21-April-2026

- India remains key driver of aluminium scrap demand

- China's scrap imports reach 5-year high in CY'25

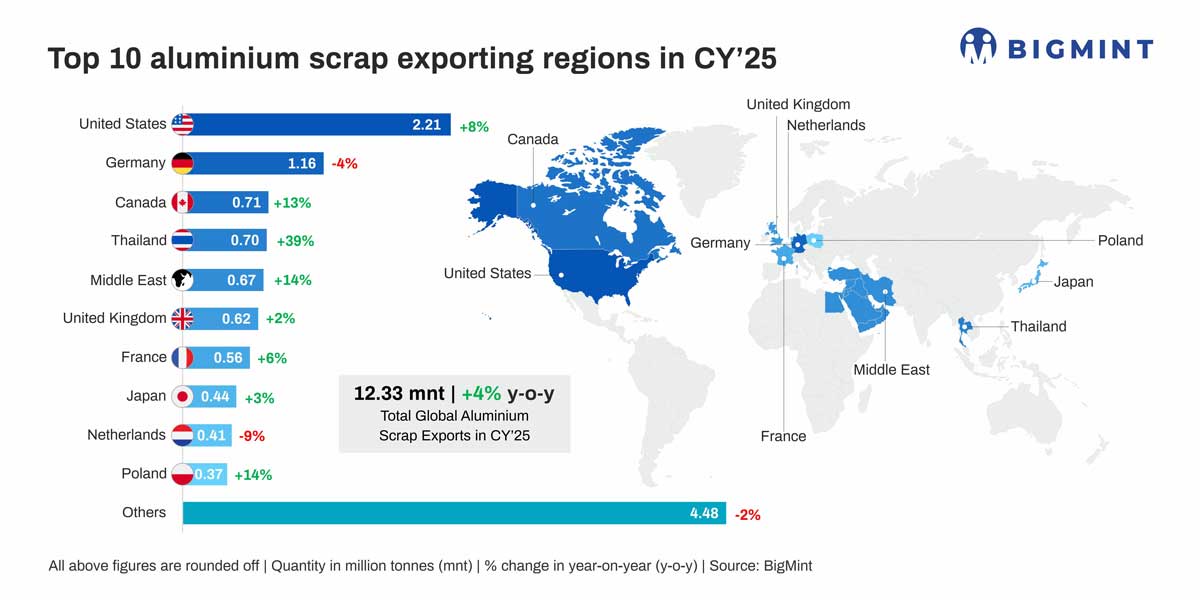

Global aluminium scrap trade volumes, including intra-European trade, increased to 12.33 mnt in CY'25 from 11.90 mnt in CY'24, reflecting a 4% y-o-y rise and highlighting resilient demand across key consuming regions.

India remained a key demand driver during the year, with aluminium scrap imports rising to 2.02 mnt from 1.74 mnt, marking a 16% y-o-y increase. This growth was supported by strong downstream consumption and continued reliance on imports from the EU, UK, and the Middle East, reinforcing its position as a major global scrap consumer.

Global scrap trade drivers

Global aluminium scrap trade flows picked up in CY'25 despite firm primary output, primarily driven by rising demand across the global market and structural supply constraints.

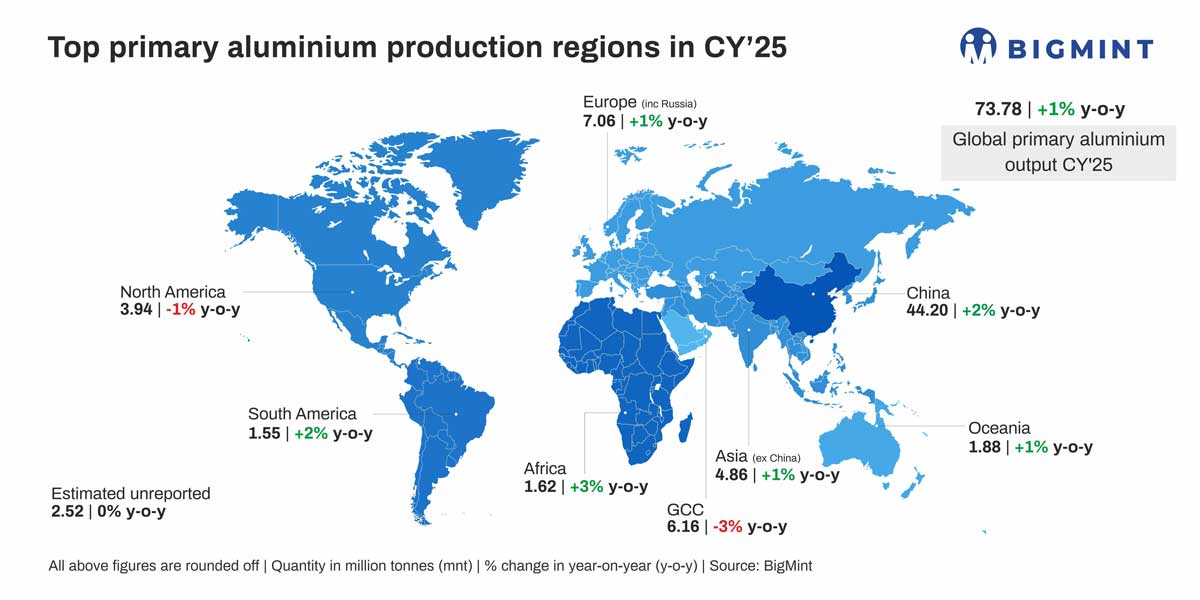

Although global primary aluminium production increased marginally to around 73.8 mnt, supply growth remained constrained, particularly in China, which continues to operate close to its 45 mnt capacity cap. Strong domestic demand and high smelter utilisation levels have limited further expansion in primary output, pushing the market to increasingly rely on secondary aluminium.

At the same time, China's secondary aluminium consumption rose to approximately 13.35 mnt in 2025, reflecting a 5% y-o-y increase. This growth has been supported by policy measures promoting recycling and expansion in secondary aluminium capacity. However, domestic scrap availability, estimated at around 11.8 mnt, has not kept pace with rising demand, creating a clear supply gap.

This imbalance has positioned China as a key driver of global scrap trade. The country increased its imports significantly to bridge the deficit, with aluminium scrap imports reaching nearly 2.01 mnt in 2025, marking a five-year high. This trend underscores the growing importance of scrap in China's aluminium value chain and its increasing integration into global trade flows.

Overall, the combination of tight primary supply and rising secondary demand supported stronger global aluminium scrap trade momentum during CY'25.

Major exporting countries and shifting trade dynamics

The United States retained its position as the leading exporter of aluminium scrap in CY'25, with export volumes rising 8% y-o-y. In contrast, Germany, one of the largest exporters within Europe, recorded a 4% decline, reflecting weaker industrial activity.

Other exporting regions demonstrated stronger momentum. Scrap exports from the Middle East increased by 14%, while Thailand saw a sharp rise of 39%, supported by stronger regional trade flows. Canada's exports grew by 13%, while the United Kingdom remained relatively stable with a modest 2% increase, reflecting a more constrained operating environment.

Regional trade flow

In the United States, export growth was supported by elevated aluminium prices, high regional premiums, and wider mill spreads, which influenced scrap availability and pricing behaviour. Operational disruptions at recycling-linked facilities and evolving domestic demand conditions further shaped trade flows.

Thailand emerged as a key destination for US aluminium scrap, with exports rising to 0.47 mnt, up from 0.35 mnt in CY'24. This increase was supported by strong procurement from Thai processing facilities and efficient logistics. Well-structured financing mechanisms, often backed by large Chinese enterprises, further supported liquidity and strengthened downstream trade flows into Asia.

Exports from the US to India increased marginally to 0.42 mnt, although the trend remained uneven throughout the year. In the early part of 2025, shipments were impacted by strong domestic demand in the US following tariff-related shifts. However, in the latter half of the year, rising domestic scrap availability and weaker demand supported increased export allocations.

Meanwhile, exports to Malaysia declined to 0.29 mnt, reflecting shipment disruptions caused by tighter inspection measures, port congestion, and extended clearance timelines.

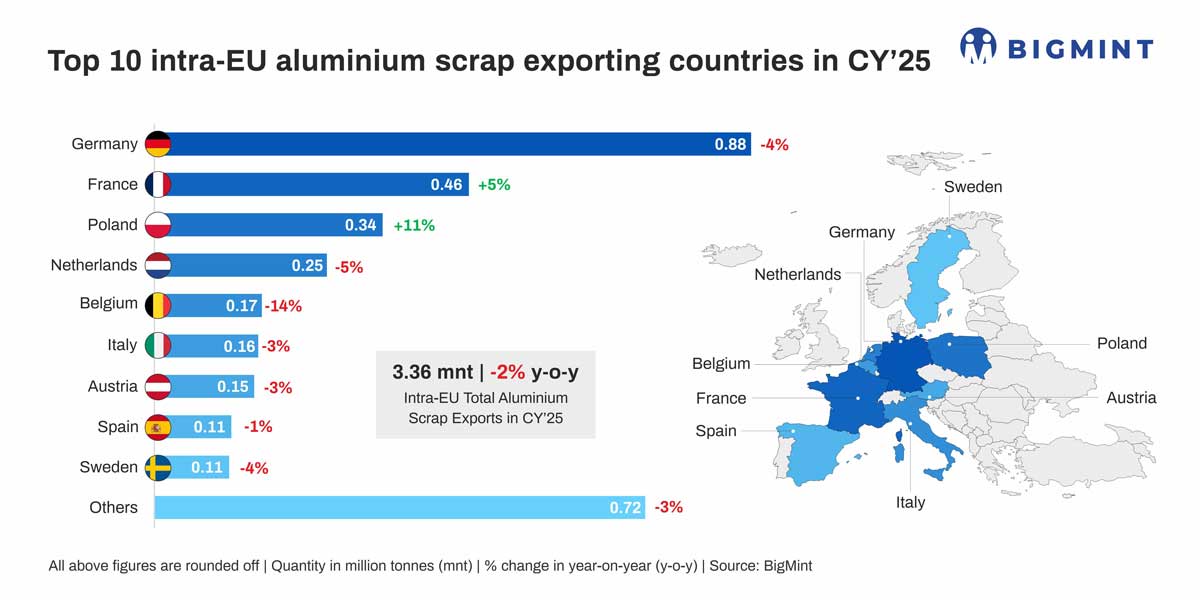

Within the EU-27, intra-regional scrap trade weakened, declining to 3.36 mnt, as subdued activity in the automotive and construction sectors weighed on demand. Exports to external markets remained broadly stable at 1.27 mnt, despite declines from key suppliers such as Germany and Belgium. Structural challenges, including high energy costs, regulatory constraints, and limited recycling infrastructure, continued to impact scrap availability in the region.

Policy developments in Europe have also played a significant role. Increased focus on reducing scrap leakage under circular economy goals, coupled with stricter waste shipment regulations and the implementation of CBAM from January 2026, is expected to further support domestic recycling and tighten export availability.

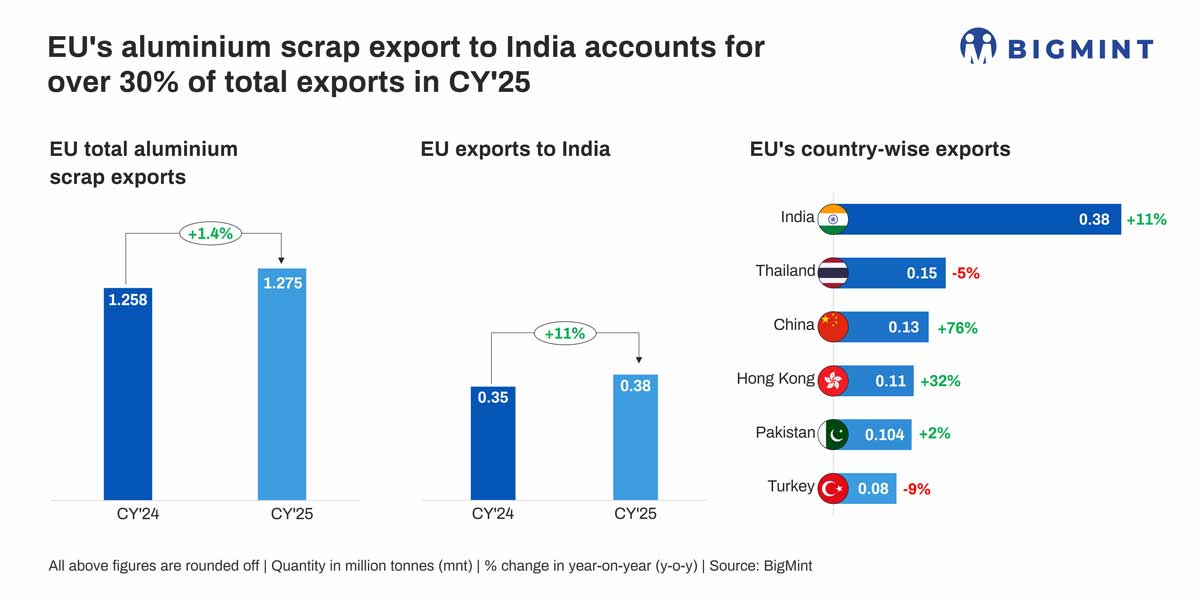

On the other hand, EU aluminium scrap exports recorded a modest increase in CY'25, with shipments to India rising at a notably faster pace. India remained the largest destination, accounting for over 30% of total exports.

Following US tariff-led disruptions in early 2025, India accelerated sourcing from alternative suppliers such as the EU, UK, and the Middle East.

Robust demand from Asian markets, particularly China and Hong Kong, further supported overall trade flows, despite mixed trends across other key import destinations.

In the Middle East, aluminium scrap exports increased to 0.67 mnt, supported by higher recycling activity and expansion of processing capacity in key countries such as Saudi Arabia and the UAE. India remained the largest importer from the region, accounting for a significant share of total exports, driven by strong demand across construction, infrastructure, and industrial sectors.

Canada recorded a 13% increase in scrap exports, supported by stronger cross-border flows to the United States. This trend was influenced by tariff-driven sourcing adjustments and evolving domestic supply conditions in the US market.

The United Kingdom saw relatively stable export performance, with volumes reaching 0.62 mnt. However, the market continued to face challenges from tighter environmental regulations, rising energy costs, and cautious trading sentiment, which limited stronger growth in exports despite supportive price conditions during parts of the year.

Outlook for CY'26 and beyond

Looking ahead, global aluminium scrap trade is expected to face heightened uncertainty in 2026. Tightening export controls in the EU under circular economy policies, the full implementation of CBAM, and tariff-led trade shifts in the United States are likely to reshape trade flows.

At the same time, escalating geopolitical tensions in the Middle East, including disruptions to key aluminium facilities and logistical constraints across critical shipping routes, are expected to create periodic supply tightness and increase price volatility.

India is likely to remain a key demand driver, supported by its high dependence on imports. However, tightening availability from major exporting regions and logistical challenges may keep prices firm.

China's increasing focus on recycling, with targets to exceed 15 mnt of recycled aluminium output, is expected to further boost domestic scrap consumption. This could tighten global scrap availability and intensify competition for material.

Overall, while capacity expansions in the Middle East may provide some relief, a stronger policy push to retain scrap domestically across regions suggests that global scrap markets may remain structurally tight in the near to medium term.

How will global aluminium scrap trade dynamics evolve in the coming years? How will the recycling momentum in India and China drive sustainable transformation in the industry? How is global scrap supply tightening affecting the low-carbon transformation of the industry? Join industry leaders at BigMint India Non-Ferrous Week (BINFW), taking place in Mumbai on 9-10 June, and be part of insightful discussions shaping the future of the non-ferrous metals industry.