20-March-2026

- Domestic prices rise sharply along with global benchmarks

- Scrap supply tightens across Gulf dependent routes

While benchmark prices on the LME have reacted sharply breaching the $3,500/t level, the real shift in India is happening at the ground level. Trade activity has slowed, supply visibility has reduced, and participants are increasingly factoring in logistics and availability risks rather than just price trends.

This marks a transition from a price-driven market to a risk-driven one.

Export disruptions pressure trade flows

Beyond imports and domestic supply, India's aluminium export chain is now facing visible strain.

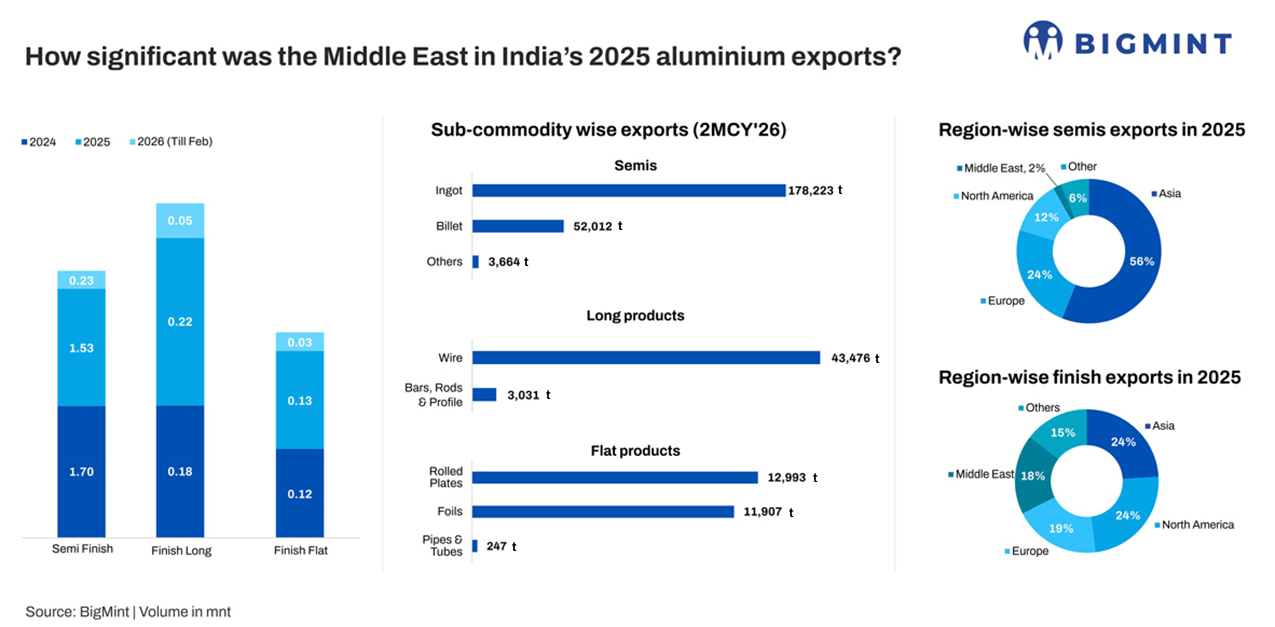

Exporters shipping aluminium products such as coils and sheets to the Gulf are encountering delays, rerouting, and rising uncertainty. Shipments that have already left Indian ports are being diverted to alternative hubs like Khor Fakkan and Fujairah, often before crossing critical maritime routes.

Logistics operators are prioritising essential cargo, leading to delays of up to two to three weeks for non-essential industrial shipments such as aluminium products.

For exporters, this creates a dual challenge. Existing cargo is delayed and costlier, while fresh orders are slowing as buyers remain uncertain about delivery timelines.

Trade finance and order flows tighten

The disruption is not limited to physical movement of goods. It is also beginning to affect the financial side of trade.

Banks and financial institutions are showing greater caution in financing export orders linked to the Gulf. This is slowing down new bookings, particularly for small and medium exporters in the aluminium downstream segment.

As a result, exporters are facing pressure on both ends. Current shipments are stuck in transit, while future order pipelines are becoming less certain.

This weakening of order visibility is adding another layer of caution across the aluminium value chain.

Freight escalation reshapes export economics

Freight dynamics are rapidly altering the economics of aluminium exports.

Container freight rates have increased to nearly $4,000 per container, significantly raising the landed cost for buyers. In many cases, additional rerouting and handling charges are being imposed, which are ultimately passed on to customers.

Shipping lines such as Mediterranean Shipping Company and Hapag-Lloyd are adjusting routes and reducing frequency on high risk corridors, contributing to longer transit times and limited vessel availability.

For aluminium exporters, this creates a difficult trade off. Higher global prices may support margins, but rising logistics costs and delivery uncertainty are eroding competitiveness in key markets.

Container congestion begins to impact production

The slowdown in cargo movement is also creating operational challenges within India.

With fewer vessels available and sailings becoming irregular, containers are increasingly getting stuck at factory locations. For aluminium product manufacturers, this is starting to affect plant operations.

As finished goods accumulate and dispatches slow, working capital gets locked in inventory. This can lead to production adjustments, especially for exporters with continuous manufacturing cycles.

The issue is particularly relevant for flat-rolled product manufacturers and downstream units that depend on steady export flows.

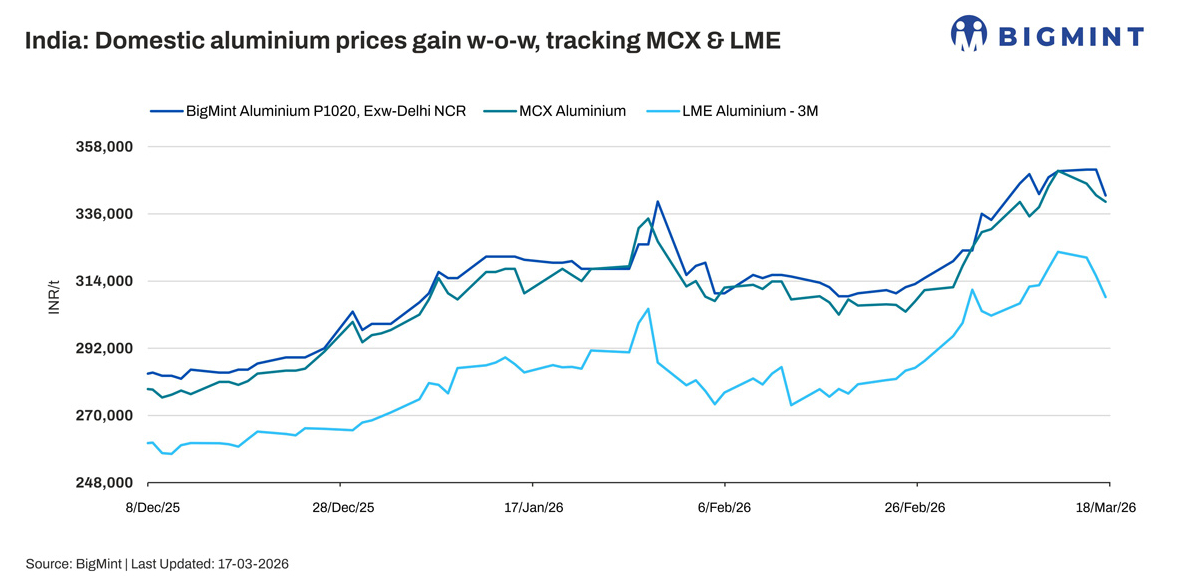

Domestic prices align with global levels

Domestic aluminium prices have increased in line with global benchmarks. Prices in domestic markets have increased by INR 25,000-30,000/t since the time the Middle East tension started. Additionally, the demand for primary aluminium has also remained firm with good buying interest in the market. The premiums in the domestic market hover between $300-320/t above LME cash.

Indias primary aluminium producers are relatively better positioned as the cut in material arrival from the Middle East region could boost demand for domestically available material.

Higher global prices are supporting realisations, and domestic supply availability remains stable compared to the scrap-dependent segment. However, input cost pressures linked to freight and raw materials remain a risk if disruptions persist.

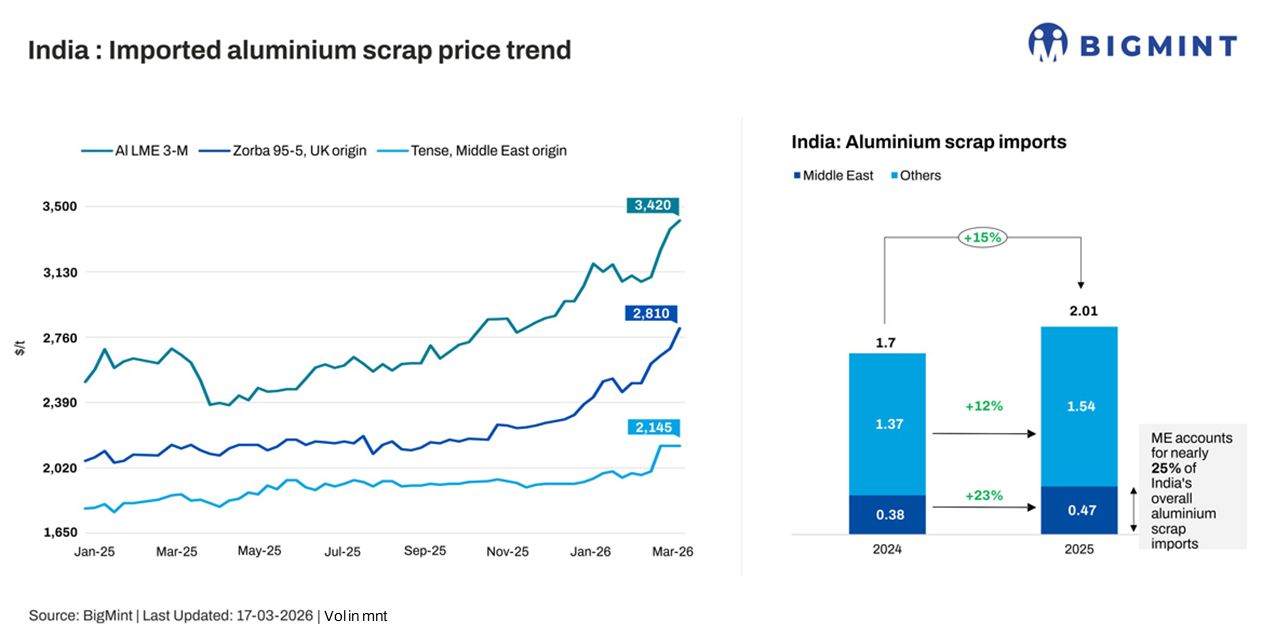

Scrap flows tighten across key corridors

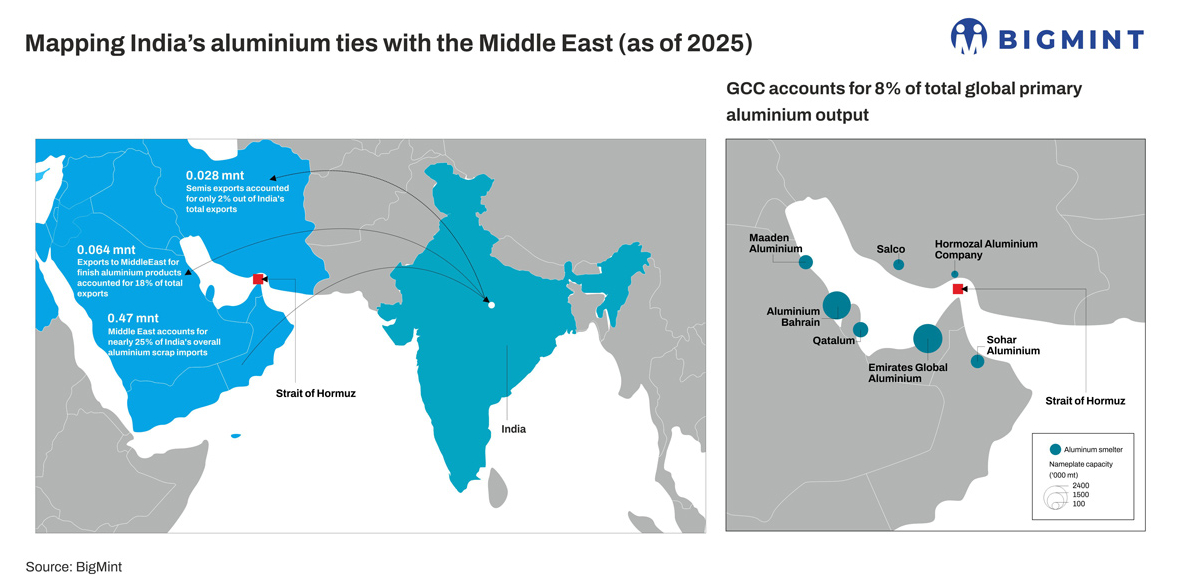

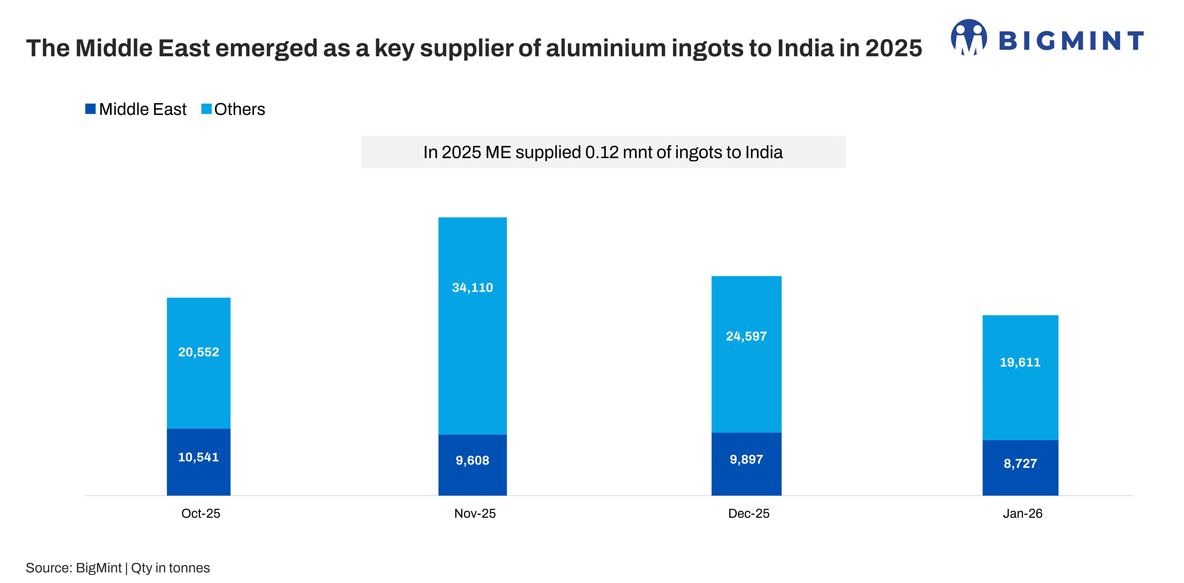

India's dependence on imported scrap is now becoming a more visible risk. With nearly 25% of scrap imports coming from the UAE and Saudi Arabia, disruptions in the Gulf are directly tightening supply. Logistics challenges at key regional ports are reducing the availability of material in the near term.

Scrap inflows were already showing signs of moderation before the escalation. The current situation is accelerating that trend, leading to tighter availability across the secondary aluminium value chain.

For recyclers, die casters, and alloy producers, the issue is no longer just higher prices. It is the lack of predictable supply. The higher LME levels, rising freight rates have also kept scrap prices from other origins also higher.

Outlook depends on supply chain visibility

The near-term outlook for India's aluminium market is closely tied to how quickly supply chain visibility improves. If shipping routes stabilise and freight conditions ease, trade activity could recover gradually. However, if disruptions continue, both imports and exports will remain constrained, keeping costs elevated and market sentiment cautious.