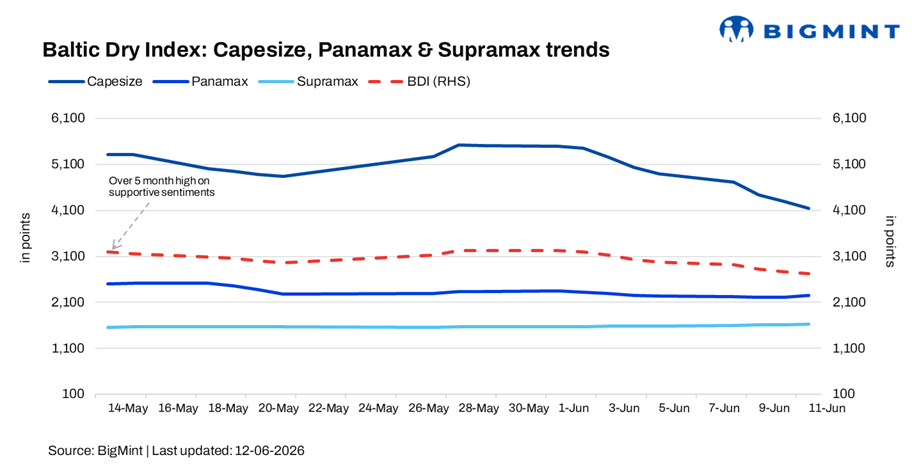

Baltic Dry Index falls for 10th consecutive session on Capesize weakness

...

- Weaker iron ore demand from China drags down the Capesize index

- Firm coal, grain shipments from Atlantic basin lift Panamax levels

The Baltic Exchange's Dry Bulk Index (BDI) fell for the tenth straight day by 1.52% d-o-d (42 points) to 2,729 points on 11 June 2026, reflecting mixed sentiment across vessel segments.

While gains in Panamax and Supramax segments highlight resilience in coal, grain, and minor bulk trades, the sharp decline in Capesize earnings, driven by weaker iron ore demand, outweighed these improvements, resulting in a lower overall BDI.

Segment-wise performance

- Capesize: The Capesize index fell by 3.74% (161 points) to 4,140 points, indicating bearish sentiment amid softer iron ore cargo volumes and reduced fixture activity on key Brazil-China and Australia-China routes. Cautious steel market conditions in China continued to weigh on demand.

- Panamax: The Panamax index rose by 1.81% (40 points) to 2,251 points, supported by firm coal and grain shipments, particularly from the Atlantic basin. Healthy cargo availability and steady vessel demand lent a bullish tone to the segment.

- Supramax: The Supramax index increased by 0.93% (15 points) to 1,633 points, reflecting stable demand for minor bulks. Meanwhile, improved regional trading activity across Asia and the Atlantic supported freight rates.

Outlook

Mixed dry bulk market fundamentals are expected to keep the BDI volatile this week, with firm Panamax and Supramax demand providing support, though Capesize performance remains the key determinant of overall market direction.

Additionally, bunker price volatility and vessel supply dynamics will remain key factors influencing freight market sentiment.