IMPORTANT ANNOUNCEMENT !!

BINFW 2026 which was earlier scheduled for 9-10 June, in Mumbai will now be presented under the umbrella of Global Commodity Conclave, powered by MCX — India’s leading commodity exchange and co-powered by BigMint from 12–14 August 2026 at the JIO World Convention Center, Mumbai.

While BINFW will continue to retain its strong non-ferrous focus, identity and dedicated agenda, this integration significantly elevates the scale of participation, institutional engagement and cross-commodity collaboration across the ecosystem.

1000 + Participants

80 + Speakers

35 + Exhibitors

3 Days

For businesses and participants across the value chain, this will enable:

- Wider networking opportunities

- Access to sessions across Non-Ferrous, Agri, Bullion & Energy

- Deeper market and trade insights

- Stronger industry and institutional participation

For already confirmed participants:

- Your registrations remain intact

- Conference now expands to 3 days (12–14 August 2026) from the earlier 2-day format

- Venue: Jio World Convention Centre, Mumbai

- Access to all other commodity sessions as well

Updated schedules and session details will be shared shortly.

We sincerely thank all delegates, speakers, sponsors and partners who have already confirmed their participation and support for BINFW 2026.

For any assistance regarding participation, schedules, speaking opportunities, sponsorships, exhibition or event updates, please feel free to connect with our team.

About The Conference

BigMint India Non-Ferrous Week is a premier industry forum designed to bring the entire non-ferrous value chain together producers, recyclers, traders, policymakers, technology providers, and end-use manufacturers. The event explores how aluminium, copper, zinc, lead, nickel, tin, and other non-ferrous metals are shaping India’s industrial growth and how global market forces are reshaping trade flows, pricing, and investment decisions.

India is rapidly evolving into a major hub for both primary and secondary non-ferrous metals. As demand expands across infrastructure, automotive, mobility, power equipment, renewables, electronics, and consumer applications, the sector is entering a new phase of complexity and opportunity. The conference will unpack these shifts, connecting long-term market drivers with the realities on the ground supply gaps, raw material constraints, regulatory transitions, technology adoption, and the growing need for reliable pricing and intelligence.

Designed as a platform for practical insights and meaningful dialogue, the event offers a mix of strategic outlooks, data-backed discussions, and case-led sessions. The conversations will highlight how global trade realignments, decarbonization pressures, policy reforms, and digital transformation are influencing decisions across the non-ferrous ecosystem. Through these discussions, the event aims to help businesses plan for the next decade with clarity and confidence.

Objective

The objective is to build a strong, connected non-ferrous community and offer a dedicated space where industry participants can exchange knowledge, explore market opportunities, and collaboratively address challenges. The forum is structured to help stakeholders understand market developments, identify actionable strategies, and align long-term plans with India’s emerging opportunities.

Conference Highlights

- Data-backed insights on global and Indian demand, supply, and pricing across key non-ferrous metals.

- Understand the impact of tariffs, trade policies, and global market shifts on Indian operations.

- Practical strategies for procurement, sourcing, and inventory optimization.

- Expert forecasts to navigate price volatility, raw material risks, and market cycles.

- Deep dive into decarbonization, recycling, and green-metal opportunities.

- Policy intelligence on EPR, PLI, GST, mining reforms, and regulatory shifts.

- Technology-led pathways through AI, automation, and digital plant integration.

- Networking platform for new partnerships across producers, recyclers, traders, and downstream industries.

Big Questions Shaping the Future of the Metals Ecosystem

1. How rapidly are non-ferrous metal applications evolving across energy, mobility, and technology?

2. Can India secure reliable, long-term supplies of concentrates, alumina, zinc ore, scrap, and critical minerals?

3. Will circularity, EPR policies, and integrated scrap ecosystems effectively bridge supply gaps?

4. How quickly can India scale value-added products, alloys, and downstream capabilities?

5. Which pricing benchmarks and hedging tools will best manage rising market volatility?

6. Can domestic mining expansion and new offtake partnerships align with India’s Vision 2047?

7. What strategic role will India play in the emerging global green-metal supply chain?

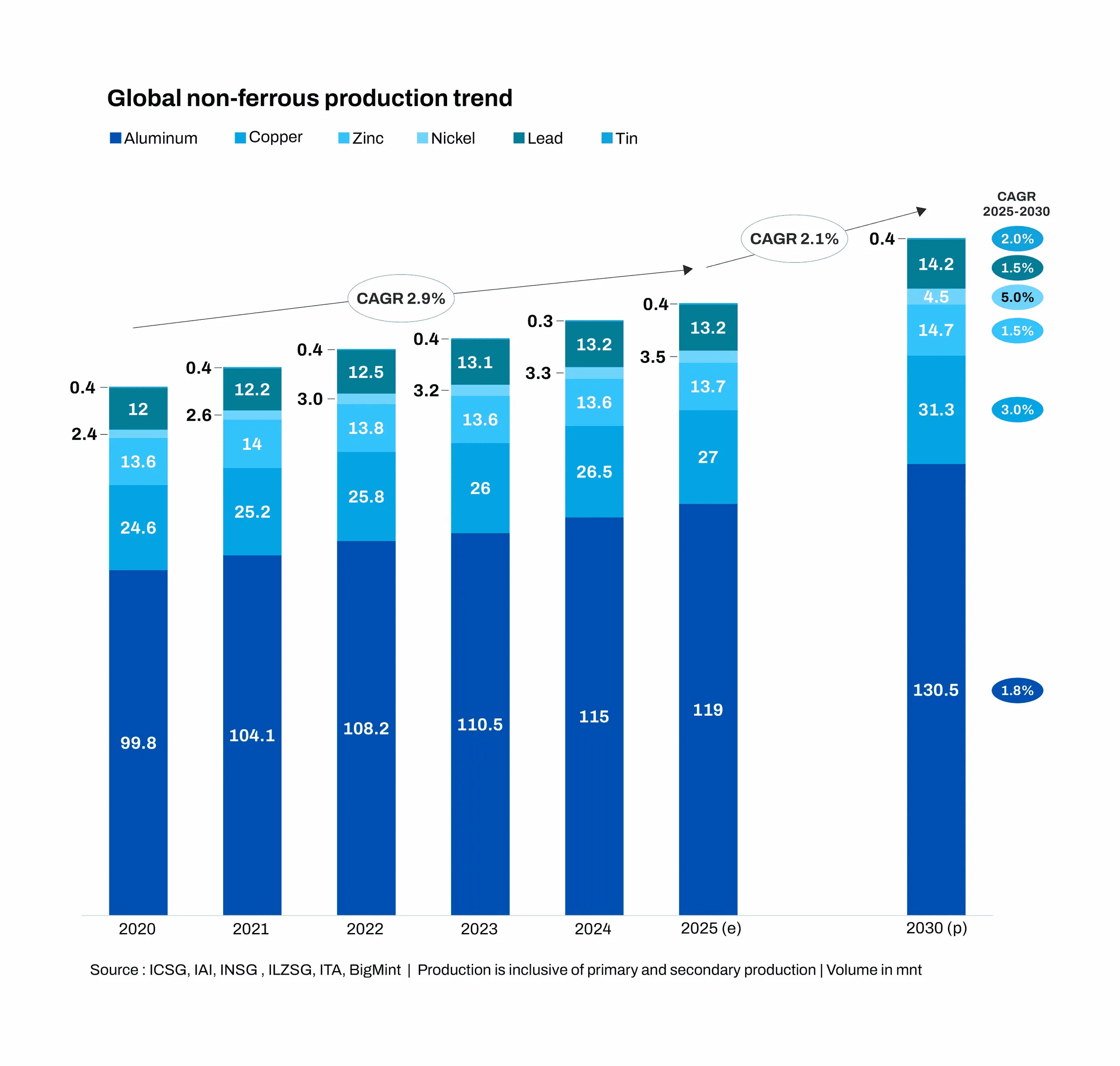

Aluminium, copper, zinc, and lead are increasingly shaping the materials landscape of the future. Their versatility and performance characteristics make them indispensable across modern industrial value chains, especially as global markets push toward high-efficiency and low-carbon solutions.

Driven by advancements in energy systems, sustainable mobility, expanding infrastructure, and emerging technologies, these non-ferrous metals are finding broader and more sophisticated applications. From electric vehicles and renewable grids to smart infrastructure and advanced manufacturing, their relevance continues to deepen.

As industries accelerate their shift toward innovation and sustainability, the strategic importance of these metals is becoming more pronounced. Their role in enabling cleaner energy, efficient transportation, and resilient infrastructure highlights their growing impact on global development.

With this transformation underway, demand for aluminium, copper, zinc, and lead is expected to rise steadily in the coming years. Their critical role in powering next-generation systems positions them as essential drivers of industrial growth and technological progress worldwide.

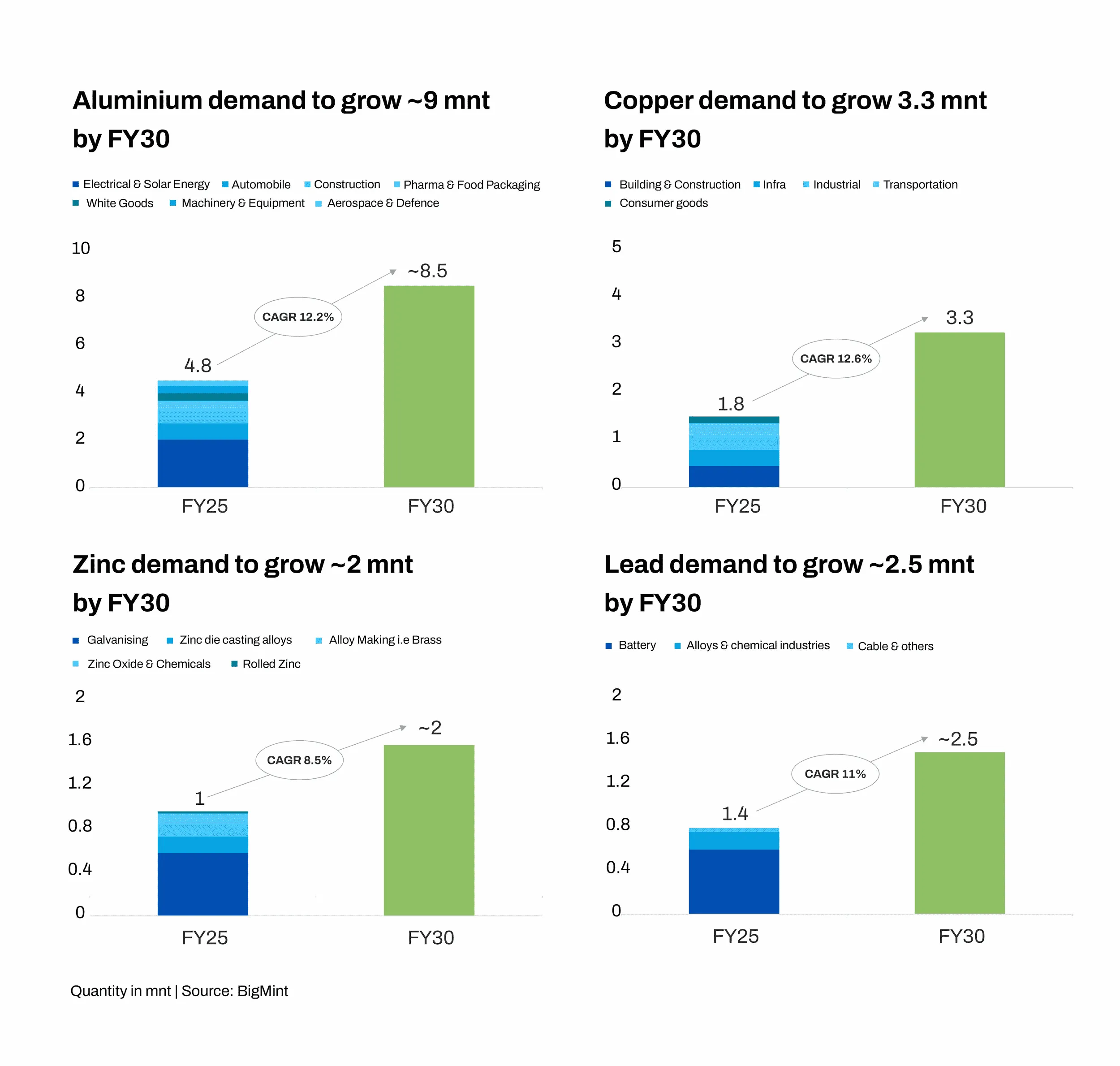

India continues to rank among the world’s fastest-growing major economies, supported by a projected GDP expansion of around 6.5% CAGR. This sustained economic momentum is creating a strong foundation for increased industrial activity, infrastructure development, and manufacturing growth.

As the economy expands, the demand for key non-ferrous metals—aluminum, copper, zinc, and lead—is set to rise substantially. These metals play a critical role across core sectors such as construction, power, transportation, and consumer goods, making them directly aligned with India’s growth trajectory.

Industry assessments indicate that consumption of these metals will grow at a healthy pace. Even on a conservative basis, demand is expected to increase by approximately 6% over the coming years. However, under more optimistic market conditions, projections suggest demand growth could climb closer to 9%.

Overall, India’s economic outlook positions the non-ferrous metals industry for a robust expansion cycle, driven by escalating domestic requirements and sustained momentum across end-use sectors.

India is entering a decisive capacity-led growth phase in the non-ferrous metals sector. Across aluminium, copper, zinc, and lead, primary output is projected to rise from around 5.8 MT in FY25 to nearly 9.5 MT by FY30. This marks one of the strongest supply-side expansions the industry has seen in the past decade.

Aluminium remains the anchor of this growth, with capacity expected to increase from 4.2 MT to 7.0 MT, driven by new smelting efficiencies and sustained investment by major producers. Copper, too, is set for a significant upswing, with capacity likely to double to 1.2 MT, restoring India’s position in the regional value chain.

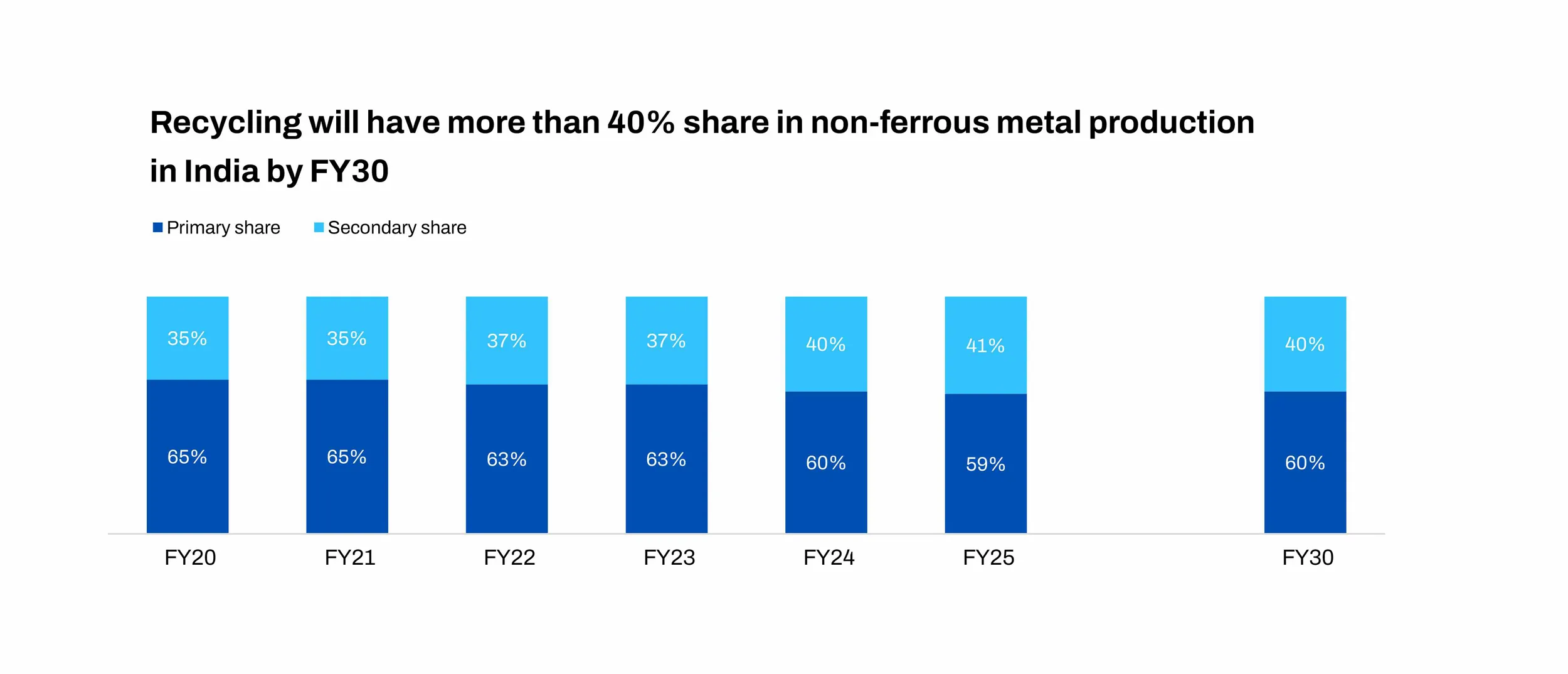

Parallel to primary expansion, the secondary non-ferrous ecosystem is strengthening. Production from recycling and scrap-based units is estimated to rise from 4.0 MT to nearly 6.2 MT by FY30, supported by improved scrap availability, formalisation of recycling networks, and a push toward circular manufacturing.

Recycled metals or metal scrap is gaining prominence as industries accelerate decarbonization efforts and align with government mandates to increase recycled content under EPR policies. The share of secondary metals in production is rising steadily, reflecting a shift toward circularity, reduced carbon footprint, and more efficient resource utilization across the aluminum, copper, zinc, and lead value chains.

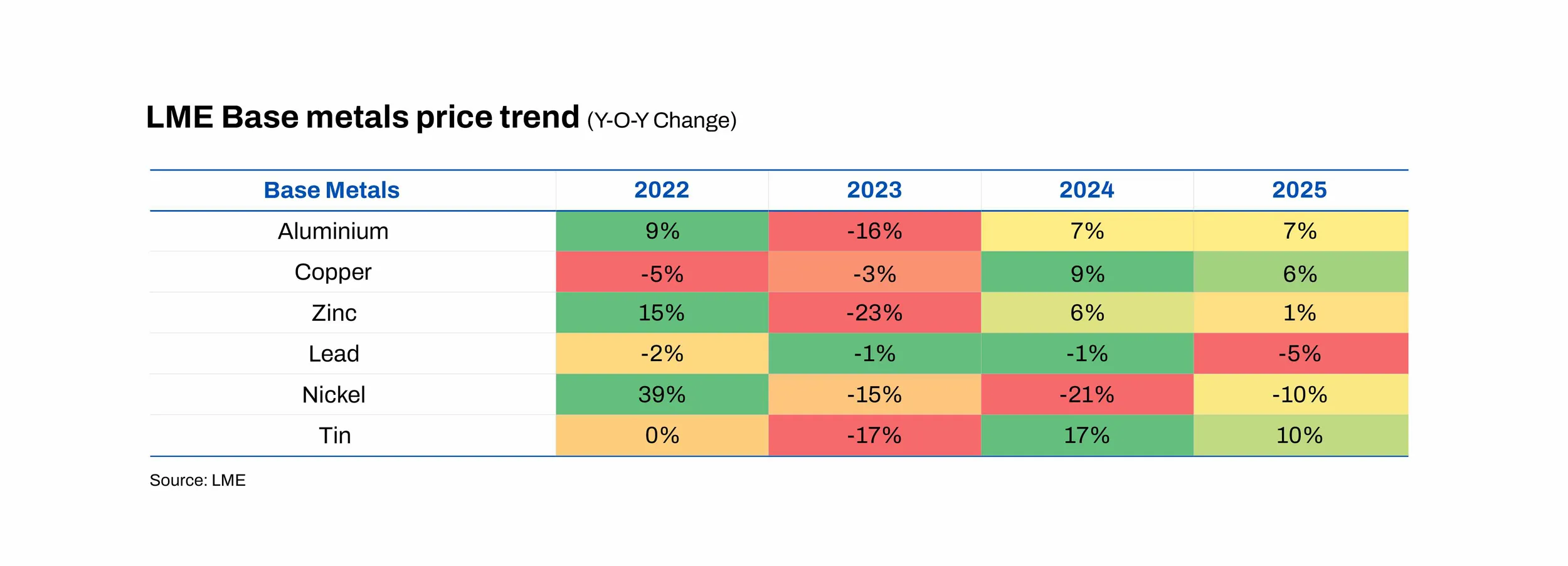

However, these metals are not immune to global uncertainties, wars, and geopolitical crises, as well as trade frictions, protectionism, tariffs, and diplomatic standoffs. Aluminum, copper, zinc, and lead have witnessed significant volatility in recent years due to shifting supply-demand dynamics, trade wars and tariffs, and the accelerating green transition. These forces continue to shape pricing trends and market stability across the non-ferrous ecosystem.

Connect with top industry leaders!

Grab the participant list now!

If you want to attend this conference and participate in the programme, then please hurry and register now!

Register Now

03-June-2026

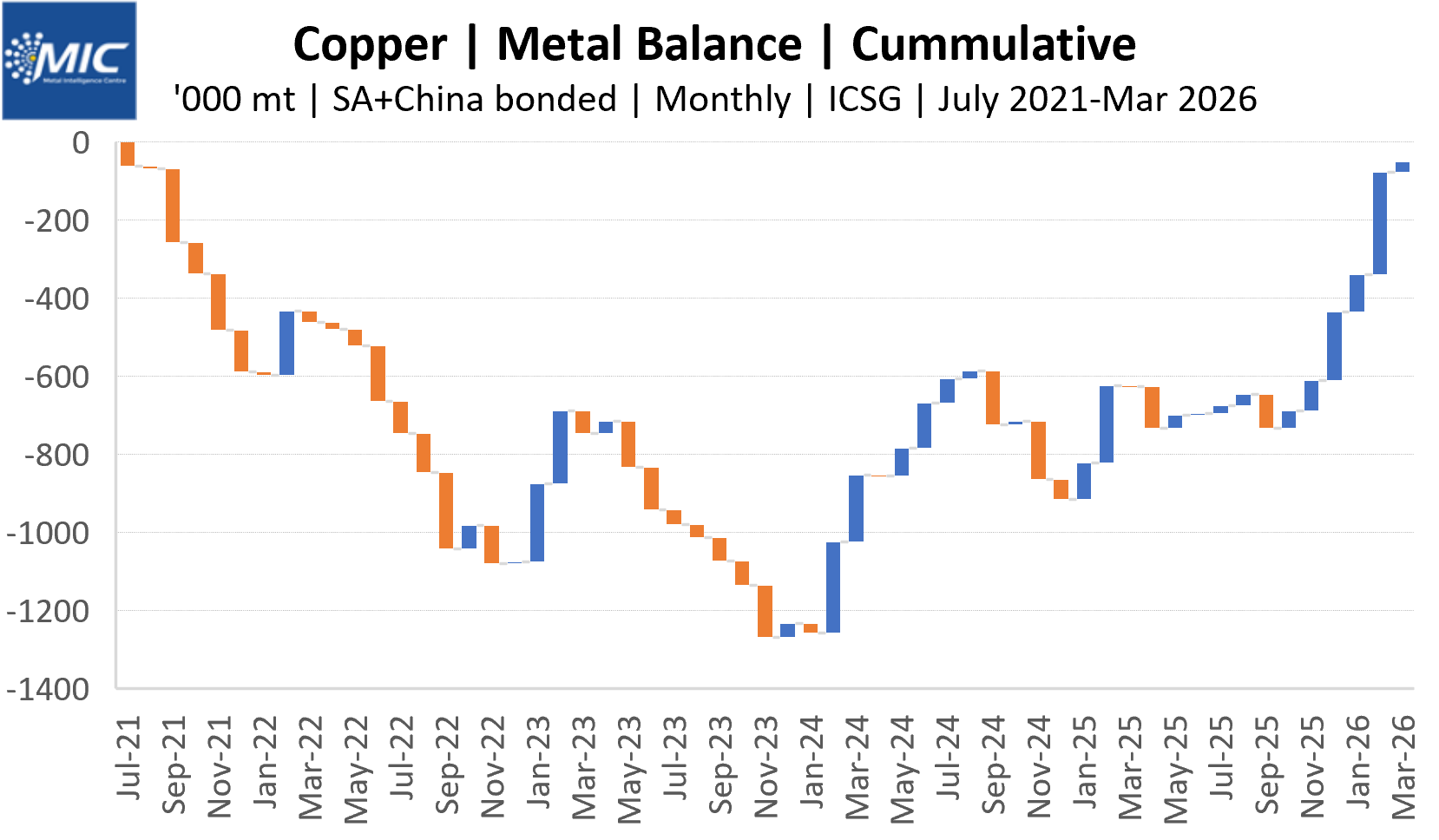

Q1 copper surplus jumps to 0.39 mnt Weak demand outweighs global supply risksMetal Intelligence Centre: The global copper market continued to register a surplus in recent years, challenging widespread expectations of a prolonged supply deficit drive...

12-May-2026

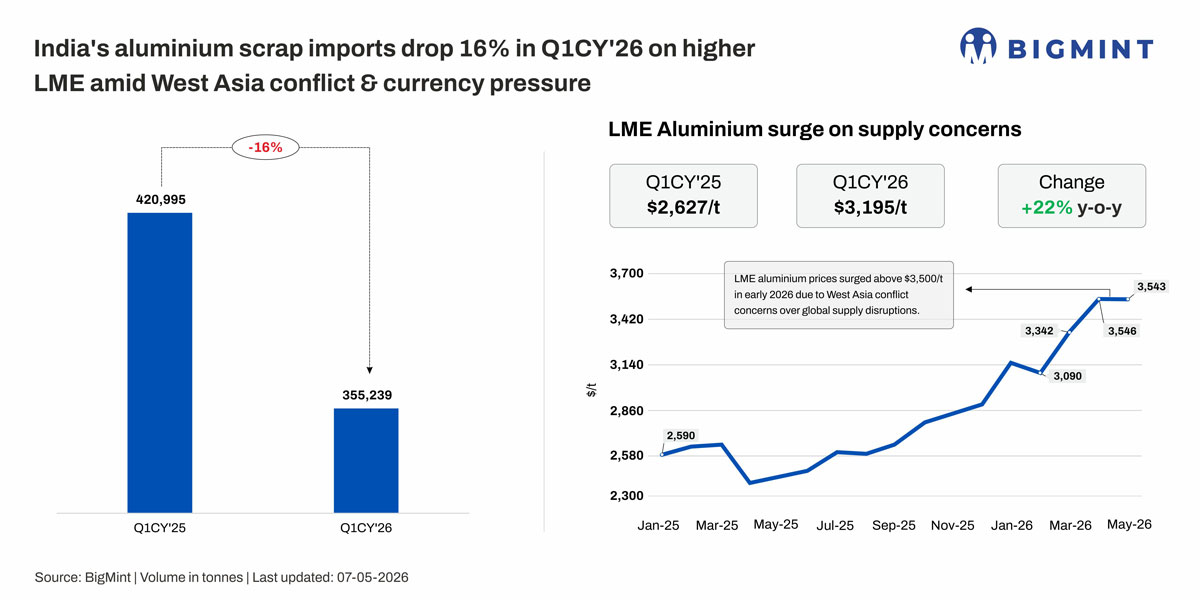

Weak rupee and LME prices raise costs Supply constraints expected to persist into Q2 Domestic recyclers face rising raw material pressuresMorning Brief: India's aluminium scrap imports declined by 16% y-o-y to 0.35 mnt in Q1CY'26, down from 0.42 mnt...

11-May-2026

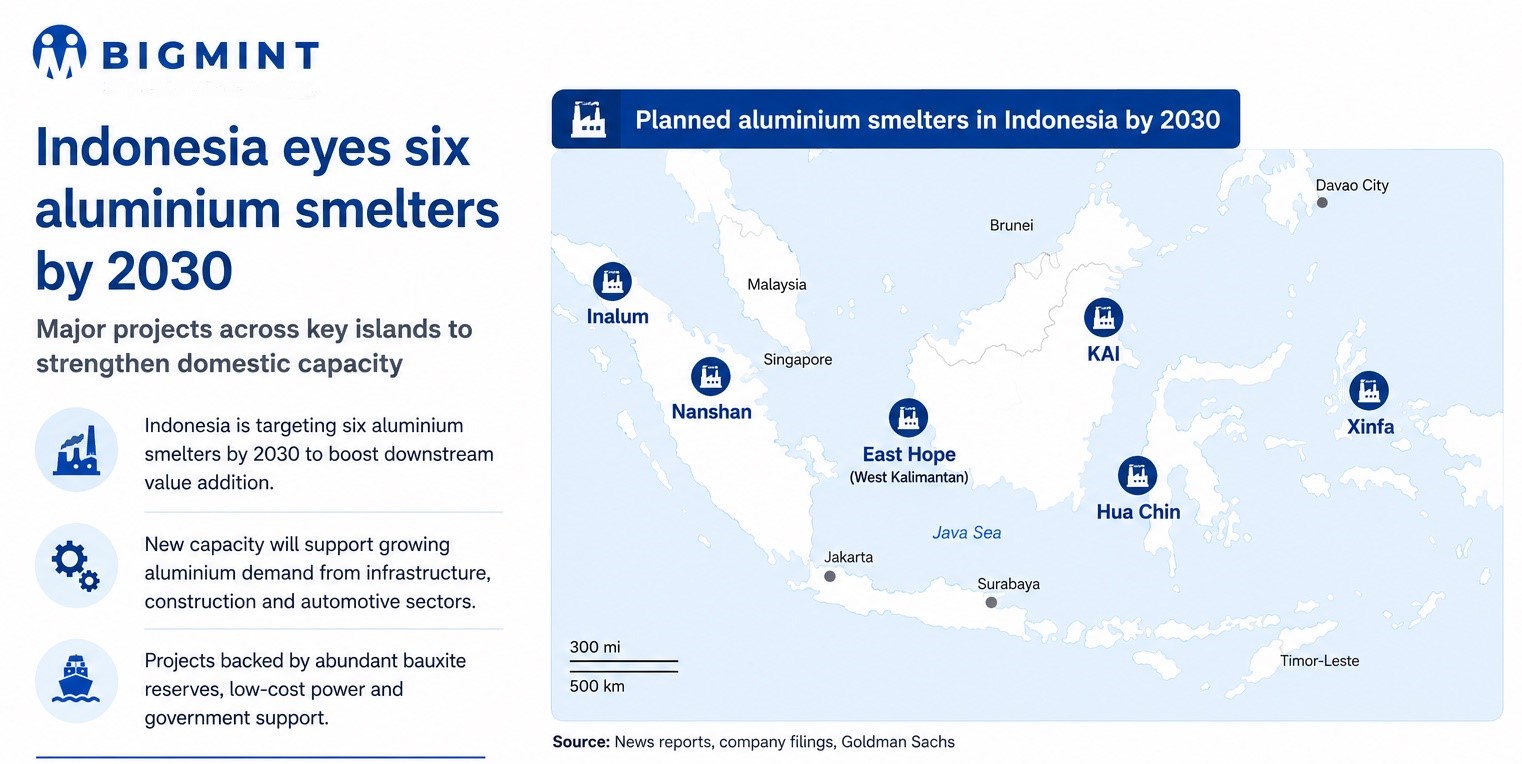

Indonesia Sulawesi smelter expands 480,000 t capacity 2 mtpa alumina refinery planned in Riau IslandsChina's Tsingshan Holding Group, also known in recent reports as "Tianshan," has applied to register its Indonesian aluminium brand HuaChin for deli...

07-May-2026

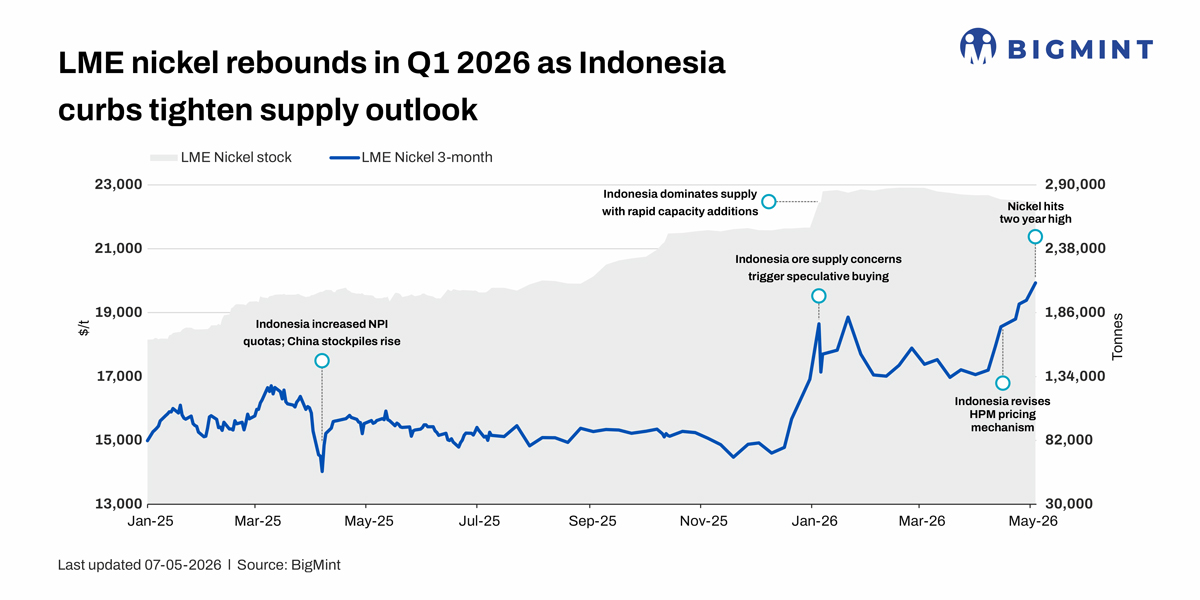

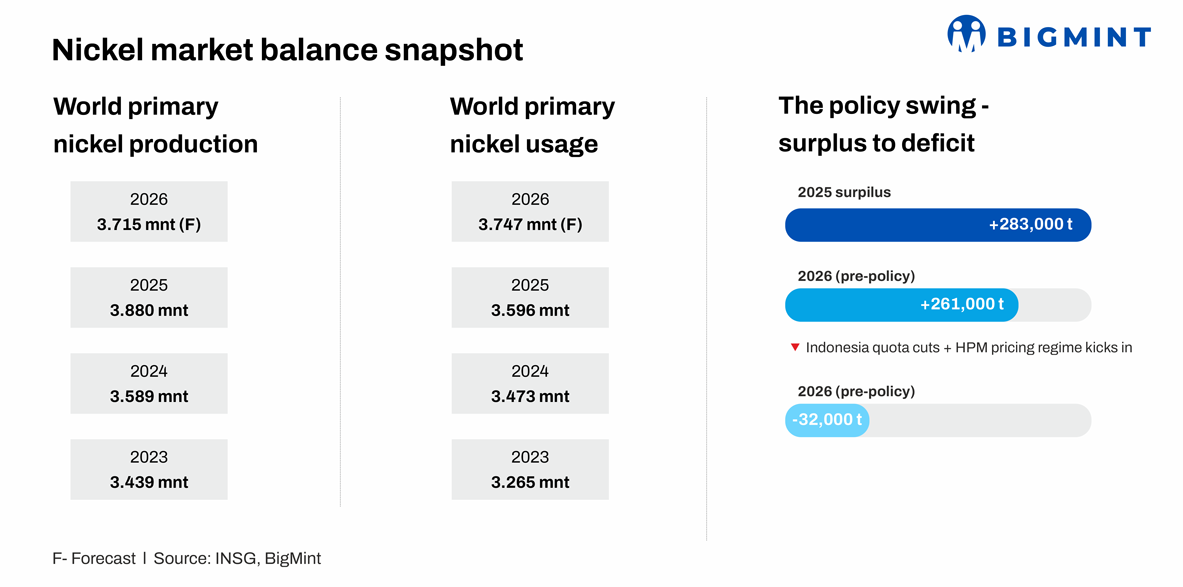

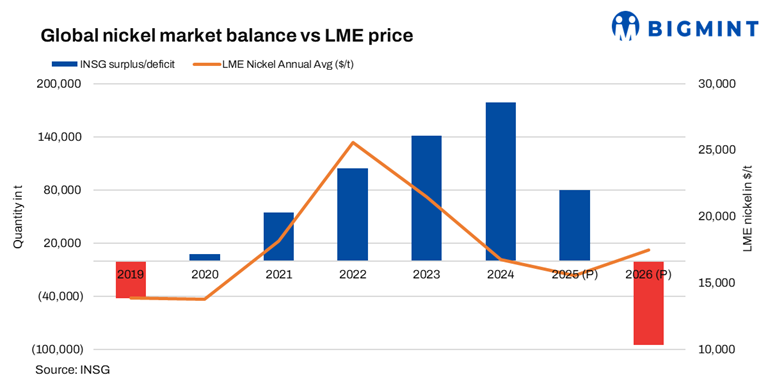

Indonesian production quota cuts, revised ore pricing mechanisms lift prices 32,000-t deficit expected in 2026 against earlier forecast surplus of 261,000 tLondon Metal Exchange (LME) nickel staged a strong recovery in Q1CY'26 after opening the year...

25-April-2026

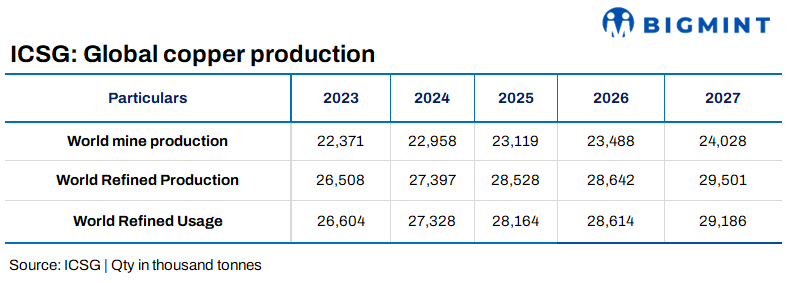

Copper production to grow 2.3% globally by 2027 outlook Global expansions and projects to strengthen copper supply growthGlobal copper mine production is projected to reach 24 mnt in 2026, reflecting 1.6% growth, and is expected to rise further to a...

25-April-2026

Market shifts from surplus to deficit year-on-year Indonesia policy reset reshapes global cost curveA market that entered 2026 burdened by a 283,000-tonne surplus is being reshaped-quarter by quarter - by Indonesian quota cuts, a revised ore-pricing...

24-April-2026

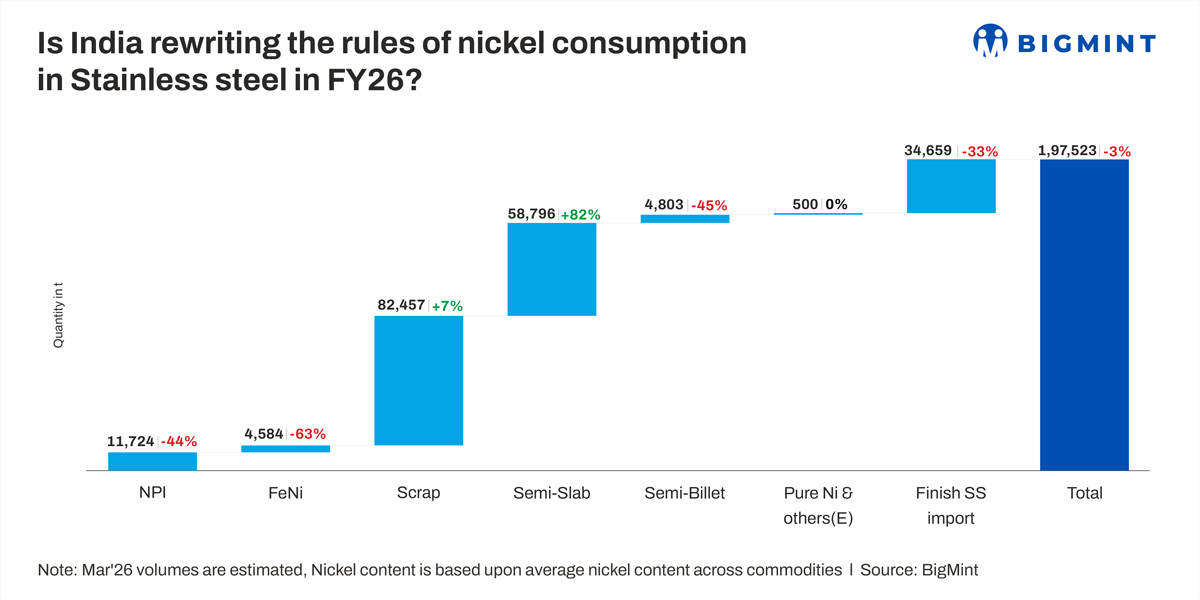

NPI, FeNi imports plunge y-o-y amid nickel price volatility Slab imports surge 82% as mills focus on cost optimisationIndia's nickel consumption in FY'26 reflects a strategic realignment rather than a demand slowdown. Total nickel content consumptio...

21-April-2026

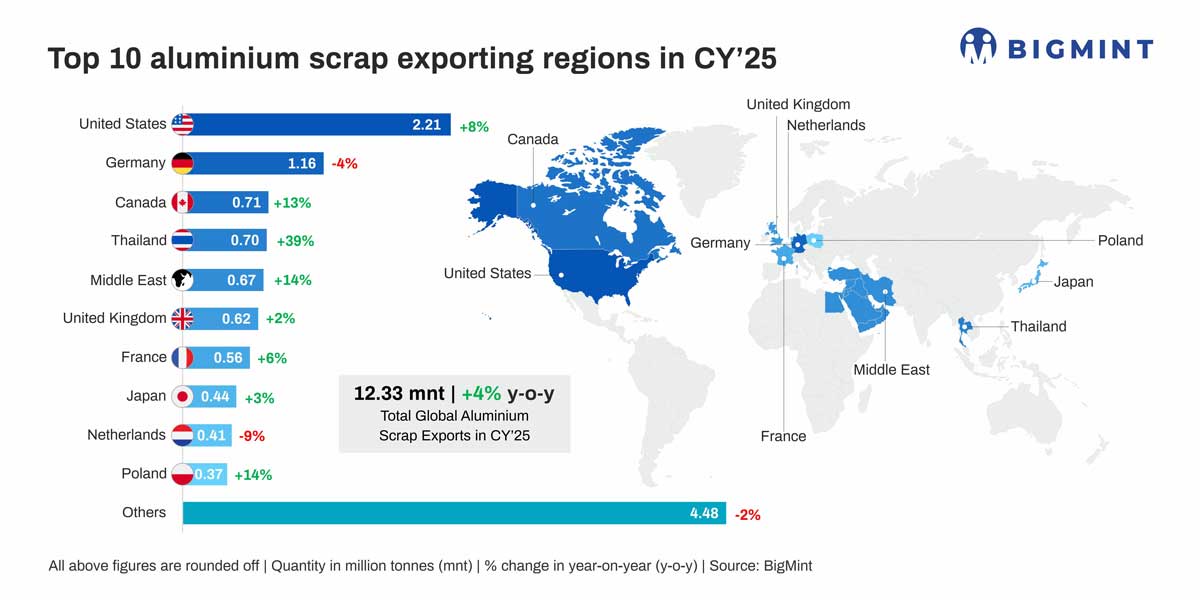

India remains key driver of aluminium scrap demand China's scrap imports reach 5-year high in CY'25Global aluminium scrap trade volumes, including intra-European trade, increased to 12.33 mnt in CY'25 from 11.90 mnt in CY'24, reflecting a 4% y-o-y r...

16-April-2026

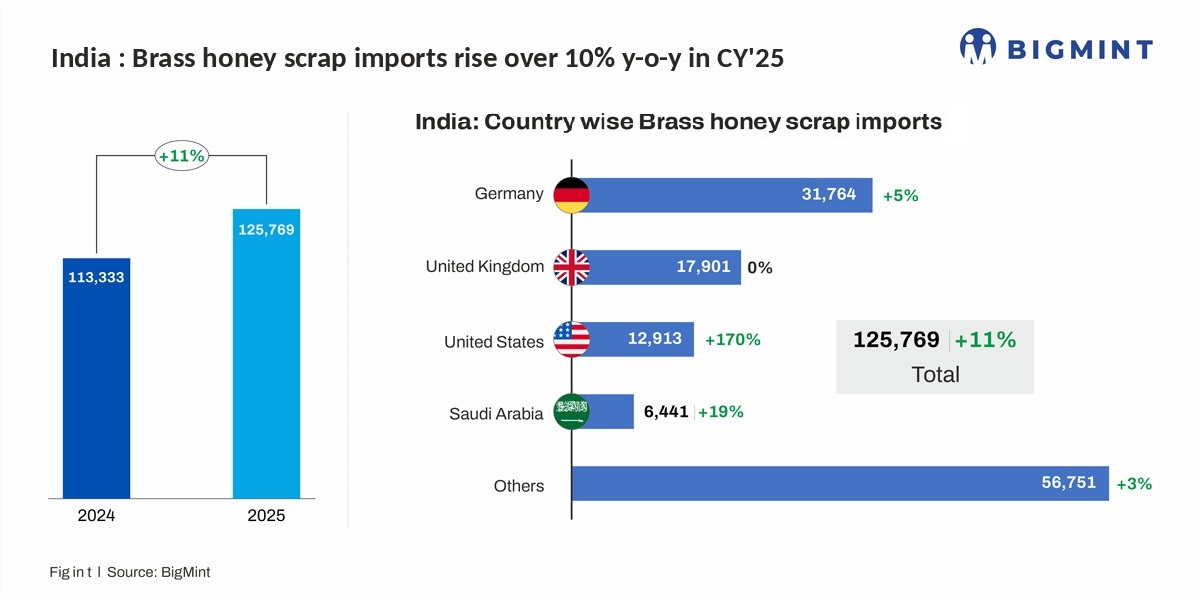

India's fragmented, informal recycling ecosystem limits domestic generation Germany remains leading supplier, supported by its strong industrial baseIndia's imports of brass honey scrap rose 11% y-o-y to 0.13 million tonnes (mnt) in CY'25, reinforci...

16-April-2026

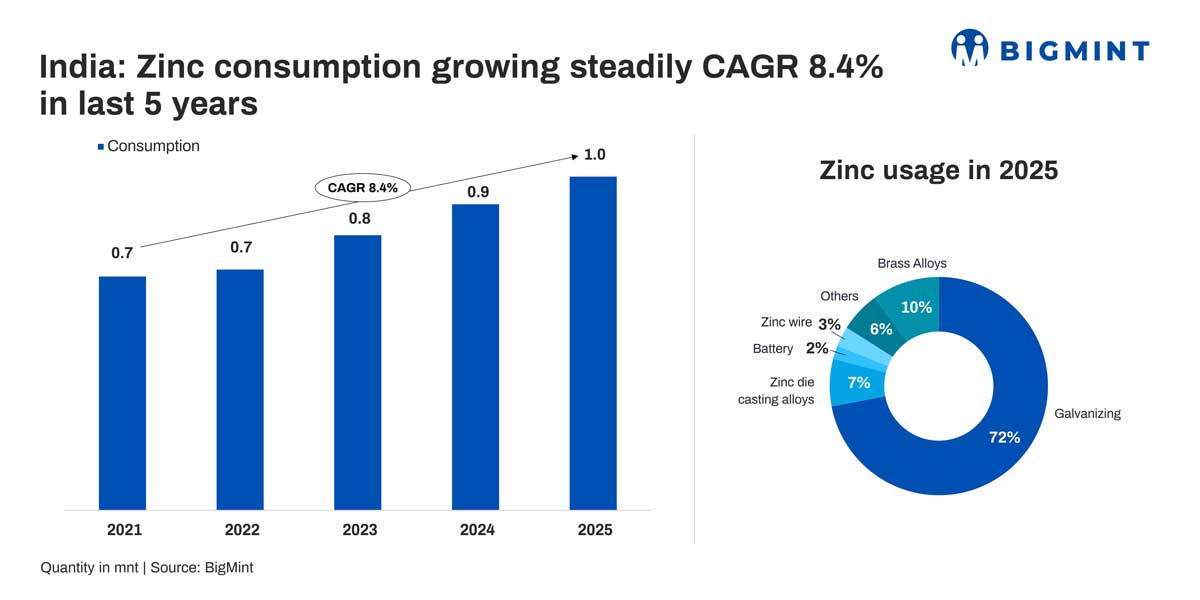

Zinc consumption outpaces production growth, imports jump Battery, die-casting segments post fastest growth amid low base India's per capita consumption remains far below global averagesMorning Brief: India's zinc consumption grew at a compound annu...

14-April-2026

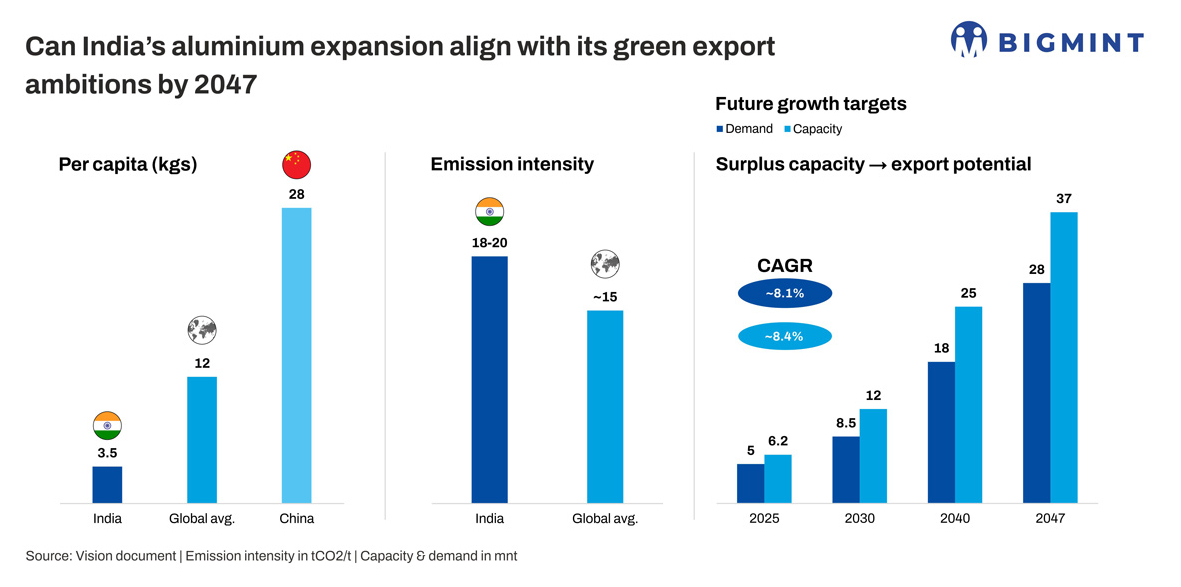

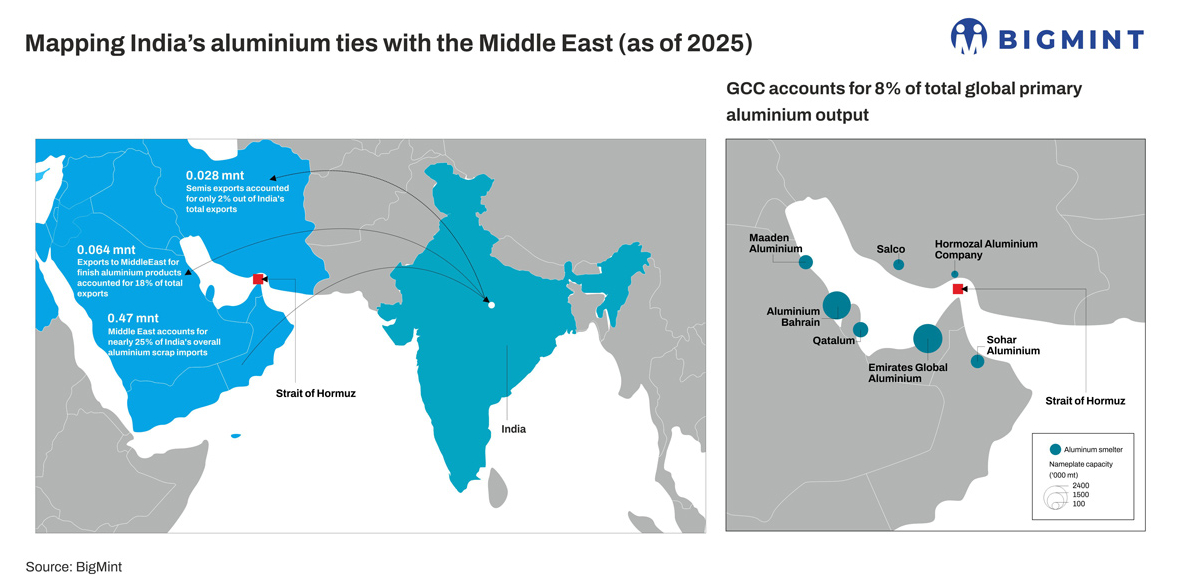

Green aluminium transition still at early stage Power shift critical for global competitivenessIndia's aluminium industry is entering a defining phase where its ambitions extend beyond domestic growth. The real opportunity lies in whether India can ...

14-April-2026

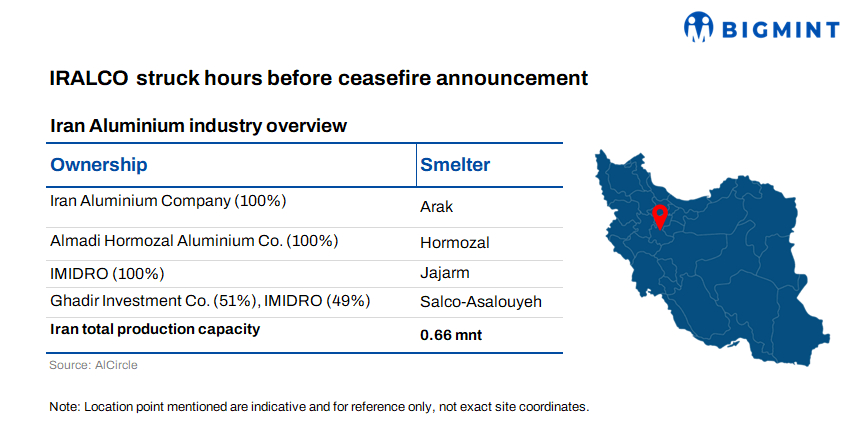

Escalation follows earlier strikes on Gulf smelters Petrochemical complex also hit in aerial strikeJust hours before the official announcement of a two-week ceasefire in the ongoing US-Israel and Iran conflict, Iranian media reported targeted strike...

14-April-2026

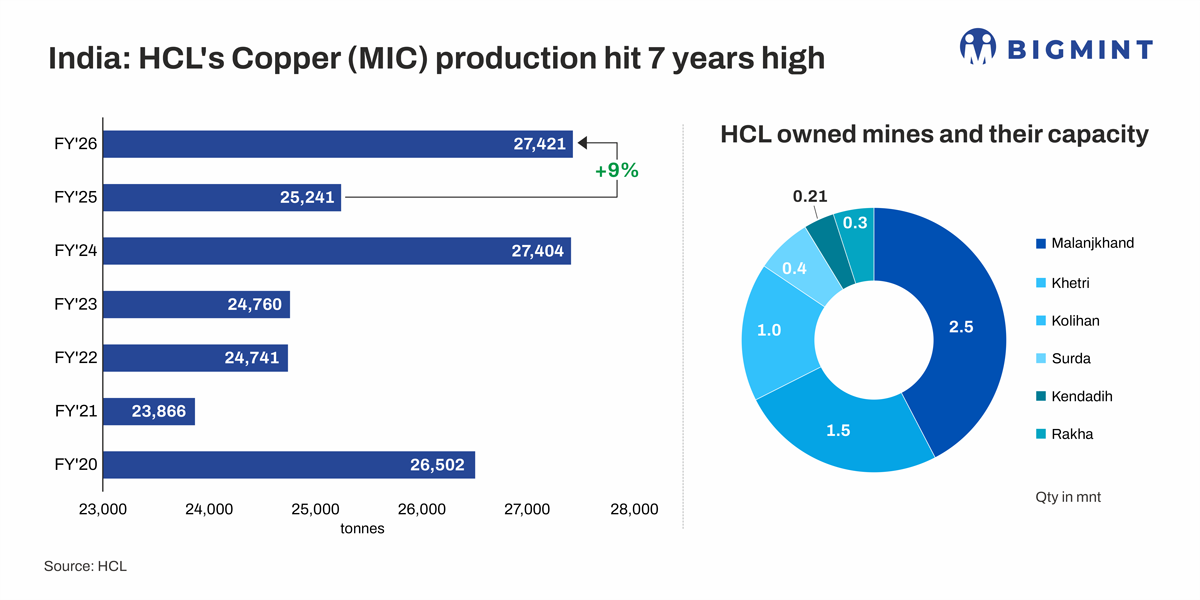

HCL achieves record production and operational growth in FY'26 Expansion plans accelerate amid rising copper import dependenceHindustan Copper Limited (HCL), Indias only integrated copper mining company, reported a strong operational performance in ...

14-April-2026

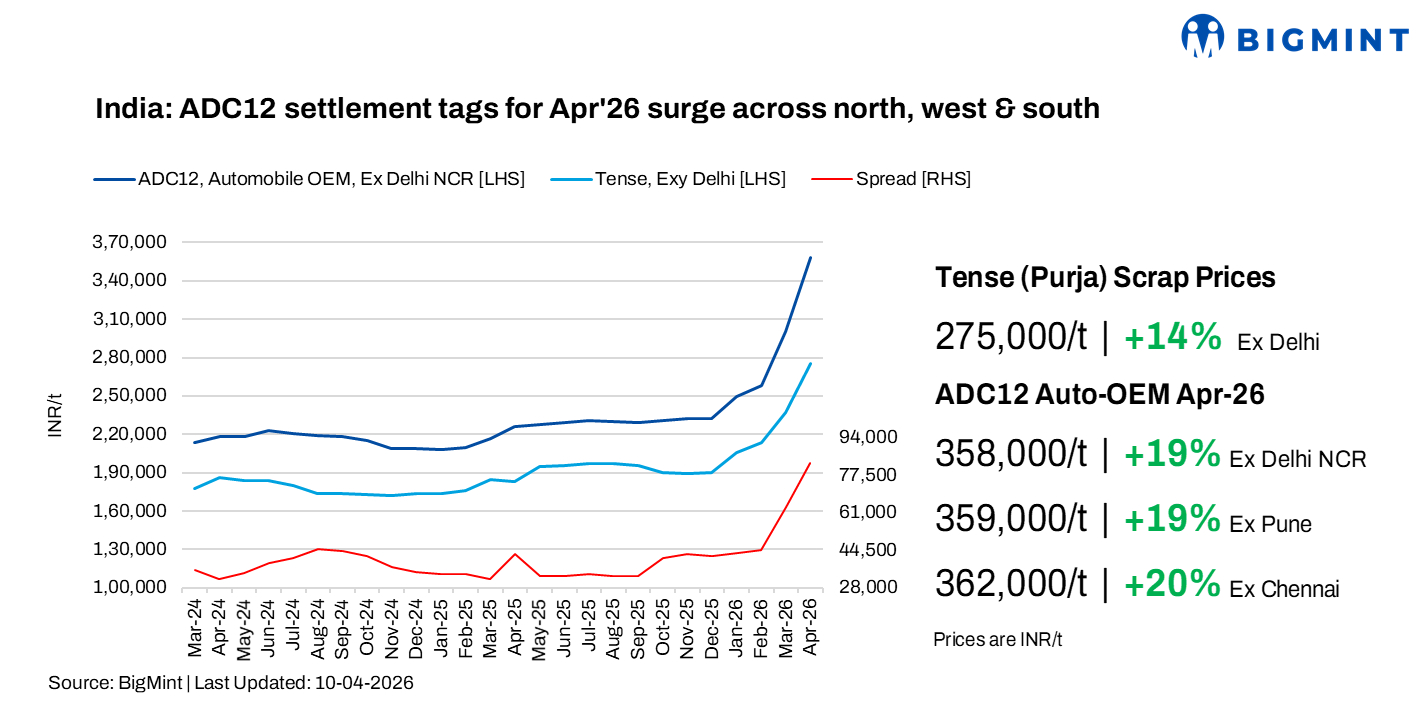

India ADC12 prices surge up to 20% m-o-m in Apr'26 Wide bid-offer gaps emerge as buyers aggressively resist high offersIndia's aluminium ADC12 alloy ingot prices rose sharply m-o-m in April 2026, driven by higher raw material costs and continued str...

14-April-2026

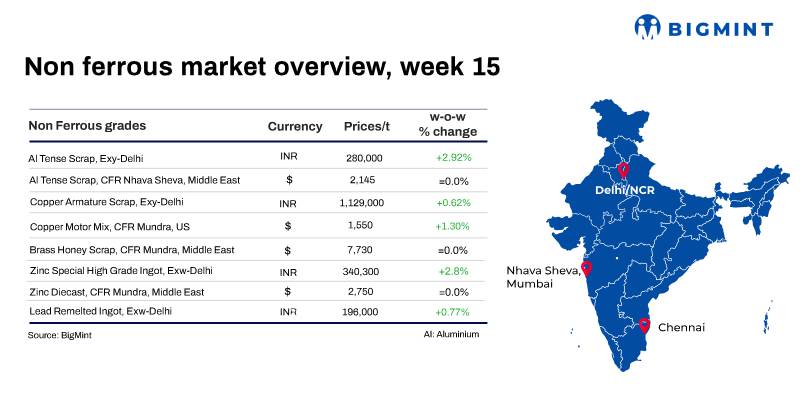

Inventory drawdowns tighten global base metals supply Domestic scrap markets firm amid supply constraintsLME base metals trended higher w-o-w as of 10 April, supported by improved sentiment across the complex. Copper led gains, rising 2.59% to $12,5...

07-April-2026

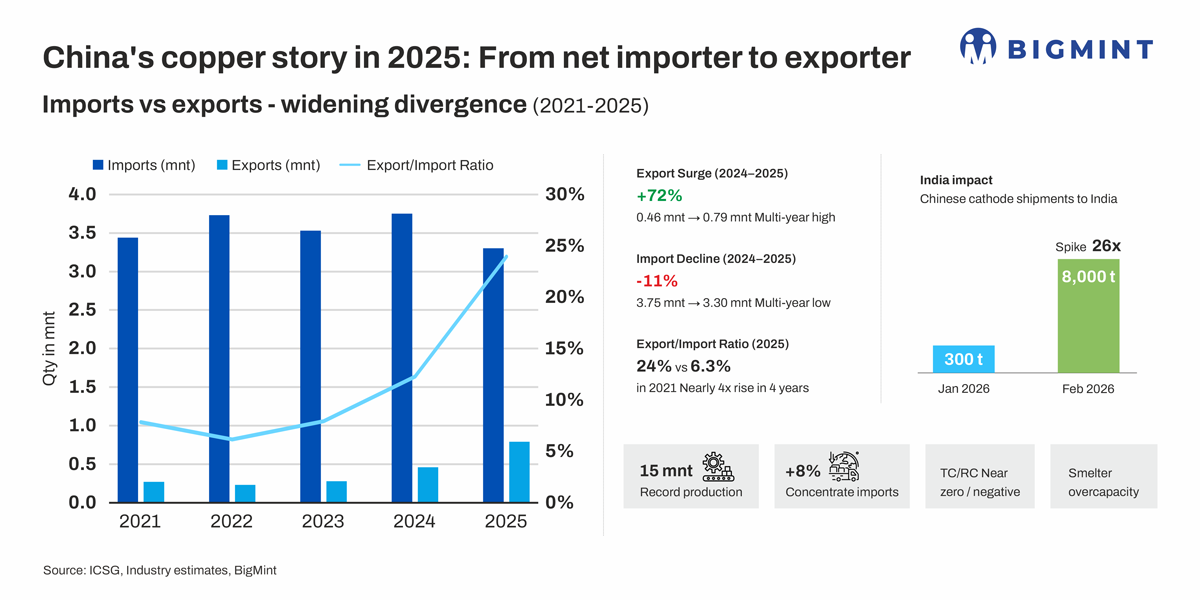

Concentrate imports rising to feed expanding smelting capacity TC/RCs are collapsing due to intense competition for raw materialsChina's refined copper production hits record high despite tight concentrate supplyChina's refined copper production sur...

07-April-2026

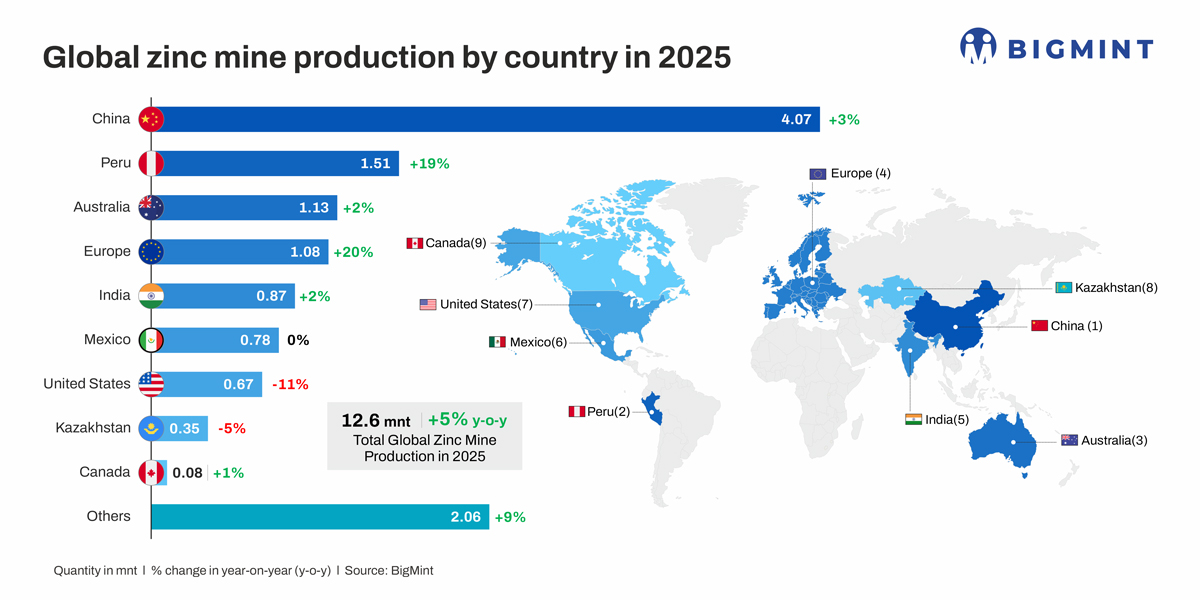

Mine output rises, led by Peru, steady gains in Australia and India China produces 4.07 mnt but imports surge 30% to 2.57 mnt Smelter tie-ups, trade disruptions, refined deficit highlight concentrate tightnessMorning Brief: Global zinc mine producti...

07-April-2026

Smelting overcapacity in China intensifies global concentrate imbalance. Global concentrate deficit expected in 2026 despite refined surplus. The global copper market is witnessing a imbalance, as tightening concentrate supply struggles to keep pace...

25-March-2026

For 2026, proposed allocations represent a reduction of 110 mnt from 2025 levels Data shows RKAB quotas have often been exceeded, raising doubts about enforecementIndonesia, the world's largest nickel producer, is engineering a sharp contraction in ...

20-March-2026

Domestic prices rise sharply along with global benchmarks Scrap supply tightens across Gulf dependent routesThe initial impact of the West Asia conflict has already been visible in global aluminium prices and supply risks. What is now unfolding is t...

17-March-2026

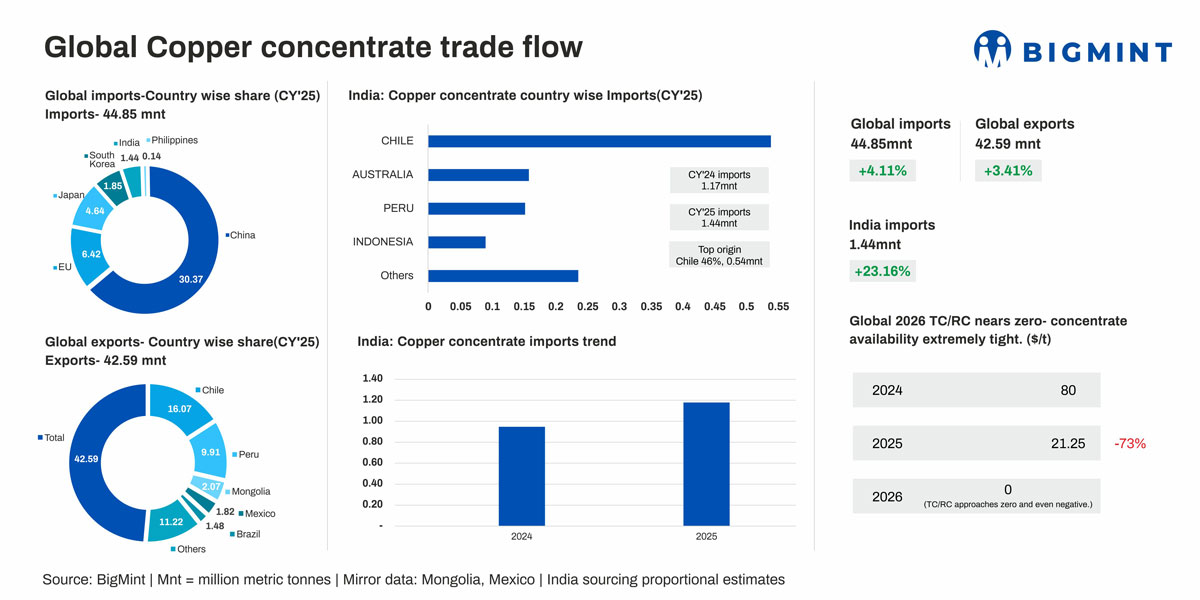

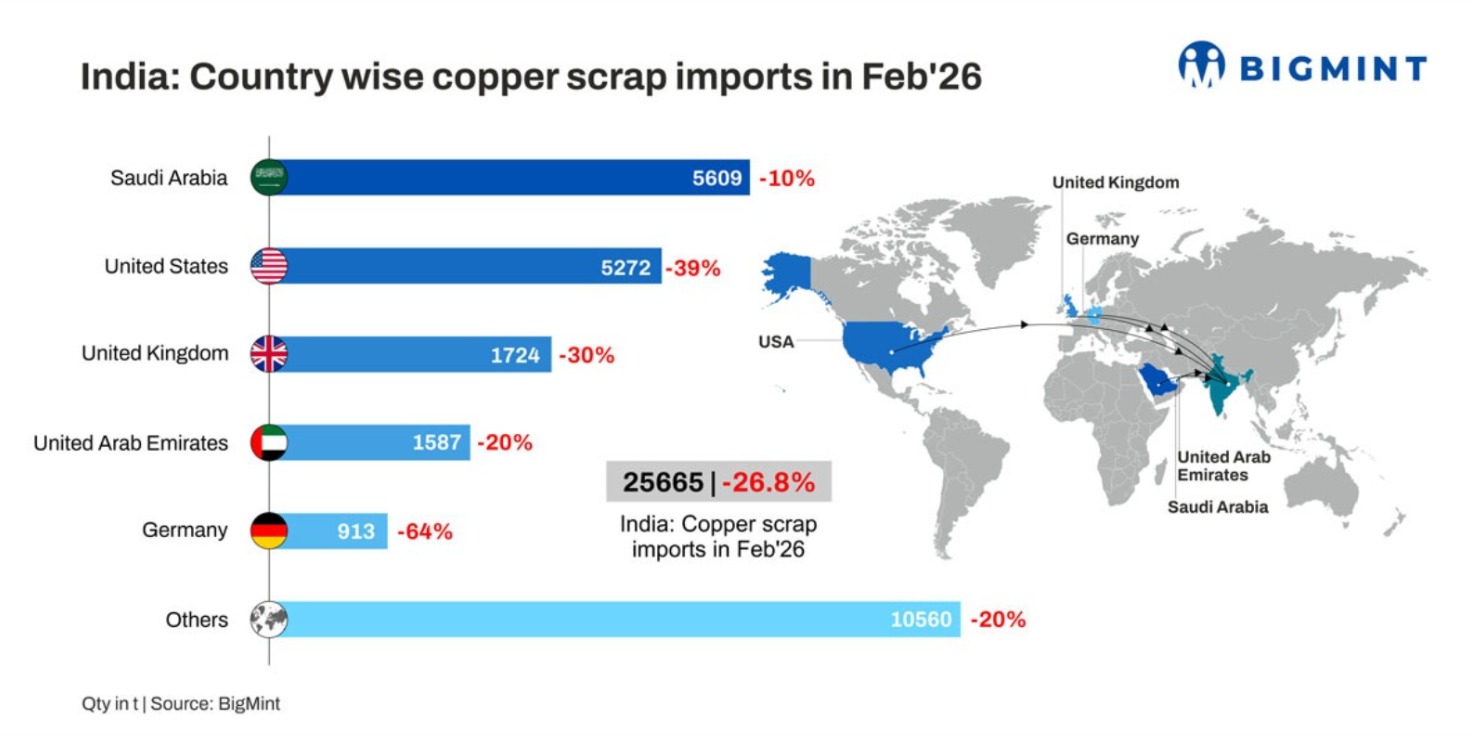

Holiday closures in Jan slow scrap collection in major exporting regions Buyers delay bookings ahead of Budget amid tariff change expectations.India's copper scrap imports fell 27% m-o-m to 25,700 tonnes (t) in February 2026 from 35,000 t in January...

14-March-2026

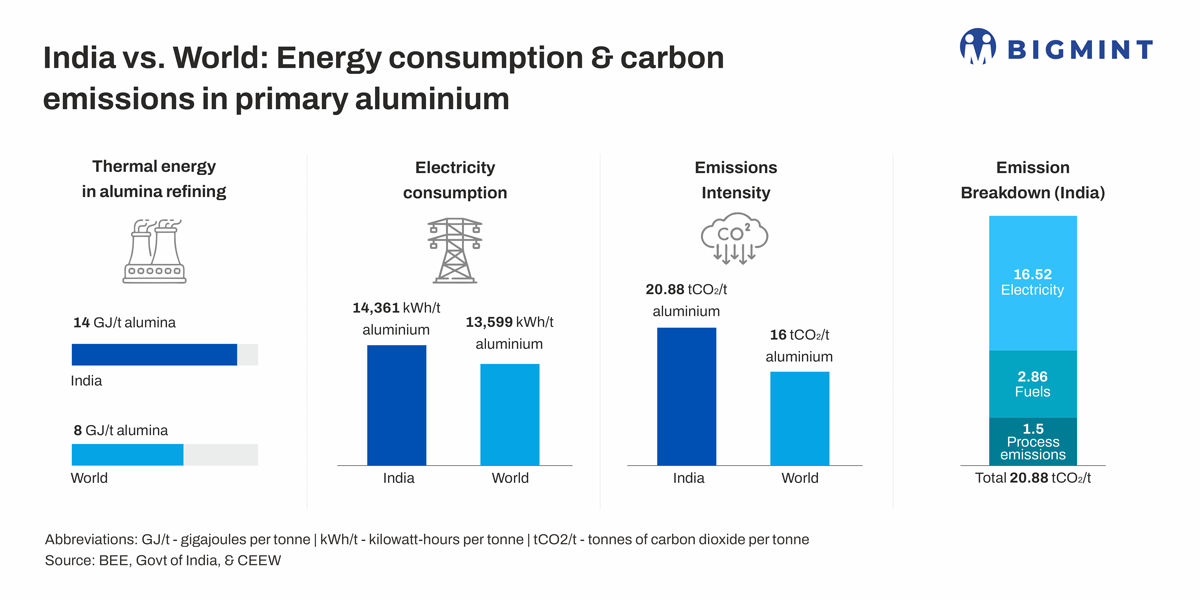

Around 80% of emissions are from captive thermal power India much lower than global average energy and CO2 intensity CCTS targeting incremental emissions reduction from primary productionMorning Brief: India is the second largest aluminium producer ...

Anamika Jain

+91-9039722000

anamika.j@bigmint.co

Pankaj Thakur

+91-9039322000

pankaj@bigmint.co

Kabir Raj Dubey

+91-9993931361

kabir@bigmint.co

Ruchi Khanna

+91-9654338732

ruchi@bigmint.co