14-March-2026

- Around 80% of emissions are from captive thermal power

- India much lower than global average energy and CO2 intensity

- CCTS targeting incremental emissions reduction from primary production

Morning Brief: India is the second largest aluminium producer in the world after China, with production reaching over 4.2 million tonnes (mnt) in 2025, as per BigMint data. Around 70-75% of India's production comprises primary aluminium -- a process of extracting and refining bauxite into alumina first and then smelting that alumina into liquid aluminium metal.

This primary process of production, as opposed to production of metal with recycled content, is highly energy and emissions intensive. In fact, scrap-based production requires just 15% of the total energy consumed in primary production.

According to the Bureau of Energy Efficiency (BEE), the embodied energy for aluminium is 211 gigajoules per tonne (GJ/t) of aluminium compared to 22.7 GJ/t for steel. However, since aluminium is much lighter than steel, the energy savings accrued during its lifetime of end use is actually three times higher that of steel.

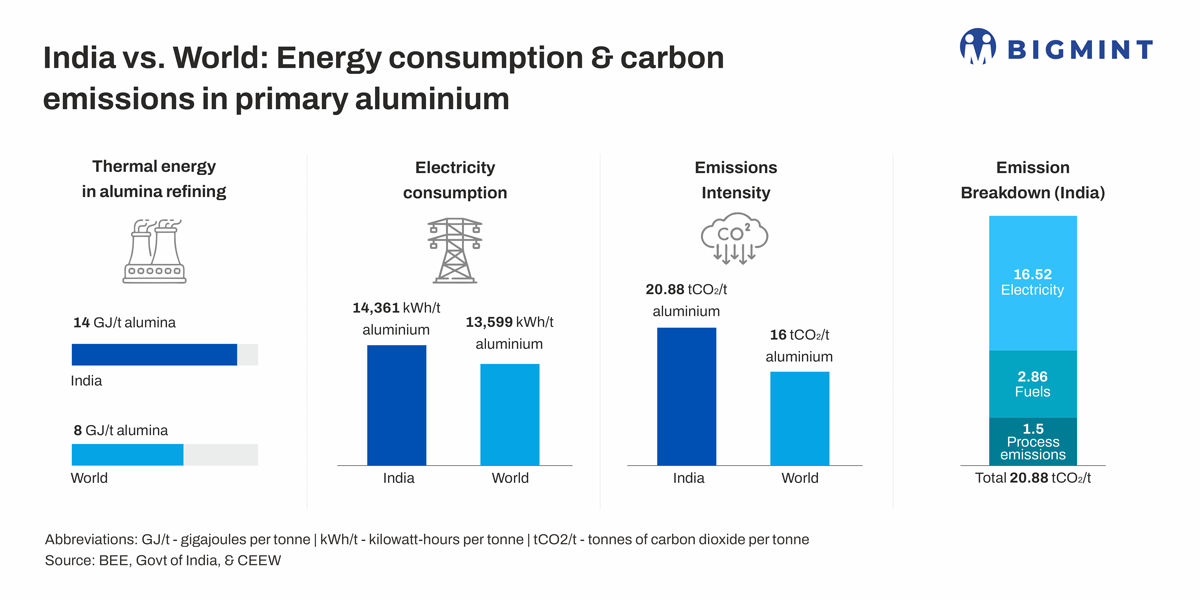

Indian scenario

According to a study by the Council on Energy, Environment and Water (CEEW), the Indian aluminium industry emitted nearly 77 mnt of CO2 in the year 2019-20 (with total production largely around the same level as today), and electricity consumption accounted for 80% of the total, while process emissions and fuel consumption accounted for the rest of Scope 1 and 2 emissions.

Mainly only thermal energy is used in the alumina refining process. For alumina refining, the Indian average energy consumption is 14 GJ/t of alumina, whereas the global best is 8 GJ/t. The average electricity consumption in India and the global achievable best are relatively similar. The average electricity consumption in India is 14,361 kWh/t of aluminium, whereas the global best is 13,599 kWh/t of aluminium.

Emissions intensity

While studies show that the Indian primary aluminium producers have an average emissions intensity of around 18-20 tCO2/t of aluminium, the global average is much lower at around 15-16 tCO2/t of aluminium.

The carbon intensity of the top 13 primary aluminium producers (contributing ~40% to total global production) show that companies operating in developed nations have already shifted to lower carbon power such as hydropower and solar, resulting in almost 50-60% lower emission intensity than those operating in developing nations. India's average carbon intensity is around 18-20 tCO2e/t of aluminium, owing to usage of coal linkage and captive coal mines.

Considering that 80% of emissions are due to electricity use in aluminium smelting, the transition to renewables is of critical import for the domestic aluminium sector.

Policies and regulations

The EU's Carbon Border Adjustment Mechanism is in force, levying carbon costs on imported aluminium. However, Indian producers are not greatly affected as electricity-related emissions are outside the purview of CBAM emissions calculations. The EU's share in India's aluminium exports is roughly 25%.

India's 'Greenhouse Gas Emission Intensity Target Rules (2025)' impose legally binding CO intensity reduction targets on aluminium producers from 2025, requiring a 2.8%-7.1% reduction in CO2 per tonne under the Carbon Credit Trading Scheme (CCTS). This might appear to be too low on ambition in terms of CO2 reductions; however, incremental carbon reduction targets may add up to significant reductions.

India has introduced measures to enhance scrap recycling to produce secondary aluminium. In addition, the Perform Achieve and Trade (PAT) scheme has driven significant energy efficiency improvements in the aluminium industry, achieving cumulative energy savings of 2.13 million tonnes of oil equivalent.

Rapid decarbonisation of the sector is possible through clean power procurement, expanded recycling, and the deployment of inert anode and CCUS technologies. Some studies show that carbon abatement at current costs could raise prices by as much as 60%. However, the rapid scaling up of RE and green biofuels as well as energy efficiency measures will gradually lead to significant reductions in C02 mitigation and removal costs.

BigMint is hosting BigMint India Non-Ferrous Week on 9-10 Jun'26 in Mumbai, bringing together stakeholders from the non-ferrous metals and recycling value chain to discuss market outlook.