16-April-2026

- Zinc consumption outpaces production growth, imports jump

- Battery, die-casting segments post fastest growth amid low base

- India's per capita consumption remains far below global averages

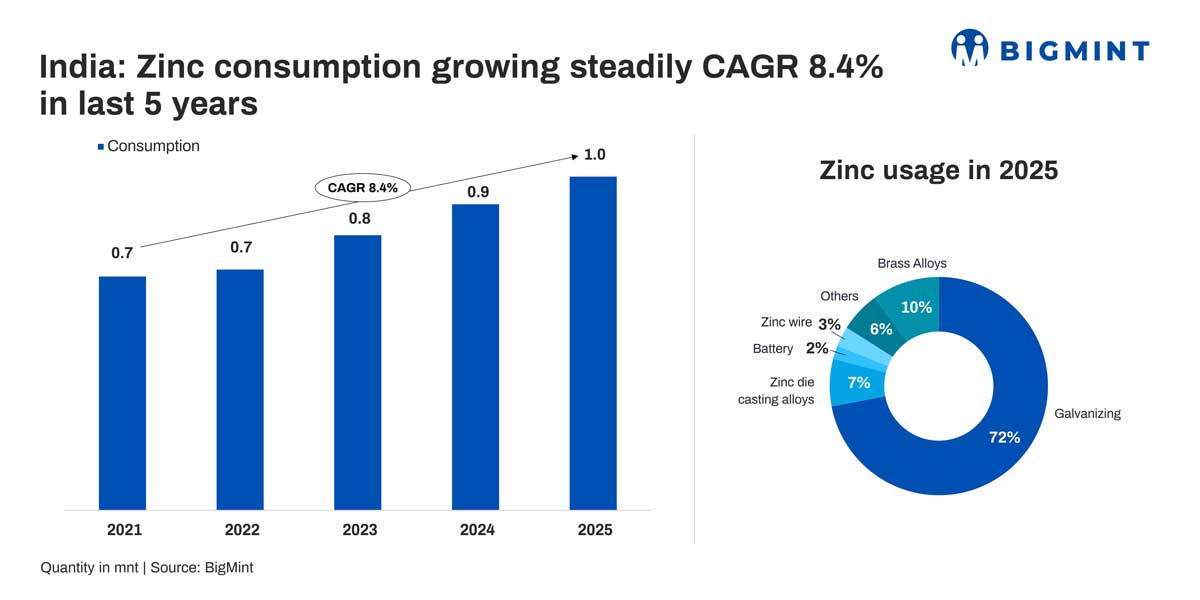

Morning Brief: India's zinc consumption grew at a compound annual growth rate (CAGR) of 8.4% between calendar years 2021 and 2025, supported by rising galvanising demand tied to infrastructure expansion and steel capacity additions.

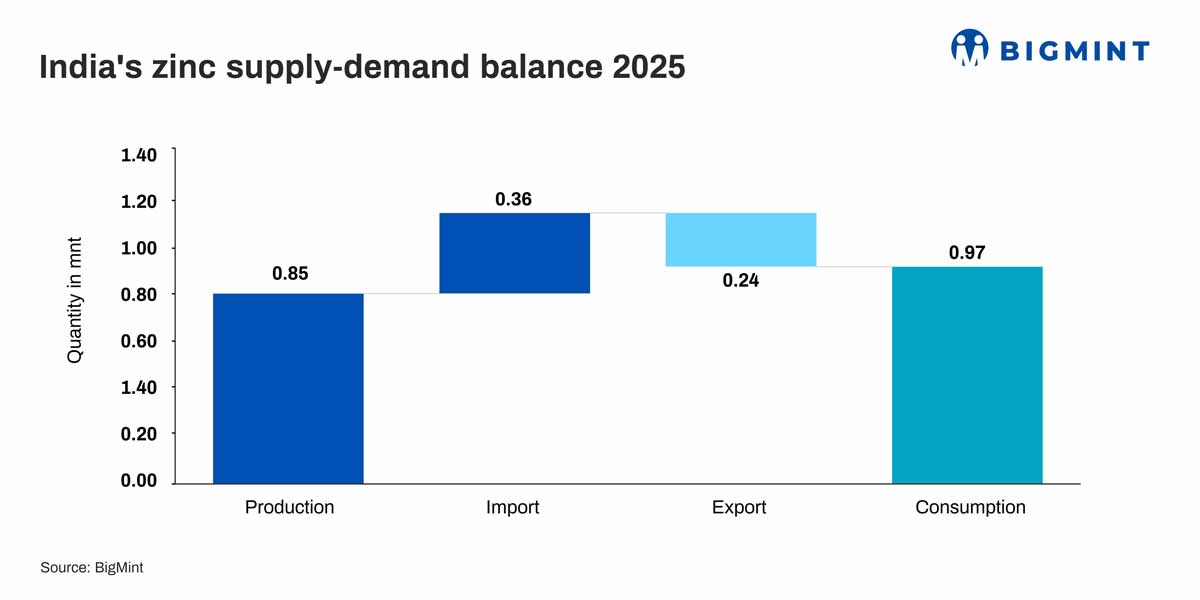

BigMint data shows that total consumption stood at nearly 1 million tonnes (mnt) in 2025, rising by 9% y-o-y. Production growth was much slower, at 2.4% y-o-y to 0.85 mnt.

In fact, over 2022-25, production has remained range-bound within 0.81-0.85 mnt, while consumption has increased from 0.7 mnt in 2022 to 1 mnt in 2025. This has widened the domestic demand-supply gap, leading to increased reliance on imports (0.26 mnt in 2022 to 0.36 mnt in 2025) and shrinking export surplus (0.38 mnt in 2022 to 0.24 mnt in 2025).

Galvanising anchors demand

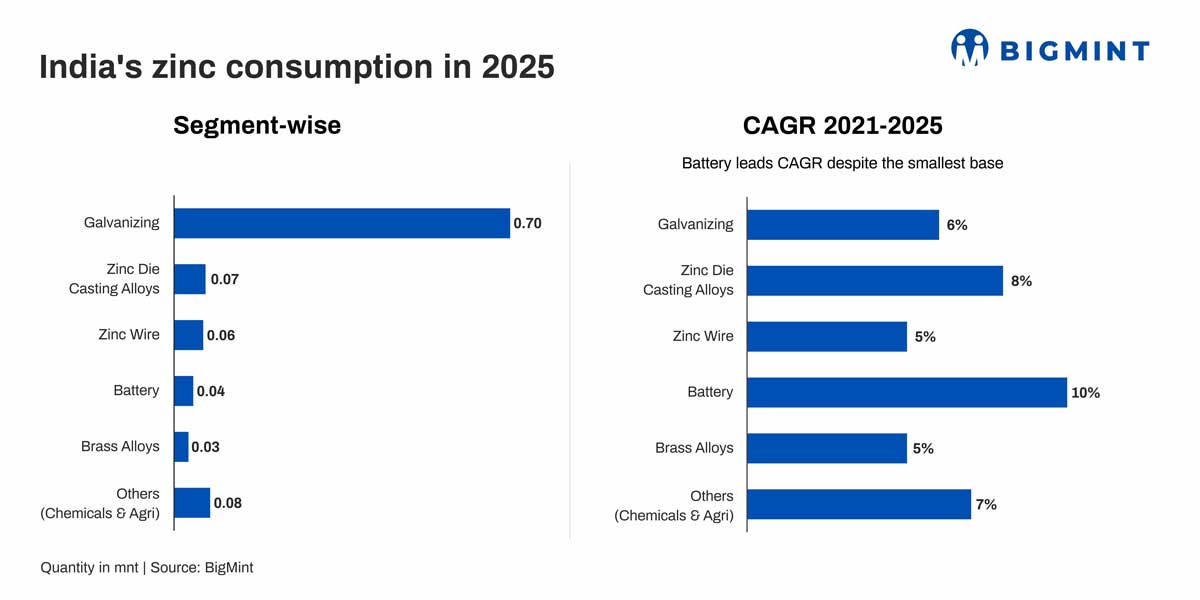

Galvanising accounted for nearly 72% of India's zinc demand in 2025, with consumption expanding at about 6% CAGR during 2021-25. The increase reflects stronger output from continuous galvanising lines and hot-dip galvanising (HDG) units supplying sheets, pipes and infrastructure fabrication.

Infrastructure-grade steel consumes 100-120 kilogram (kg) of zinc per tonne, while automotive galvanising requires 60-90 kg/t. Expansion in renewable energy, transmission, metro rail, and construction has increased galvanising utilisation. Solar mounting structures, pipes and transmission towers have also emerged as key demand drivers.

Meanwhile, consumption in zinc die-casting alloys increased by a CAGR of over 8%, while zinc wire demand doubled over the period. Battery applications recorded the fastest expansion at around 10% CAGR, supported by emerging energy storage demand. Brass and chemical segments also grew moderately, highlighting stable industrial consumption.

Per capita consumption highlights long-term upside

India's per capita zinc consumption remains significantly below global benchmarks at around 0.5 kg, compared with a global average of 3-4 kg and up to 6-7 kg in developed economies (South Korea, and US). Even a modest increase to 1 kg per capita would imply incremental demand of over 1 mnt.

This gap reflects underpenetration in key segments such as automotive galvanisation, infrastructure coatings, and corrosion protection standards. To illustrate, in India, about 20-25% of automotive production units using galvanised steel versus 90-95% globally, according to the International Zinc Association (IZA). This indicates significant headroom for zinc consumption growth.

Policy initiatives, including increased infrastructure spending, are expected to support gradual convergence towards global averages.

Domestic demand remains strong despite LME price volatility

The consumption growth cycle coincided with volatile but elevated London Metal Exchange (LME) zinc prices, which remained largely above $2,700/t during 2024-2026 after peaking above $4,100/t in 2022. Despite price fluctuations, galvanisers continued procurement, indicating structurally strong consumption driven by steel-intensive sectors.

LME zinc prices surged from around $2,800/t in early 2021 to a peak of nearly $4,500/t in 2022 amid energy-driven smelter cuts, before correcting to the $2,400-3,100/t range during 2023-2024. Prices recovered again through 2025, averaging around $2,600-3,100/t and briefly touching about $3,400/t in early 2026 before easing towards $3,050/t.

The elevated price band supported domestic realisations while not significantly impacting galvanising demand, which remained volume-driven. The steady increase in imports despite price volatility also points to robust consumption dynamics and highlights limited price sensitivity and a structurally tightening domestic supply balance.

Outlook

India's zinc demand is set for sustained growth amid the government's infrastructure push and rising steel production. Demand is expected to reach around 2 mnt by FY'30, implying a CAGR of approximately 8.5%, according to BigMint's projections.

Infrastructure segments such as highways, rail electrification, renewable energy installations and transmission networks, are expected to drive consumption growth, given that all of them require corrosion-resistant steel.

Increased adoption of galvanised steel in automotive and construction, alongside policy efforts to improve corrosion standards, is also expected to gradually lift usage intensity

On the supply side, domestic output is projected to grow at a slower pace of about 5.9% CAGR to reach approximately 1.2 mnt by FY'30. Production is largely dominated by Hindustan Zinc Limited, which has announced capacity expansion plans, but overall growth is expected to significantly lag behind demand. This imbalance suggests a widening structural deficit, likely resulting in increased import dependence and tighter domestic availability over time.

Key questions for the industry

Will galvanising continue to account for over 70% of India's zinc demand? Can battery-linked zinc demand scale meaningfully with EV adoption? Will die-casting growth accelerate with automotive expansion? How will LME price volatility influence galvanisers' procurement strategy? Will domestic zinc supply keep pace with double-digit demand growth?

These questions will be discussed at BigMint India Non-Ferrous Week 2026, a two-day industry forum bringing together producers, recyclers, traders, policymakers, technology providers and end-use manufacturers across aluminium, copper, zinc, lead, nickel and tin. The event will be held on 9-10 June 2026 at The Lalit, Mumbai, focusing on demand outlook, pricing trends, trade flows and investment decisions shaping India's non-ferrous markets.