Aluminium scrap imports drop 16% y-o-y in Q1CY'26. Will India face tighter supplies in Q2?

...

- Weak rupee and LME prices raise costs

- Supply constraints expected to persist into Q2

- Domestic recyclers face rising raw material pressures

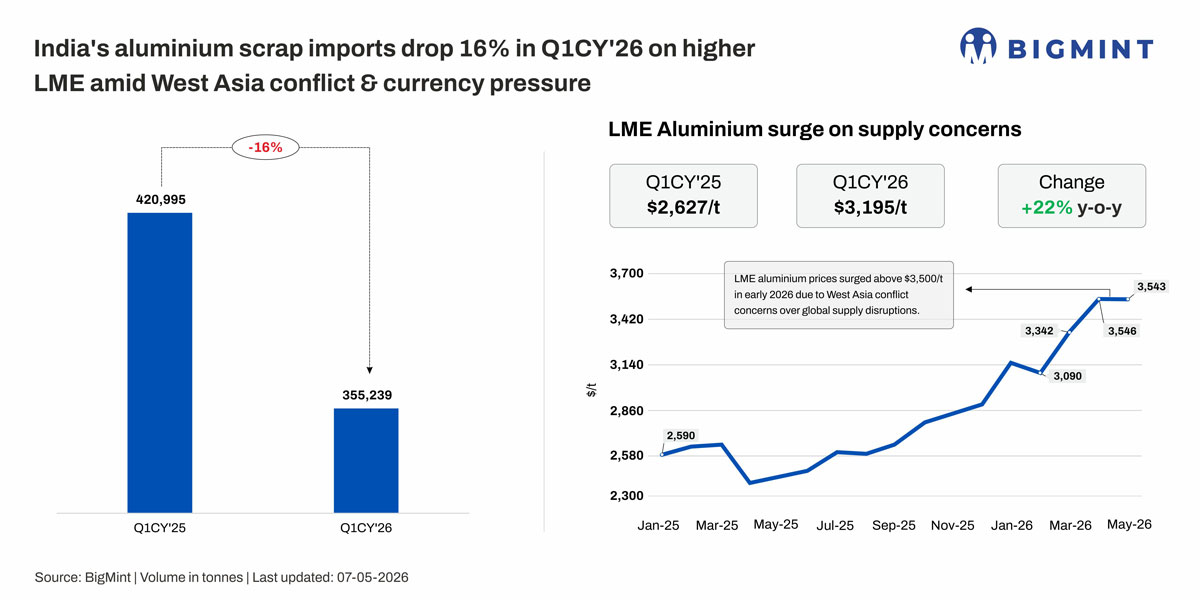

Morning Brief: India's aluminium scrap imports declined by 16% y-o-y to 0.35 mnt in Q1CY'26, down from 0.42 mnt in the corresponding period last year.

The country remains heavily dependent on imports, with nearly 85% of its aluminium scrap requirement sourced from overseas. As a result, the decline in arrivals has had a direct impact on domestic secondary producers, who rely on a consistent inflow of scrap to sustain production.

The downturn has been driven by a combination of volatile LME prices, constrained global supply, and currency pressures, which have elevated landed costs and weakened fresh booking activity. This situation has been further aggravated by escalating geopolitical tensions in the Middle East, which have disrupted key trade flows, increased freight and insurance costs, and tightened scrap availability from major exporting regions. As a result, supply to India has become more uncertain, while domestic prices have firmed in response to global cues.

Notably, India's aluminium scrap imports peaked at 0.2 mnt in October 2025, following which arrivals witnessed a steady decline, before dropping sharply to 0.1 mnt by March 2026. This trend highlights a marked slowdown in import volumes over the period.

Grade-wise & country-wise imports

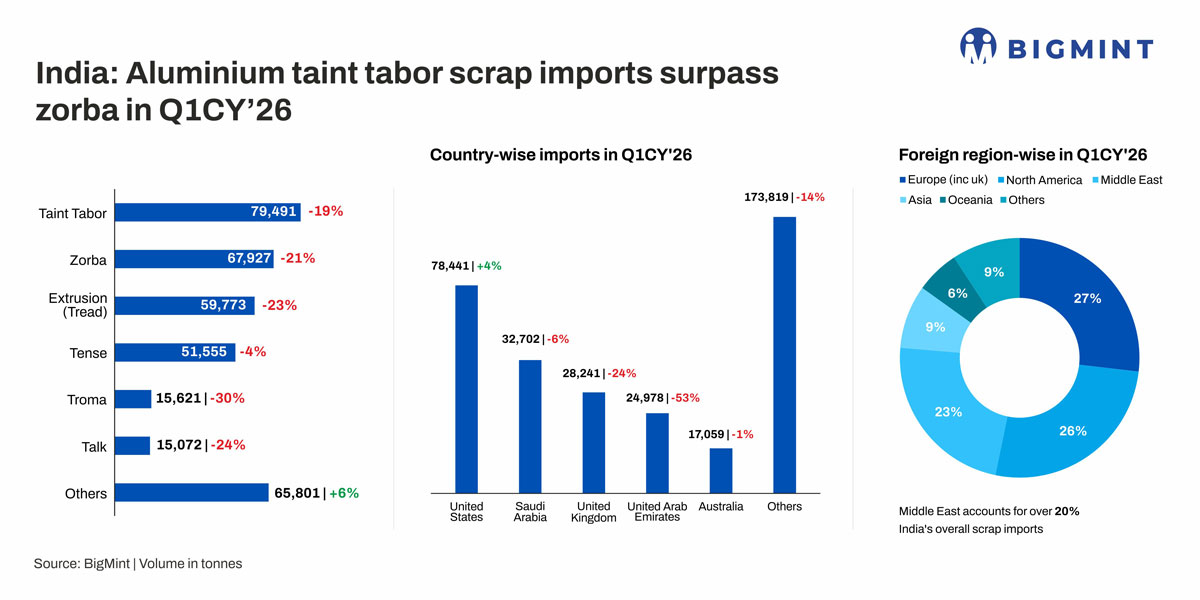

India's aluminium scrap imports were largely dominated by taint tabor and Zorba, which remained the most imported grades in Q1CY'26 despite witnessing notable declines of 19% y-o-y and 21% y-o-y, respectively, significantly impacting overall volumes. Among all grades, troma recorded the steepest decline at 30% y-o-y, followed closely by zorba and extrusion, indicating sharp weakness in mixed and processed scrap inflows.

India's aluminium scrap import basket witnessed a sharp country-wise reshuffle in Q1CY'26, with the UAE recording a steep 53% y-o-y decline, followed by notable drops from the UK (24% y-o-y) and Saudi Arabia (6% y-o-y), while supplies from the US remained largely stable and Australia posted modest growth.

Meanwhile, India's aluminium scrap imports saw a further decline in March, reflecting growing supply pressure from escalating geopolitical tensions in the Gulf. In 2025, India imported nearly 2 mnt of scrap, with nearly 0.47 mnt (25%) coming from the UAE and Saudi Arabia, highlighting high dependence on Gulf-origin material.

Rising disruptions linked to the US-Israel-Iran tensions have affected key shipping routes, especially around the Strait of Hormuz, leading to vessel delays, rerouting, and higher freight and insurance costs (insurance up 100-200%, freight charges above $3,000 per 40 ft container). This has tightened scrap availability and slowed bookings in March.

The UAE remains the most significant supplier for India, followed by Saudi Arabia, making the region's stability critical for India's secondary aluminium industry. China remains relatively insulated due to strong Russian inflows, but global supply stress continues to impact India's import flows indirectly.

On the other hand, in Q1CY'26, aluminium scrap arrivals saw a decline across all regions. The north was hit the hardest, with a 26% drop, bringing volumes down to 136,540 t. The south and east also saw noticeable declines of 11% and 31%, with arrivals at 67,737 t and 11,211 t respectively.

The west, however, stood out by staying largely stable, seeing a slight decrease of 3%, with volumes at 139,752 t.

What affected scrap imports in Q1CY'26?

Price trends

Aluminium markets showed a clear upward bias in Q1CY'26, supported by tighter fundamentals and elevated geopolitical risk. LME aluminium prices rose by $568/t y-o-y, reaching an average of $3,195/t in Q1CY'26 versus $2,627/t in Q1CY'25. At the same time, LME inventories declined by around 14% y-o-y, falling to 0.47 mnt from 0.55 mnt, reflecting tighter visible supply conditions in the physical market.

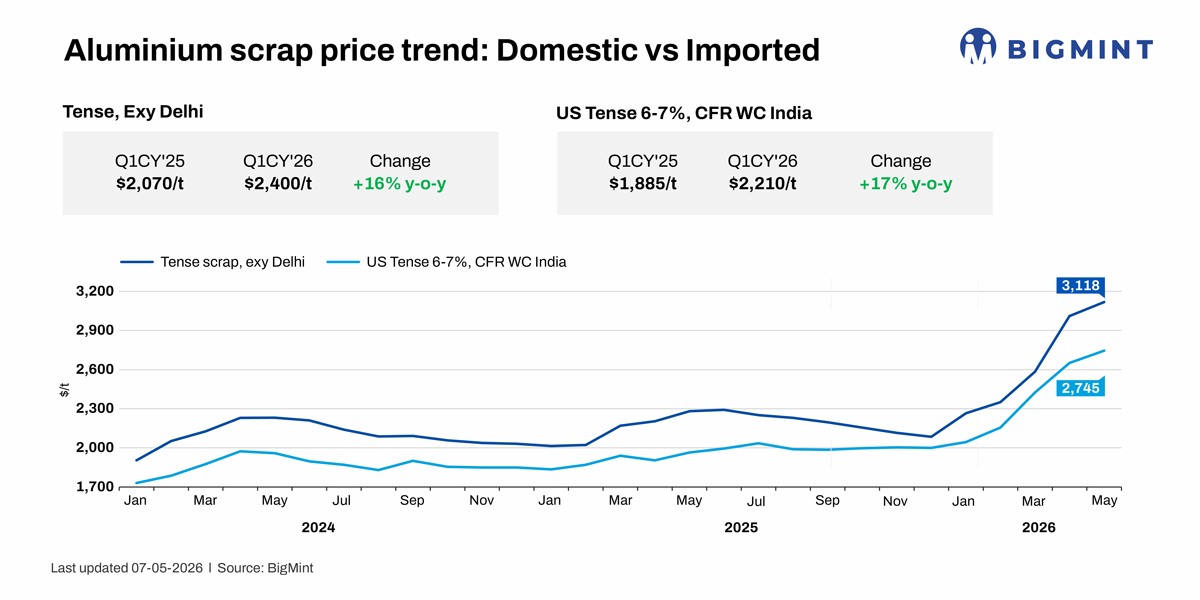

This strength also transmitted into the scrap segment, with both imported and domestic scrap prices moving higher in line with LME trends. For instance, US tense (6-7%) scrap was assessed at $2,210/t CFR West Coast India in Q1CY'26, up 17% y-o-y from $1,885/t in Q1CY'25, indicating firm international scrap demand and tighter supply conditions.

Within Q1CY'26, LME aluminium experienced extreme intra-quarter volatility driven by escalating US-Israel-Iran tensions and repeated disruptions in the Gulf, which contributes around 8% of global primary aluminium output. Prices during early-March stood in the $3,240-3,300/t range before surging above $3,500/t in mid-March on fears of Strait of Hormuz disruptions and supply risks.

This rally reversed sharply on 19 March when prices fell more than 8% in a single session to around $3,115/t, marking the steepest daily decline since 2018. The correction was driven by a broader macro risk-off sentiment, including concerns over global growth slowdown and liquidation of long positions across commodities.

Volatility persisted thereafter, with prices rebounding around 30 March 2026 by ~6% to near $3,492/t after renewed reports of Iranian strikes on Gulf production assets, reviving supply disruption concerns. Particularly after reported operational impacts at key producers including Emirates Global Aluminium (Al Taweelah, ~1.6 mnt capacity) and Aluminium Bahrain (Alba) following missile and drone strikes.

In line with higher global benchmarks, domestic scrap markets also strengthened. Delhi-based tense scrap prices increased by 16% y-o-y to $2,400/t in Q1CY'26, compared with $2,070/t in Q1CY'25, largely supported by tighter domestic availability and firm import parity. Overall, both primary aluminium and scrap markets reflected a structurally tighter environment, with volatility amplified by geopolitical disruptions and fluctuating sentiment in March.

Exchange rate

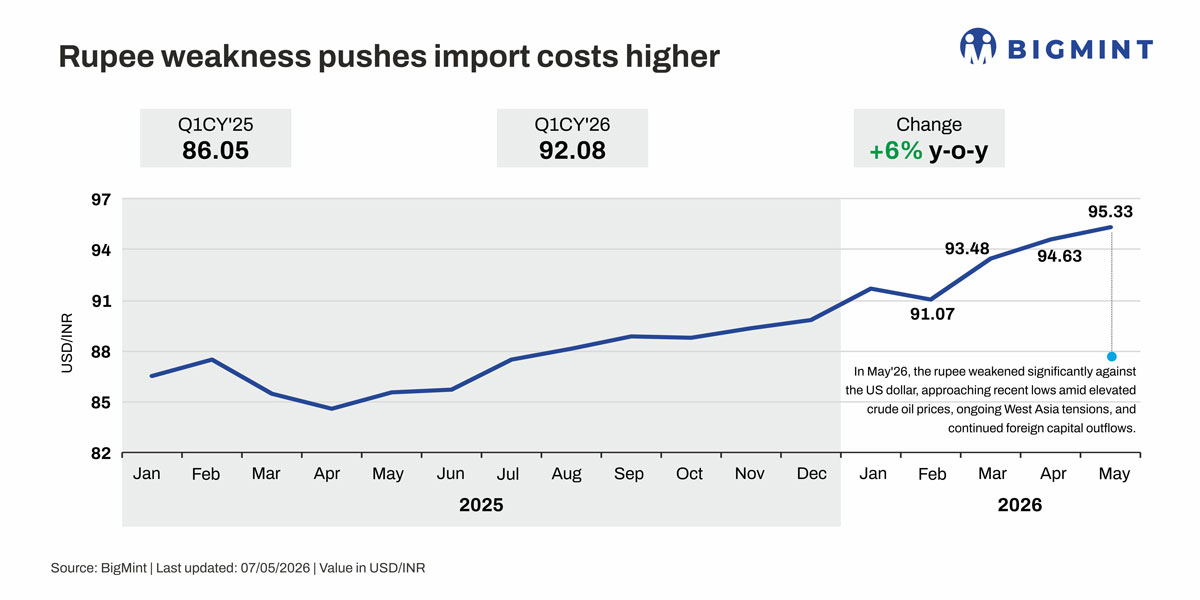

India's currency market witnessed heightened volatility as the rupee weakened sharply, crossing the 95 per US dollar mark for the first time, and closing at a record low of around 94.83-95.14 levels during late March. The currency recorded its fourth consecutive weekly decline, marking one of its steepest depreciations since 2011-12. The move came amid persistent foreign outflows, rising crude oil prices, tighter forex conditions, and RBI measures to curb volatility, all of which contributed to amplified swings in the currency market.

India's heavy reliance on imports makes the rupee's movement a key factor in aluminium scrap trade. As the rupee weakened by over 6% in 2025 and continued to depreciate further into early 2026--now breaching the 95/USD level--import costs rose sharply. This was compounded by elevated LME prices, making aluminium scrap significantly more expensive for domestic buyers on a landed basis. As a result, many buyers have curtailed or delayed fresh bookings, contributing to the decline in aluminium scrap imports during Q1CY'26.

Strong demand

The sustained decline in aluminium scrap arrivals since October 2025, extending into early 2026, has significantly tightened domestic availability. Given India's near 85% import dependence for aluminium scrap and limited domestic generation of around 0.2 mnt annually, the fall in imports has materially constrained supply. This has led secondary producers to increasingly rely on local sourcing, thereby supporting higher domestic scrap prices.

At the same time, demand for ADC12widely used in the automotive sector--strengthened further, underpinned by steady OEM production and healthy downstream consumption. Since ADC12 is produced from scrap grades as tense and zorba, improved automotive demand, supported by GST-driven consumption momentum since September 2025, has further lifted scrap usage.

However, the market is simultaneously facing an acute shortage of tense scrap, which has tightened feedstock availability, restricted blending flexibility, and intensified cost pressures across secondary producers. This imbalance has also widened the gap between supplier expectations and OEM bids, as buyers continue to resist elevated offers amid rising input costs.

Overall, the combination of constrained supply and robust downstream demand has kept aluminium scrap prices firm in the domestic market.

What lies ahead?

The continued West Asia conflict, which escalated from late February into Q1CY'26, has caused sustained disruption across global trade flows, particularly in metals such as aluminium. With the GCC region accounting for nearly 8-9% of global primary aluminium output, ongoing instability has significantly impacted market sentiment and supply expectations. The disruption of key maritime routes, including the Strait of Hormuz, has affected both inbound and outbound cargo movement from the region, leading to irregular shipment flows.

As a result, LME aluminium prices experienced sharp volatility during March, briefly breaching $3,500/t. Scrap markets were simultaneously affected, as Middle East-origin flows slowed due to port disruptions, and rerouted cargo meant higher freight and insurance costs, which increased overall landed costs and restricted fresh offers into key Asian markets, including India.

Globally, scrap availability has remained structurally tight as several exporting regions increasingly diverted material to domestic consumption amid stronger local demand and evolving trade policies. This has contributed to firmer scrap pricing across major origins and reduced export availability.

Even if the West Asia conflict comes to an end tomorrow, the ripple effect of the war is expected to stay for a while.

As per market feedback, it was heard a few ports like Khor Fakkan in the Middle East have started operations. However, there is still a notable delay due to port congestion.

For India, the impact has been more pronounced given its high import dependence. Scrap arrivals, which had already declined steadily through late 2025, remained weak into Q1CY'26, tightening domestic availability further. With import inflows continuing to remain subdued since January, supply conditions are expected to stay constrained into Q2CY'26. While domestic secondary producers are increasingly relying on locally available scrap, this shift has further supported domestic scrap prices, keeping overall cost pressures elevated across the value chain.

How will global aluminium scrap trade evolve in H2 CY'26 and what will be the continued ramifications of geopolitical conflict in the Middle East? How are domestic end-users looking to address the challenge of growing scrap availability? Hear experts deliberate on the evolving dynamics of the aluminium scrap market at BigMint India Non-Ferrous Week (BINFW) to be held over 9-10 June 2026 in Mumbai, India.