25-April-2026

- Imports to stay firm amid supply constraints

- JSW Steel dominated imports with sharp rise

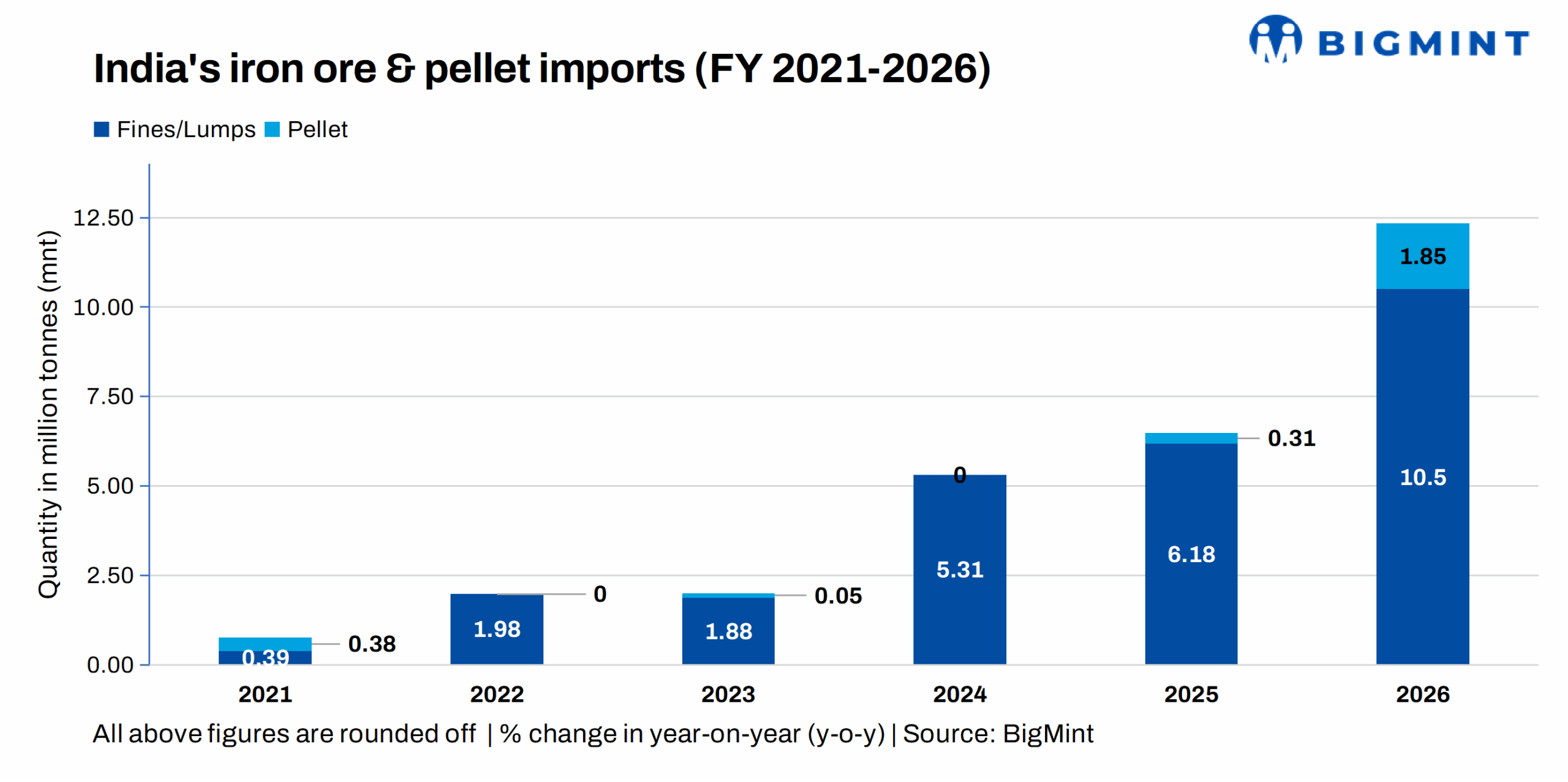

Indias iron ore imports rose to 12.35 million tonnes (mnt) in FY'26, a seven-year high, according to BigMint data. Imports nearly doubled y-o-y from 6.49 mnt in FY25, driven by rising domestic steel demand, supply constraints in key mining regions due to suspension of activities, a prolonged monsoon, and fluctuations in global iron ore prices. Of the total, 10.5 mnt comprised fines and lumps, while pellets accounted for 1.85 mnt.

This marks the highest level since 2018 and only the third instance of annual imports exceeding 10 mnt.

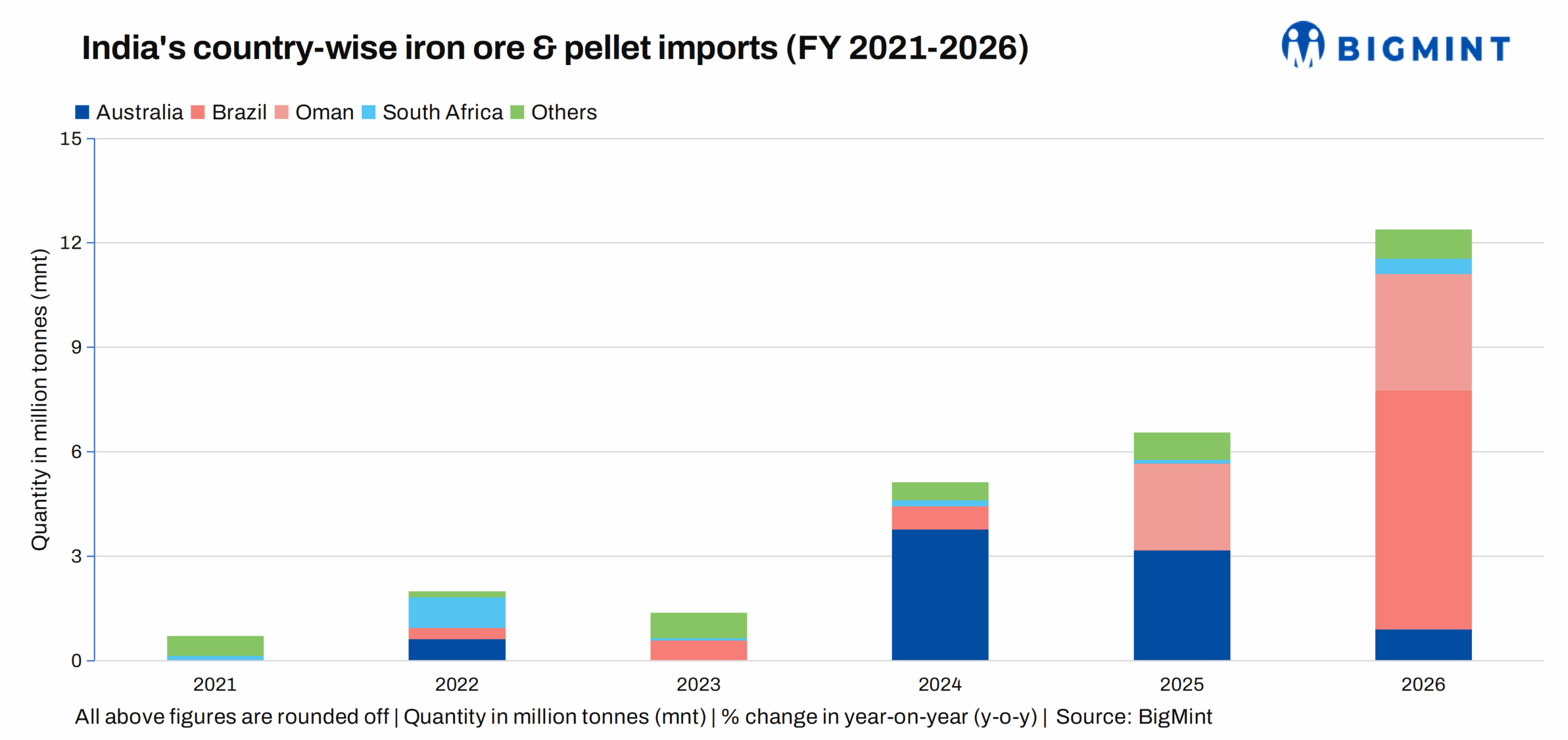

Brazil leads exports as supplier mix shifts

Brazil replaced Australia as the largest supplier in FY'26, with shipments of around 6.86 mnt. In FY'25, Australia led exports to India at 3.17 mnt; however, its share declined to 0.9 mnt this year. The shift was primarily driven by stronger demand for high-grade ore and improved price competitiveness of Brazilian material.

In pellets, Oman emerged as the primary supplier, exporting 1.79 mnt, with a marginal volume of 0.05 mnt routed via the UAE. However, according to sources, a significant portion of these shipments originated from Brazil and was routed through Oman and Malaysia for processing.

JSW Steel leads import volumes

JSW Steel emerged as the largest importer, with volumes rising to 10.02 mnt from 5.76 mnt in FY'25. Among pellet importers, Delta Global led with 0.34 mnt, followed by Suryadev at 0.33 mnt. Pellets were primarily sourced by mills in western and southern India throughout the year.

Jaigarh remains key import gateway

Jaigarh accounted for the largest share of imports at 5.9 mnt, followed by Krishnapatnam (3.56 mnt) and Kandla (0.99 mnt).

Factors driving higher imports in FY'26

Demand outpaced supply, widening the gap: Iron ore production rose 7.3% y-o-y to ~310 mnt, while crude steel output grew faster at 11% to 168 mnt. Given the ore-intensive nature of steelmaking, this mismatch created a structural shortfall, increasing reliance on imports.

Prolonged monsoon and high-grade constraints: An extended monsoon disrupted mining and logistics. Additionally, a significant portion of incremental production faced issues around ore quality and consistency. Despite higher output, availability of usable high-Fe ore remained tight, supporting import demand.

Import economics turned favourable: Global Fe 62% fines prices eased from aout $109/t in CY'24 to about $102/t in CY'25. Combined with elevated domestic freight and handling costs, this improved landed cost parity, particularly for coastal mills.

Global supply recovery supported availability: Improved seaborne supply and softer international demand enhanced cargo availability and pricing flexibility. With Chinese steel production declining from 1,002.26 mnt in CY'24 to 955.46 mnt in CY'25, major global miners increasingly targeted India as a growth market. Upcoming projects such as Simandou are expected to further boost global supply.

Outlook

Iron ore demand is expected to remain strong in the coming financial year, in line with the steel capacity expansion and production outlook. While domestic miners such as NMDC are working to increase high-grade output, depletion of quality reserves will continue to necessitate imports. As a result, import volumes are likely to remain firm, supported by persistent supply gaps and easing global prices amid rising international supply.