25-April-2026

- Market shifts from surplus to deficit year-on-year

- Indonesia policy reset reshapes global cost curve

A market that entered 2026 burdened by a 283,000-tonne surplus is being reshaped-quarter by quarter - by Indonesian quota cuts, a revised ore-pricing benchmark, and a demand mix increasingly split between stable stainless steel and a slowing battery-chemistry shift.

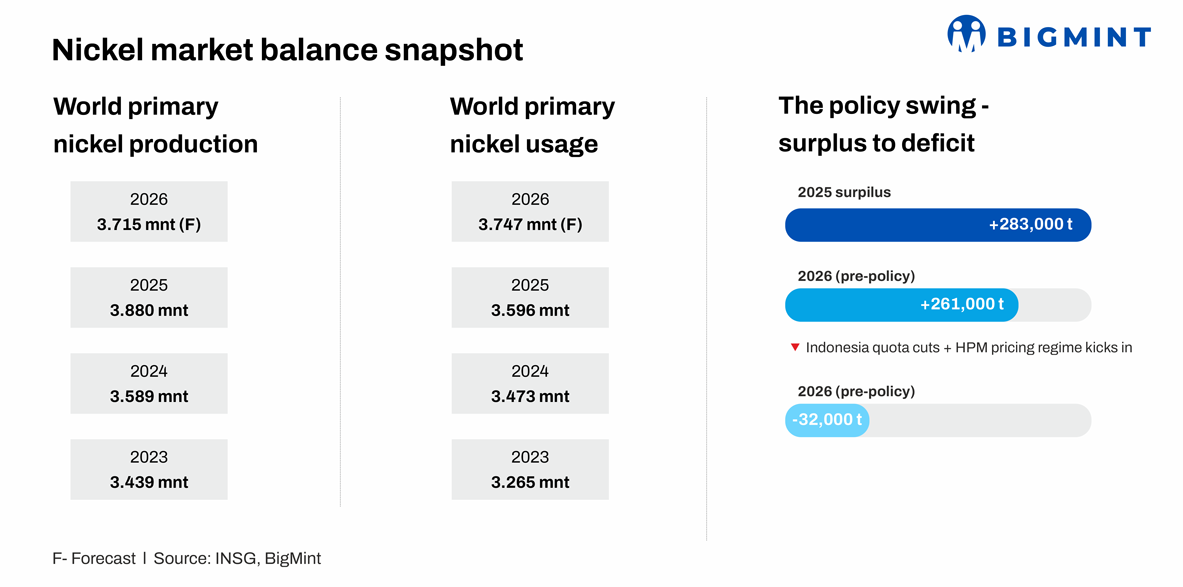

Nickel's 2026 outlook is turning tighter, but the market is still navigating a large 2025 surplus that keeps prices capped. The key swing factor is Indonesia: tighter ore quotas and a new pricing regime are now enough to move the market from the INSG's (International Nickel Study Group's) expected 261,000 tonnes (t) surplus in 2026 to an estimated 32,000 t deficit, while 2025 remains in surplus at about 283,000 t.

The INSG April 2026 outlook indicates a clear shift in market balance, with a surplus of 283,000 t in 2025 expected to reverse into a deficit of 32,000 t in 2026. This marks a significant change from earlier projections of a 261,000 t surplus for 2026, prior to Indonesia's tighter supply policies. The group also estimates global primary nickel production at 3.715 million t against consumption of 3.747 million t, pointing to a modest but notable supply shortfall.

Indonesia dominates supply dynamics

Indonesia still dominates global nickel supply growth, especially through NPI and HPAL, and market estimates commonly place it near 60% of global output. That makes Indonesian policy changes disproportionately important for the world balance, because even modest quota reductions can overwhelm small demand changes elsewhere.

Additionally, Vale Indonesia suspended mining activity after delays in 2026 plan approval, and that officials were aiming to align quotas with domestic smelter needs. While, Weda Bay Nickel received a sharply lower quota for 2026 versus 2025, underscoring how aggressive the policy reset has become.

HPM pricing lifts cost base

Indonesia's revised HPM (Harga Patokan Mineral) benchmark, effective 15 April 2026, raises the floor price for nickel ore sold domestically. The new HPM has limited impact on RKEF (rotary kiln electric furnace) costs but materially raises the cost base for HPAL operations, whether integrated or not.

That matters because HPAL plants are more sensitive to ore pricing and reagent costs than many RKEF operations, so the pricing change can compress margins and slow the pace of HPAL expansion even if ore remains available. In short, the policy does not just lift costs; it selectively squeezes the growth engine for nickel units aimed at batteries.

Demand remains mixed

Nickel demand is still led by stainless steel, which remains the main absorber of primary nickel in the global market. Even in 2026, stainless demand is the most stable pillar, while battery demand is more sensitive to chemistry shifts, EV growth rates, and inventory digestion.

The battery side is becoming less nickel-intensive at the margin because (lithium iron phosphate) LFP adoption is taking share from nickel-rich chemistries in mass-market EVs. That does not eliminate battery demand for nickel, but it slows the incremental growth rate that markets had once assumed.

So the demand picture is mixed: stainless steel provides the base load, but EV batteries no longer guarantee the same pace of nickel demand growth because LFP reduces nickel intensity per vehicle. That is one reason the market can tighten in 2026 even without a boom in end-use demand.

Surplus overhang and risks persist

Despite the projected deficit, the large surplus from 2025 is expected to act as a buffer, delaying any sharp price rally.

Geopolitics and shadow inventory- INSG flagged uncertainty around the Middle East conflict. Russian supply and broader LME shadow inventories continue to affect price discovery and physical availability - particularly in markets sensitive to sanctions.

Operational disruptions- Sulphur, energy, and logistics constraints can slow HPAL and smelting ramp-ups; mine-plan approval delays (as seen at Vale Indonesia) can interrupt supply before the market fully tightens.

2025 surplus overhang- With 283,000 t of surplus nickel estimated in 2025, existing inventory acts as a buffer - keeping prices capped even as the 2026 balance formally tips to deficit. Drawdown pace will determine when prices genuinely tighten.

Indonesia policy reversal- If quotas are revised upward, ore imports rise, or HPM pricing is softened, the projected 2026 deficit could disappear rapidly. Conversely, further enforcement tightening could spike prices well beyond current demand fundamentals.

Outlook

Nickel prices are expected to remain firm but volatile in the near term, supported by tightening fundamentals and higher production costs. However, sustained price upside will depend on the pace of inventory drawdown and continued enforcement of Indonesia's supply discipline.