Australian high-CV coal prices fall on weak demand; Indonesian coal prices remain firm on supply constraints

...

- Australian high-CV coal prices dropped sharply amid weak buyer confidence

- Indian demand stayed weak as buyers preferred cheaper domestic coal

The Asian thermal coal market showed diverging trends in the week ending 10 April 2026, as weakness in Australian high-CV coal contrasted with firm Indonesian prices supported by supply constraints. The divergence reflects a split between cost correction in higher-grade material and supply-led support in lower grades, while demand across key markets remains subdued.

The Big Story: Australian Prices Correct as Demand Weakens

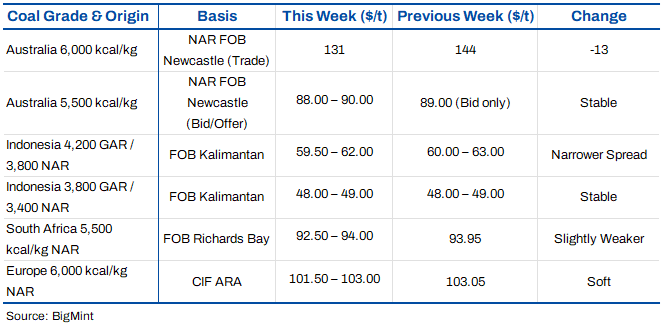

Australian high-energy coal prices declined sharply as weak buying interest reduced support for recent price levels. After trading around $144/t for June-loading cargoes, a 6,000 kcal/kg cargo for May delivery was concluded at $131/t FOB, with bids falling further to $128-130/t, indicating reduced buyer willingness to commit at earlier levels. The decline reflects weakening spot demand, particularly from China and India, as buyers remained cautious amid sufficient inventories and limited near-term requirements. The widening gap between bids and offers highlights a disconnect between seller expectations and buyer willingness, reinforcing downside pressure on prices. In contrast, the 5,500 kcal/kg segment remained relatively stable, as lower-grade material continued to find support from price-sensitive buyers.

Indonesia: Supply Constraints Support Prices

Indonesian coal prices remained firm as supply-side constraints limited availability despite subdued demand. The government's production quota approvals have reached around 580 million tonnes against a 600 million tonne target, but delays in approvals and higher domestic allocation requirements under revised Domestic Market Obligation rules have restricted export availability. As a result, several producers have limited or no spot cargo availability, tightening supply in the seaborne market. This has prevented prices from declining despite weak import demand from major buyers such as China and India.

China: Policy Signals Support Coal Preference

China remained selective in its seaborne coal purchases, with demand constrained by high domestic inventories and seasonal weakness. However, policy direction continues to favour coal over alternative fuels. In Guangdong province, authorities instructed power plants to increase coal stockpiles while reducing reliance on gas-fired generation, reflecting efforts to prioritise energy security amid volatile LNG prices and geopolitical risks. Gas consumption for power generation is expected to decline to 19 bcm from 21 bcm in 2025. While this shift supports underlying coal demand, immediate spot buying remains limited as domestic supply continues to meet requirements.

India: Weak Imports Despite Domestic Tightness Signals

Indian seaborne demand remained negligible as buyers stayed out of the spot market due to high import prices relative to domestic coal. Coal India's production declined 1.7% y-o-y to 768 million tonnes in FY'26, marking its first annual drop in four years. However, domestic availability remained sufficient, with industrial consumers preferring local procurement.

E-auction premiums rose to 45% in March from 35% in February, indicating strong domestic demand. However, this did not translate into import demand, as elevated seaborne prices continued to deter buying activity.

Southeast Asia: Regional Demand Supports Indonesian Market

Southeast Asian demand provided support to Indonesian coal prices, with buyers in Vietnam and the Philippines actively securing cargoes across multiple grades. This demand reflects energy security-driven procurement rather than opportunistic buying, with these markets remaining less sensitive to short-term price movements. As a result, regional demand has helped sustain Indonesian prices despite weak participation from larger importers.

Price Table

Outlook

The market remains split between supply-side tightness in Indonesian coal and weakening demand for higher-grade Australian material. Supply constraints, driven by production quotas and domestic allocation requirements, continue to support Indonesian prices, while weak spot demand is weighing on Australian high-CV coal.

In the near term, we expect Indonesian low- to mid-grade coal to remain supported in the $59-62/t range, as limited export availability offsets subdued demand. In contrast, Australian high-CV coal remains vulnerable to further correction if buying interest does not improve.

The key variable remains demand recovery from China and India ahead of the summer season. Until restocking activity emerges, the market is likely to trade sideways, with downside risk concentrated in higher-grade segments.