could be attributed to rising raw material prices and input costs and falling inventories. Rebar inventories at primary mills dropped further by 8-9% in end-March as against the beginning of the month, as per sources.

The BF-IF rebar price spread in Mumbai widened to around INR 9,500-10,000/t. IF rebar continues to dominate the Indian market, accounting for an estimated 65-70% share.

Slowdown in scrap imports expected to add to cost burden: Scrap imports are estimated to have declined sharply in March following higher shipping costs and market uncertainty. In February 2026, imports had already fallen to 0.34 million tonnes (mnt) compared to 0.76 mnt in February 2025 and 0.47 mnt in December 2025.

Buyers are increasingly relying on domestic scrap or alternative metallics instead of imported material. If this trend persists, raw material costs could stay elevated, particularly for mills that depend on imported scrap as a blending source, as reduced availability generally limits procurement flexibility and can support prices.

Outlook

Domestic steel prices are expected to stay firm amid the escalating West Asia conflict, shipping disruptions and high energy prices. However, lack of buyer acceptance and resistance are likely to weigh on the rebar and construction steel market. Likewise, the narrowing spread with landed cost of imports will definitely limit the ability of domestic mills to raise flat steel prices further.