14-April-2026

- Green aluminium transition still at early stage

- Power shift critical for global competitiveness

India's aluminium industry is entering a defining phase where its ambitions extend beyond domestic growth. The real opportunity lies in whether India can position itself as a competitive exporter of green aluminium, at a time when global markets are rapidly shifting toward low carbon materials.

With demand rising, capacity expanding, and sustainability becoming central to trade, the question is no longer just about growth. It is about whether India can align scale with decarbonisation to unlock export potential.

Scale creates natural export opportunity

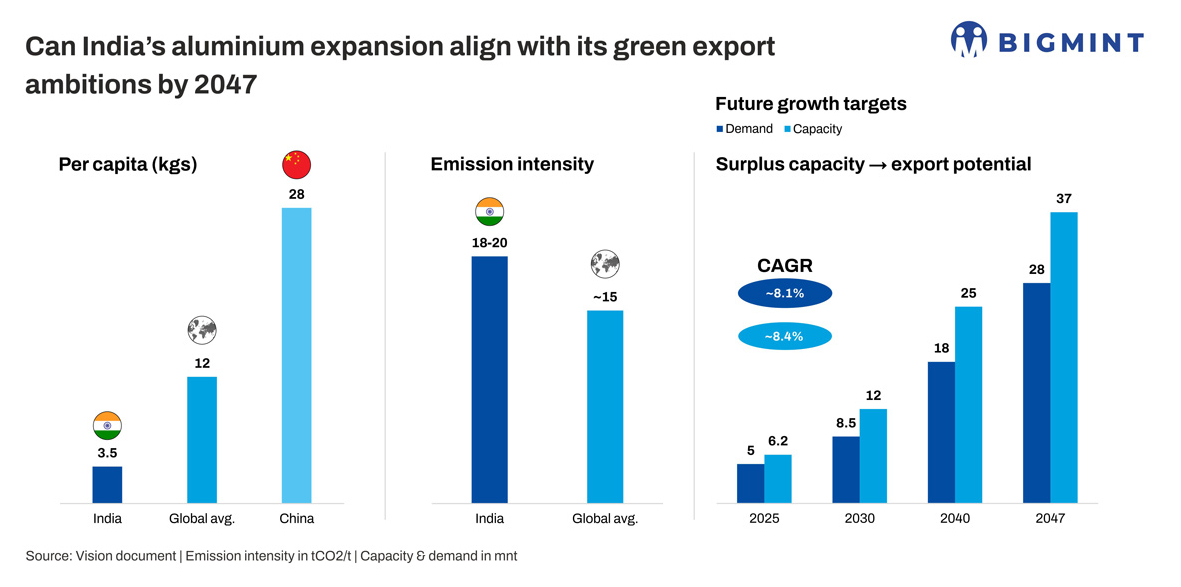

India's aluminium demand is expected to grow sharply from current 4.8 mnt in 2025 to around 28 million tonnes (mnt) by 2047, driven by infrastructure, electric mobility, and renewable energy expansion.

On the supply side, capacity is projected to reach 37 mnt, creating a structural surplus. This gap between production and domestic consumption naturally positions India as a potential export-oriented market.

The country is already aiming to increase its share in global aluminium trade from 3.8% to 10%by 2047, signalling clear export intent.

Emissions remain key constraint

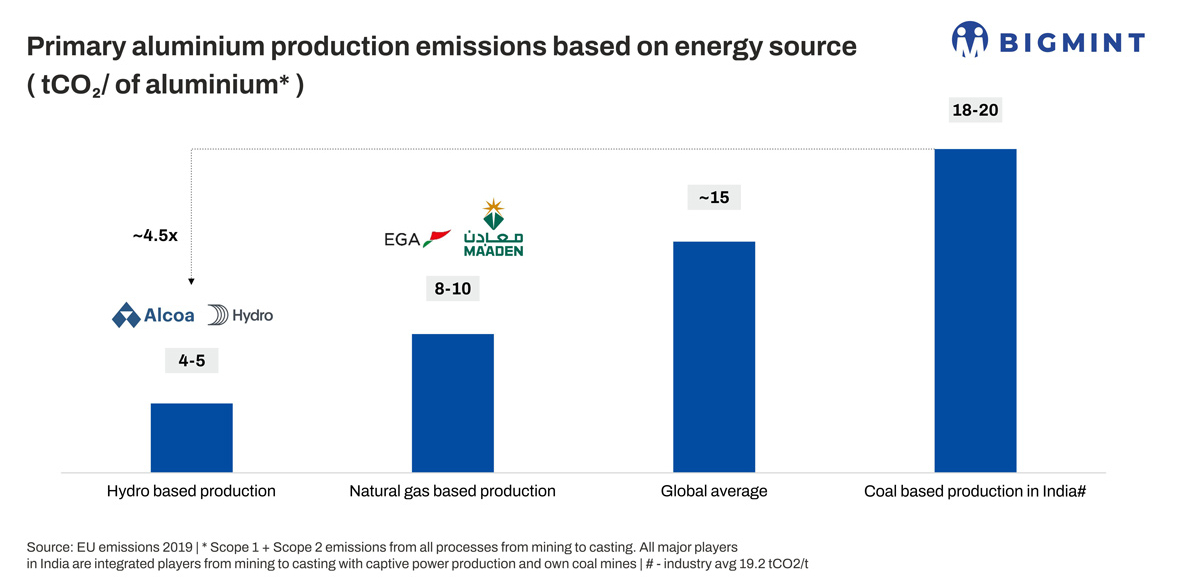

Despite its scale advantage, India faces a structural challenge in the form of high carbon intensity.

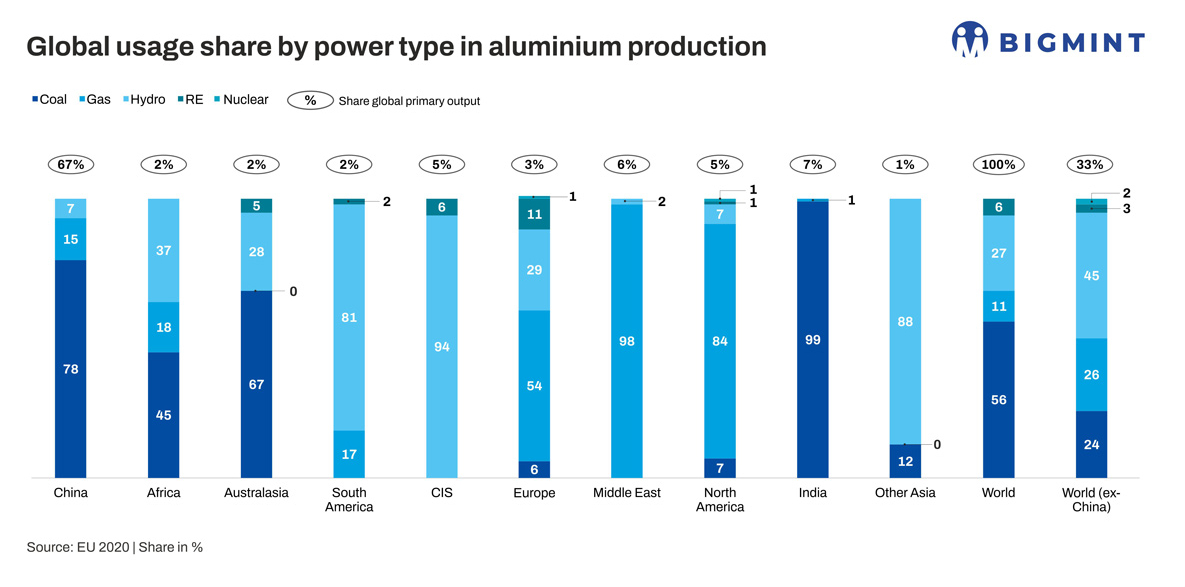

Aluminium production in India emits around 18-20 t of CO2 per tonne, compared to a global average of about 15 t. The primary reason is the sector's ~99%reliance on coal-based power.

As global buyers increasingly prioritise low carbon sourcing, this creates a risk. India may remain cost competitive, but not necessarily carbon competitive, which is becoming equally important in international markets.

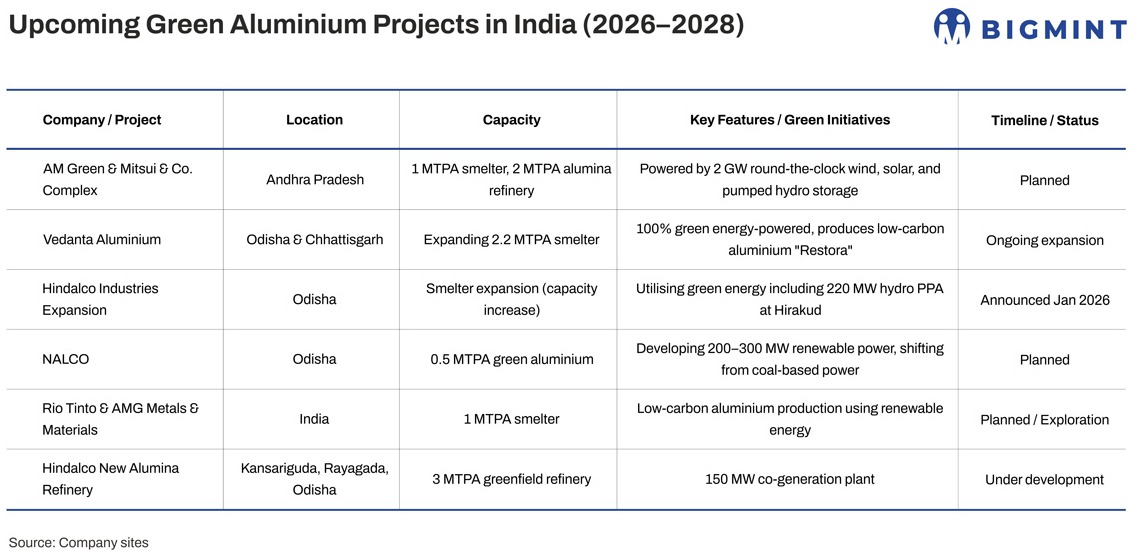

Green aluminium transition begins, but slowly

India is gradually moving toward green aluminium production.

Producers are integrating renewable energy through solar, wind, and hybrid models, and new capacities are being designed with improved energy efficiency. Some companies have also started offering low carbon aluminium products to cater to global buyers seeking greener materials.

However, the transition is still in its early stages and remains uneven across the industry.

![]()

Recycling strengthens the green export case

Secondary aluminium offers a major advantage in the green transition. It requires up to 95%less energy than primary production.

Indias current recycling rate is around 30%, leaving significant room for improvement. Scaling this up can directly lower emission intensity and enhance Indias positioning as a green supplier.

Power transition will decide the outcome

Electricity accounts for 70-75%of aluminium production costs and emissions, making it the single most important factor.

While renewable energy adoption is increasing, challenges remain due to the need for uninterrupted power supply in smelting operations.

The future likely lies in a hybrid energy mix, combining:

- Renewable energy

- Storage solutions

- Grid integration

- Potential nuclear options such as SMRs

Without a meaningful shift in power sources, India's green aluminium ambitions will remain constrained.

Global competition is already moving ahead

Regions like the Middle East are emerging as lower carbon aluminium producers, supported by cleaner energy mixes.

At the same time, global buyers are increasingly factoring in carbon footprint alongside price, reshaping procurement strategies.

This means Indias export success will depend not just on scale, but on how quickly it can close the carbon gap.

Green aluminium demand and export opportunity

Green aluminium demand is rising across sectors where sustainability is becoming non-negotiable. In India, key consumers include automotive and EV manufacturers, renewable energy developers, packaging, and construction, all of which are aligning with lower carbon material sourcing.

The European Union remains the most critical market, where the Carbon Border Adjustment Mechanism is expected to penalise high emission imports, making low carbon aluminium a competitive advantage.

To stay relevant, India may need to ring fence nearly 4 to 5 mnt of certified green aluminium capacity for exports.

North America is another key destination, driven by increasing demand from automotive and packaging sectors transitioning to sustainable sourcing.

In Asia, countries such as Japan and South Korea are gradually integrating green procurement standards, offering continuity for India's existing trade relationships. Additionally, emerging markets in Africa and the Middle East present long term opportunities, particularly for downstream and alloyed aluminium products.

How will Indian aluminium producers cater to fast-expanding demand globally for lower CO2-embedded metals products? Over and above integration of RE, what other energy efficiency measures need to be taken to mitigate emissions? How will CBAM and carbon markets at home and abroad drive the transition in the aluminium sector? Hear experts deliberate on these issues and much more at the BigMint India Non-Ferrous Week (BINFW)in Mumbai on 9-10 June.