25-April-2026

- Indonesia strengthens dominance in India's coke market

- AM/NS India and JSW Steel remain major importers

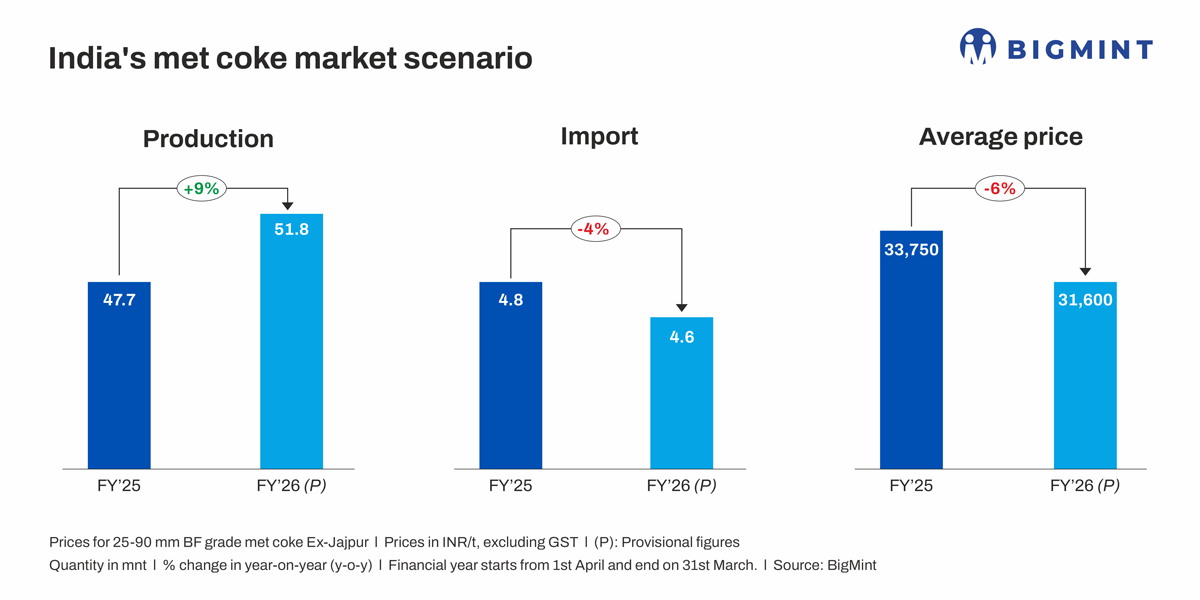

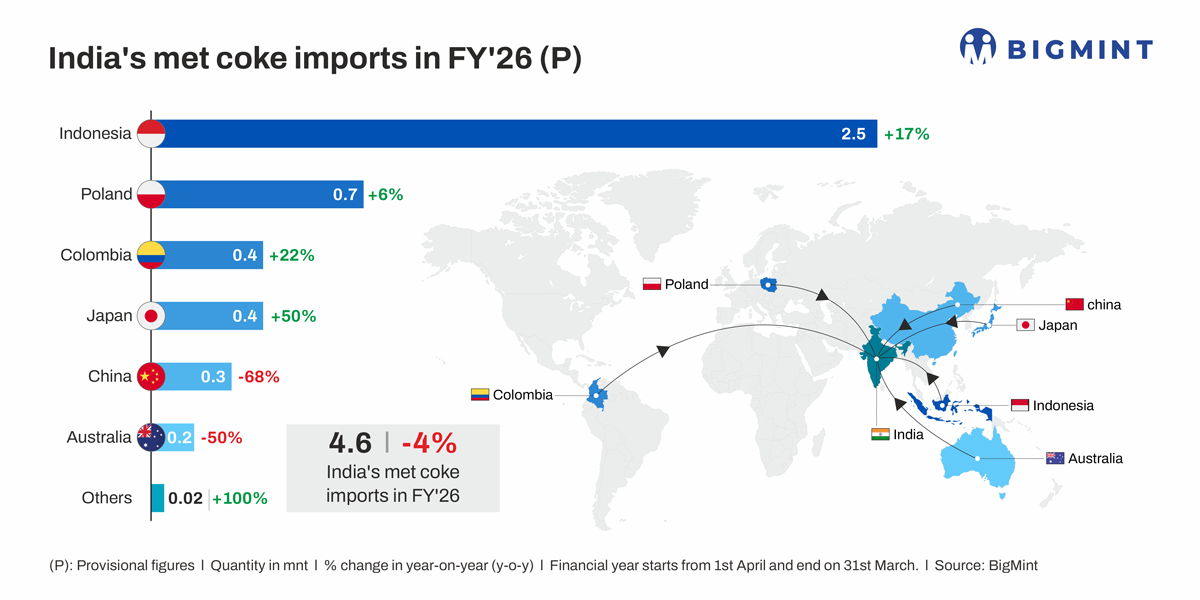

India's metallurgical coke (met coke) imports recorded a marginal decline of around 4% y-o-y in FY'26 to 4.62 million tonnes (mnt), compared with 4.81 mnt in FY'25.

The slight contraction reflects relatively subdued demand conditions and cautious procurement strategies adopted by steelmakers amid improved domestic availability and inventory optimisation. Despite the overall decline, sourcing patterns across supplier countries and cargo movement across ports displayed notable shifts during the year.

Country-wise trend: Indonesia consolidates dominance

On the supply side, Indonesia further strengthened its position as India's leading met coke supplier in FY'26. Imports from Indonesia increased by 17% y-o-y to 2.53 mnt from 2.16 mnt in FY'25, supported by competitive pricing, geographical proximity, and consistent supply availability.

Poland also registered a moderate increase of 6% to 0.74 mnt, reflecting stable inflows from European suppliers. Imports from Japan rose by 22% to 0.39 mnt, primarily driven by demand for higher-quality coke from integrated steel producers.

Meanwhile, imports from Colombia surged by 50% to 0.39 mnt, suggesting diversification of sourcing as buyers explored alternative origins amid supply constraints in traditional markets. In contrast, shipments from China declined sharply by 68% y-o-y to 0.28 mnt, while Australian volumes dropped by 50% to 0.15 mnt. The decline from these origins was largely attributed to relatively higher costs, limited export availability, and weaker competitiveness compared with lower-cost Asian suppliers.

AM/NS India, JSW major importers, but volumes drop

At the company level, procurement strategies varied significantly among major buyers. AM/NS India remained the largest importer despite a 21% y-o-y decline to 1.14 mnt, likely reflecting improved inventory management, partial substitution with domestic coke, and enhanced blast furnace efficiency.

JSW Steel maintained relatively stable imports at 0.36 mnt, indicating steady consumption and a balanced sourcing approach. In contrast, Tata Steel recorded a sharp 62% drop to 0.27 mnt, suggesting reduced dependence on imported met coke, possibly due to higher utilisation of captive or domestic supplies and optimisation of coke consumption rates. Similarly, IMR Resources witnessed a 56% decline to 0.15 mnt, reflecting softer trading activity or reduced downstream demand.

Meanwhile, some smaller players expanded their procurement. India Coke & Power increased imports by 14% to 0.16 mnt, supported by improved offtake from industrial consumers. Rashmi Group recorded a notable 75% increase to 0.14 mnt, albeit from a lower base, driven by higher operational utilisation and incremental demand.

Eastern ports emerge as key gateways

Port-level data indicates a gradual shift in import activity toward eastern India, reflecting stronger demand from steel plants located in the region. Vizag handled around 1.1 mnt of met coke in FY'26, registering a 23.7% y-o-y increase supported by higher cargo inflows. Haldia recorded the strongest growth among major ports, with volumes rising 62.8% y-o-y to approximately 1.1 mnt, driven by increasing demand from eastern steel producers and improved port logistics.

Conversely, Hazira witnessed a 21.3% y-o-y decline to 1.14 mnt, reflecting relatively weaker demand in western India and possible inventory adjustments among buyers. Imports through Paradip also softened by 8% to 0.74 mnt, indicating moderate demand conditions, while Krishnapatnam handled around 0.2 mnt, marking a 23% y-o-y decline.

Overall, the fall in imports during FY'26 was largely driven by reduced demand in western and southern regions, improved domestic coke availability, and cautious procurement strategies by steelmakers. However, stronger inflows through eastern ports and increased sourcing from Indonesia helped partially offset the decline.

Domestic met coke production strengthens in FY'26

India's domestic met coke production increased significantly in FY'26, reaching around 51.7 mnt, marking a 9% y-o-y rise from FY'25. A large share of this output - approximately 91% - came from captive production by integrated steel producers. The increase in domestic output helped reduce reliance on imports and supported the cautious procurement approach adopted by several steelmakers during the year.

Policy developments: Import curbs followed by AD duty

Government policy interventions also influenced the import landscape during the year. In Dec'24, the Indian government imposed quantitative restrictions on imports of LAM coke (ash content below 18%), following complaints from domestic producers that cheaper imports - particularly from Indonesia - were eroding profitability and forcing local plants to operate at lower capacity utilisation.

At that time, India's merchant met coke industry had an installed capacity of around 8 mnt, while actual production in FY'25 stood at nearly 4 mnt, highlighting significant underutilisation. The import curbs were initially imposed for six months until June and were subsequently extended until 31 December. Quarterly import allocations were set at 713,583 t, with the full-year volume capped at 2.85 mnt.

Following the expiry of these restrictions, the government introduced a provisional anti-dumping duty on LAM coke imports for a period of six months to protect domestic manufacturers from low-priced overseas supplies. The duty ranges between $60.87/t to $130.6/t depending on the country of origin and applies to imports from China, Indonesia, Colombia, Japan, and Russia. At the same time, the government withdrew the quantitative import restrictions, making imports of LAM coke freely permissible.

Price trend: Input costs limit sharper decline

Domestic metallurgical coke prices in India declined by around 6% y-o-y in FY'26, mainly due to softer demand and improved domestic availability. However, elevated coking coal costs from earlier bookings, higher imported met coke prices amid firm freight rates, and supportive steel and pig iron prices helped limit the overall price decline.

Outlook: Imports likely to remain range-bound

Domestic supply may improve following Synergy Capital's acquisition and restart of met coke production at Saurashtra Fuels in January, targeting the merchant market in western India. This development could moderately reduce Indias reliance on imports.

Going forward, India's met coke imports are expected to remain largely range-bound, with only gradual growth aligned with steel demand. Indonesia is likely to retain its dominant share due to cost advantages, while steelmakers are expected to maintain cautious and optimised procurement strategies.