24-April-2026

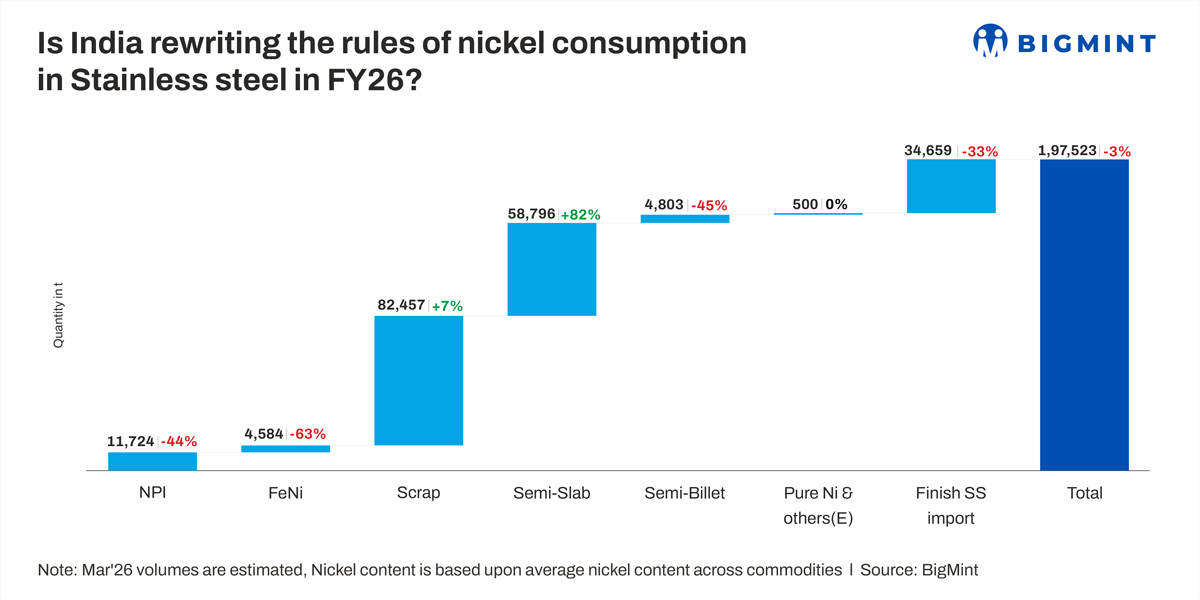

- NPI, FeNi imports plunge y-o-y amid nickel price volatility

- Slab imports surge 82% as mills focus on cost optimisation

India's nickel consumption in FY'26 reflects a strategic realignment rather than a demand slowdown. Total nickel content consumption edged down by 3% y-o-y to 197,523 tonnes (t), compared to 203,344t in FY'25. However, beneath this stable headline lies a sharp shift in sourcing dynamics, with stainless steel producers actively reconfiguring their raw material mix to optimise costs and improve flexibility.

The most notable trend was the steep decline in primary nickel inputs. Nickel pig iron (NPI) consumption dropped 44% y-o-y to 11,724 t, while ferro nickel (FeNi) saw an even sharper fall of 63% to 4,584 t. This marks a significant pullback from traditional imported nickel-bearing intermediates, largely due to their elevated and volatile cost structures.

In contrast, scrap strengthened its position as the backbone of Indias nickel consumption. Nickel content through scrap rose 7% y-o-y to 82,457 t, making it the single largest contributor to the overall basket. The shift was primarily driven by favourable economics -- imported stainless steel scrap prices declined more sharply than primary nickel, enhancing its cost competitiveness. Mills, especially those operating electric arc furnaces (EAF) and induction furnaces (IF), increasingly preferred scrap due to its lower effective nickel unit cost, shorter processing cycles, and reduced working capital requirements. This transition also aligns with operational flexibility, allowing producers to better navigate demand uncertainty.

Simultaneously, semi-finished imports emerged as a critical channel for nickel inflow. Nickel content via stainless steel slab imports surged 82% to 58,796 t, indicating a growing preference for upstream processed materials that embed nickel. This route enables mills to bypass direct exposure to raw nickel price volatility while ensuring steady feedstock availability. However, this trend was selective -- nickel content through billet imports declined 45% to 4,803 t, suggesting that mills prioritised specific semi-finished forms based on cost efficiency and downstream requirements.

Another notable shift was the 33% drop in nickel content through finished stainless steel imports, which fell to 34,659 t. This indicates improved domestic substitution and a cautious approach toward higher-cost finished imports amid weak demand conditions.

What's driving the shift?

The transition is fundamentally cost-led. Scrap has emerged as the most economical and flexible alternative, while slab imports offer a strategic hedge by embedding nickel within semi-finished products. Together, these channels have effectively displaced a significant portion of primary nickel inputs.

Near-term outlook

India's nickel consumption pattern is expected to remain skewed toward scrap and semis in the near term. As long as scrap maintains its cost advantage and global availability remains stable, it will continue to dominate the sourcing mix. Semis, particularly slabs, will act as a tactical lever based on margin dynamics. A recovery in NPI and FeNi demand would depend on a meaningful correction in their pricing relative to scrap and a sustained improvement in stainless steel demand. Until then, Indias nickel strategy will remain anchored in cost optimisation, supply flexibility, and indirect sourcing routes.