29-April-2026

- Exports fall to 24.7 mnt in Jan-Mar 2026 amid broad-based regional slowdown

- Sharp declines across East Asia and South Asia signal weakening intra-Asia demand

- Growth in Europe fails to offset contraction in core markets

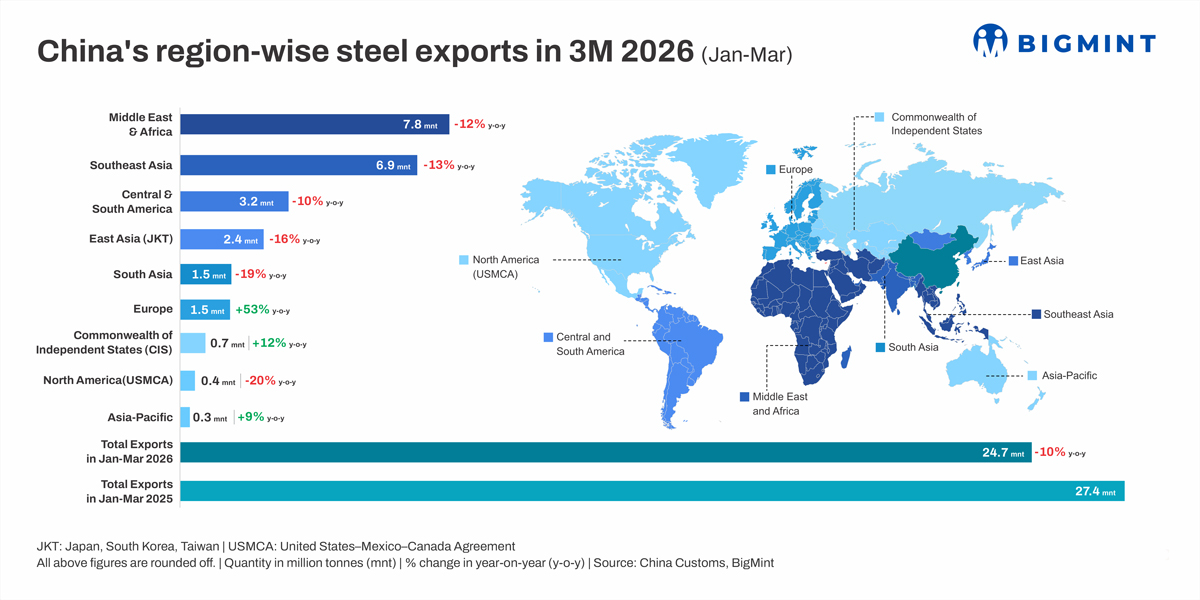

Morning Brief: Chinas steel exports declined 9.9% year-on-year to 24.7 million tonnes (mnt) in January-March 2026, indicating a loss of nearly 2.7 mnt of export volumes compared to the same period last year, according to BigMint data. While shipments increased month-on-month in March, the overall trend remains negative, pointing to reduced global absorption of Chinese steel.

The decline is broad-based, with major export destinations including the Middle East and Africa, Southeast Asia, and East Asia all recording double-digit contractions. Given that these regions account for over 60% of Chinas steel exports, the scale and spread of the decline suggest that the slowdown is driven by weakening demand across regions rather than a redistribution of trade flows.

East Asia and South Asia lead the decline

Exports to East Asia (JKT) fell 16% y-o-y to 2.4 mnt, marking one of the sharpest declines among major regions. Japan (-24%) and South Korea (-16%) recorded significant reductions in imports, indicating weaker industrial demand across key manufacturing economies.

South Asia saw a steeper contraction, with exports declining 19% y-o-y to 1.5 mnt. The drop was led by Pakistan (-40%) and Bangladesh (-26%), while higher shipments to India were insufficient to offset the decline across the region.

Core export markets weaken

The Middle East and Africa, Chinas largest export destination, saw shipments decline 12% y-o-y to 7.8 mnt, driven by sharp reductions in key markets such as the UAE (-38%) and Saudi Arabia (-13%).

Southeast Asia, the second-largest market, recorded a 13% y-o-y decline to 6.9 mnt, led by lower shipments to Vietnam (-33%) and Thailand (-22%), indicating weakening demand in major steel-consuming economies, despite moderate growth in Indonesia.

Central and South America also declined 10% y-o-y to 3.2 mnt, reinforcing the broad-based nature of the slowdown across regions.

Limited growth in secondary markets

Europe was the only major region to record growth, with exports rising 53% y-o-y to 1.5 mnt, though from a low base. However, emerging regulatory pressures such as the EUs Carbon Border Adjustment Mechanism (CBAM) are expected to increase compliance costs and limit long-term export competitiveness into the region .

Shipments to CIS countries increased 12% y-o-y, while exports to North America declined 20%, indicating continued constraints in accessing developed markets.

Outlook

We expect export flows to remain under pressure as demand across China's primary export regions has weakened simultaneously, leaving a gap of roughly 2.5-3 mnt in the first quarter that is not being offset by secondary markets.

While month-on-month improvements may support near-term volumes, they are unlikely to alter the underlying trend unless demand recovers in core regions such as the Middle East, Southeast Asia, and East Asia. In the absence of such recovery, incremental volumes will continue to face resistance rather than being redirected.

At the same time, tightening regulatory frameworks in developed markets, including carbon-related compliance requirements, are likely to raise costs and constrain growth into regions such as Europe. As a result, the system is likely to adjust through lower export volumes, with performance remaining dependent on a recovery in global steel demand.